Companies in South Africa taking pain – and consumers are paying the price

Companies in South Africa are experiencing heavy levels of distress amid rising costs.

This is according to the latest Deloitte Stability Index (DSI), which shows that companies across Africa are experiencing increased signs of distress for the first time since the pandemic.

Deloitte said the main culprits for the volatile input costs could be inflation, a weakening local currency, or supply chain issues.

Cash-strapped consumers are ultimately the ones who pay for the price increases.

The DSI measures the extent to which a company is financially stable. It is based on a granular model that converts leading indicators into a composite score and covers ten jurisdictions.

The financial ratios used in the DSI include Trading performance, Debt management, Return on assets, Financial leverage, Interest Cover and the Altman z-score (Risk of short-term bankruptcy).

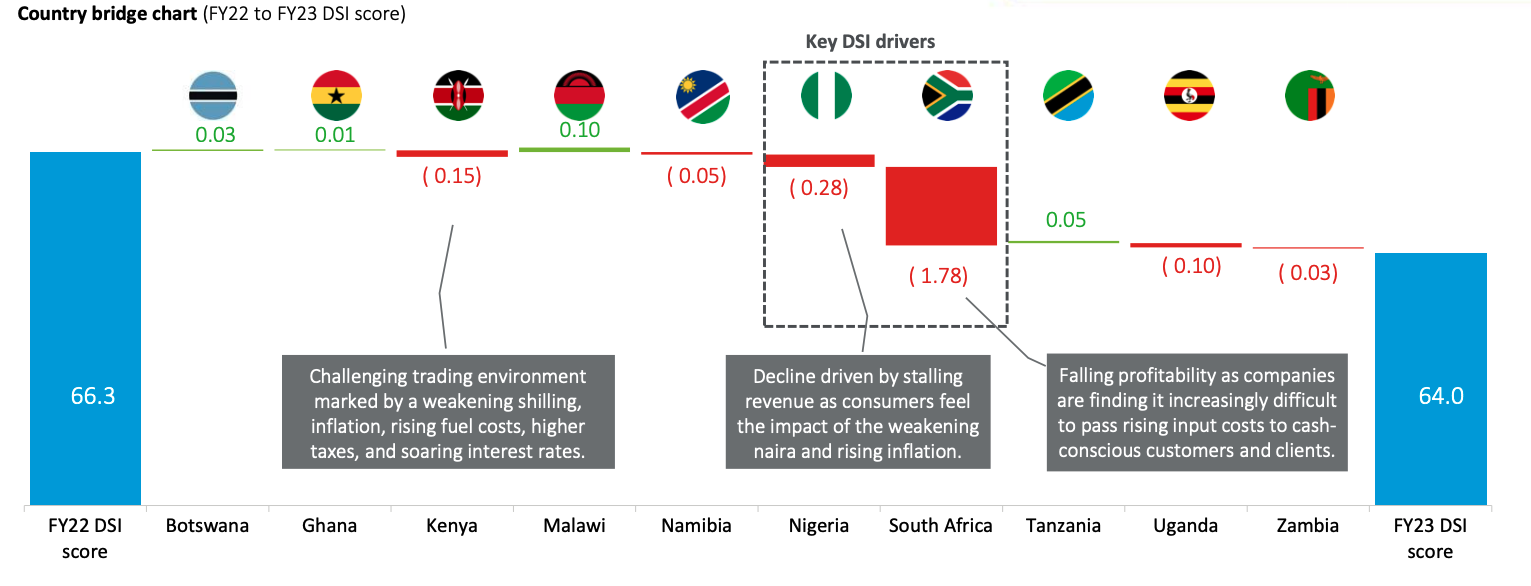

For the first time since the pandemic, the overall DSI score in Africa declined, with the key driver

for most countries being reduced consumer spending power and companies struggling to pass on volatile input costs.

Deloitte said that falling profitability as companies find it increasingly difficult to pass rising input costs to cash-conscious customers and clients.

South Africa was the largest contributor to the overall drop in the DSI of the ten countries involved in the study.

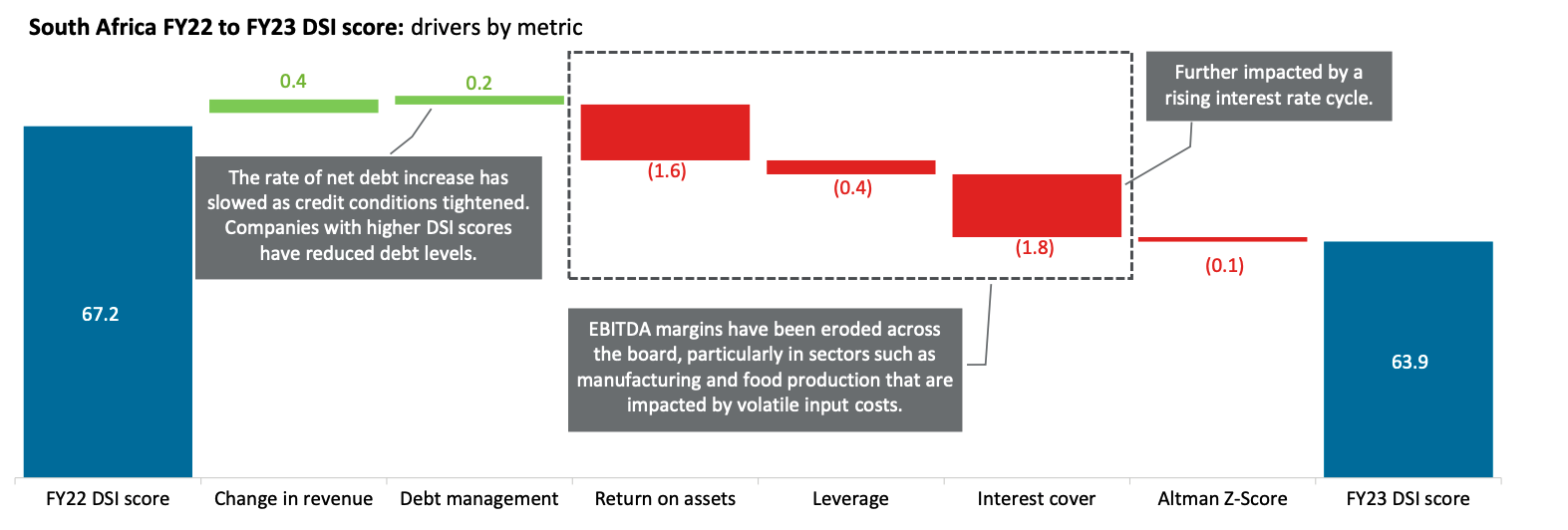

While the overall DSI score dropped from 66.3 in FY22 to 64.0 in FY23, the South African DSI dropped from 67.2 to 63.9.

“The South African DSI score has fallen for the first time since the pandemic, driven by eroding profitability in sectors reliant on commodity inputs (e.g. manufacturing) and consumer-facing sectors (e.g. retail) where already-thin margins have been squeezed further,” said Deloitte.

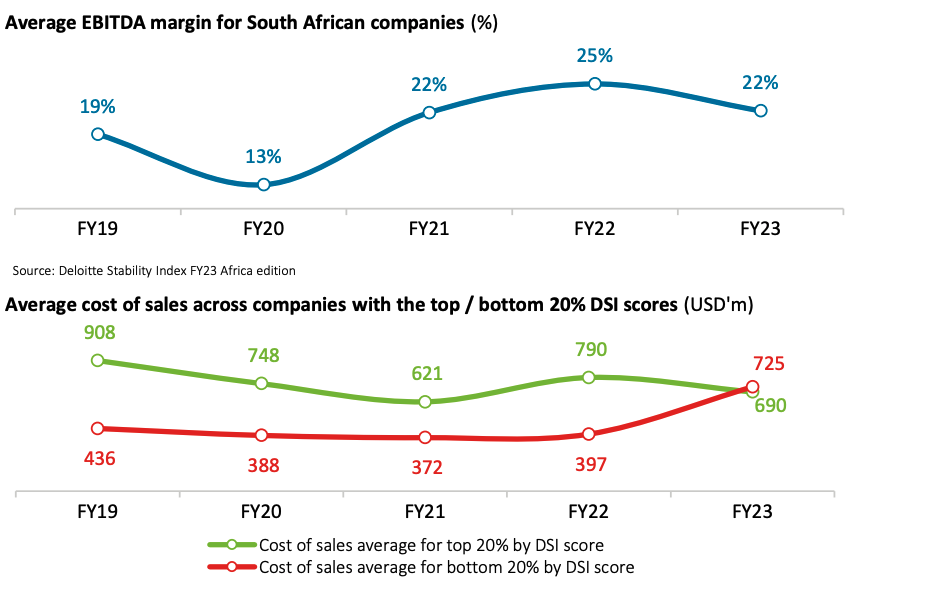

Deloitte’s data showed that the average EBITDA margin for South African companies dropped from 25% in FY22 to 22% in FY23.

“While overall average profitability has declined, the impact of rising costs is felt most keenly by companies with a lower DSI score. This disparity is not sector-specific. It may instead reflect qualitative factors such as the calibre of management and strength of board oversight,” said Deloitte.

“The key cause of the overall DSI score reduction in South Africa is rising costs and a reduced scope to pass cost increases to the customer.”

“However, companies with a higher DSI score seem better able to keep costs down. This effect cannot be explained by sector-specific trends as the DSI shows this divergence also occurs within sectors.”

Deloitte said that the widening gap between stronger and weaker companies probably lies in the quality of board oversight.

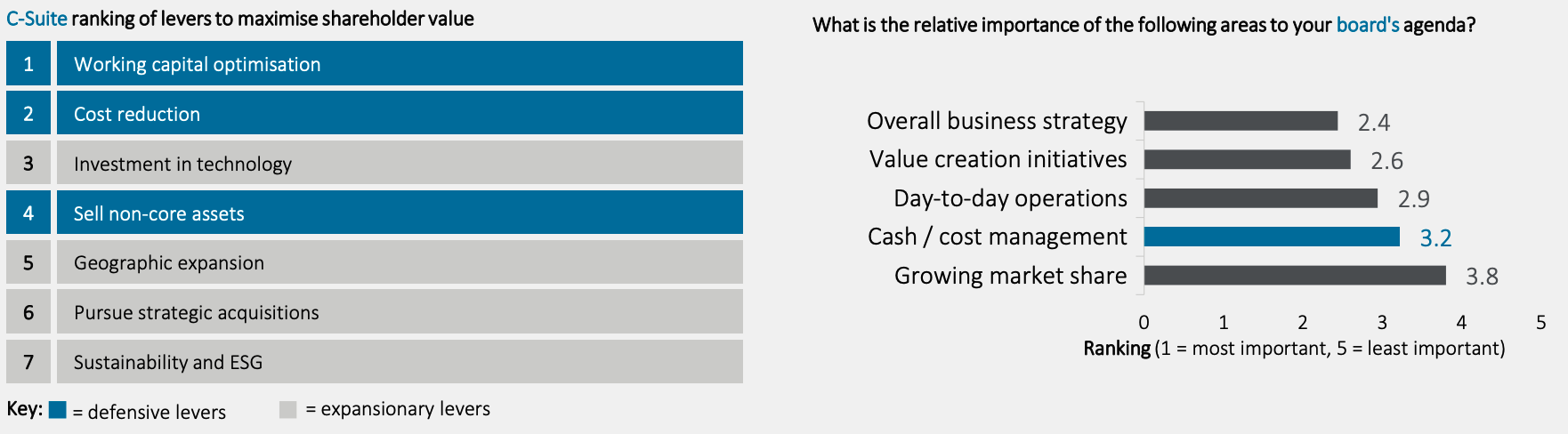

Deloitte’s Restructuring Survey showed that C-suite executives want to prioritise cost management initiatives, but they could face challenges from boards that do not share the same priorities.

The survey showed that boards are mainly concerned with the overall business strategy, with cost management further down on the list of priorities.

“In our experience, it is crucial that the board understands the importance of effective cost management initiatives and that there is executive-level sponsorship and accountability against tangible targets.

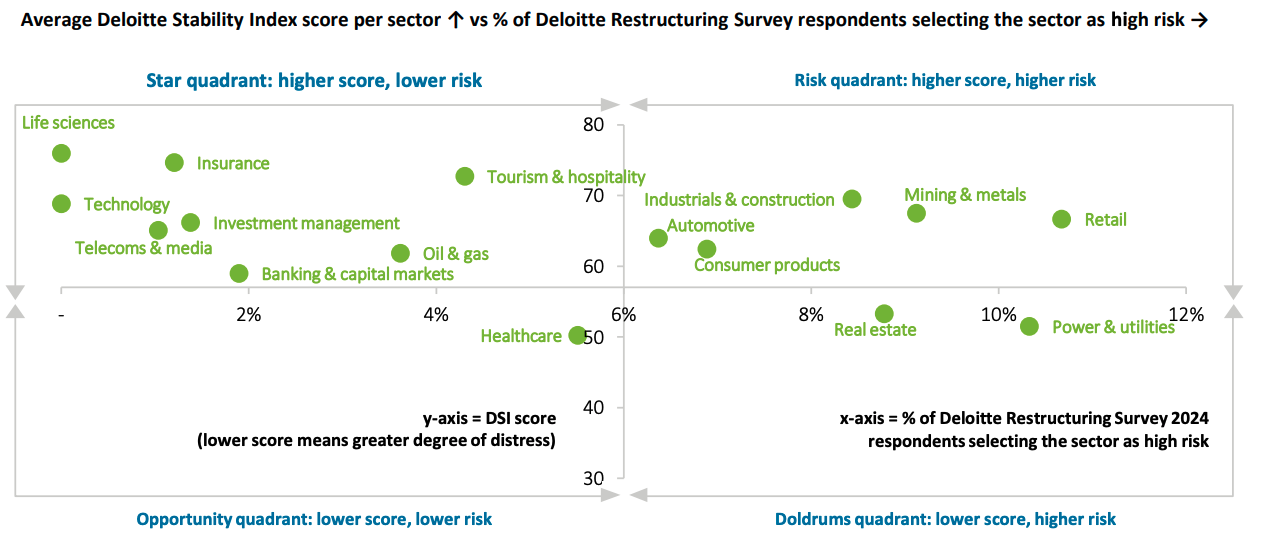

Sectors being hit hardest

In South Africa, retail and consumer products remain in the high-risk quadrant due to increasingly low consumer confidence.

The latest FNB and BER Consumer Confidence Index improved from an index score of -10 in Q2 2024 to -5 in Q3 2024.

Although this is an improvement and has been the highest level since the first half of 2019, it still remains below the long-term average.

Deloitte’s data also showed that the cost crunch has severely impacted the mining, industrial and construction sectors.

On the bright side, sectors in the lower-risk quadrants include Life Sciences, Technology, Insurance, Telcos, and more.

Read: South Africa’s best employers – with one making the top 20 in the world