Top South African retailer goes from hero to zero in 75 days

TFG (The Foschini Group) promised the market an exceptional performance during its 2025 Capital Markets Day. 75 days later, it produced results far below expectations.

During TFG’s Capital Markets Day on 6 and 7 August 2025, chief executive Anthony Thunström and his management team painted a rosy picture.

Thunström told investors that TFG has done much of the heavy lifting and that their strategy was working.

He told investors that TFG will be outperforming the market through consistent share gains and category leadership.

TFG CFO Ralph Buddle told investors they were driving sustainable growth through organic expansion, strategic acquisitions, and diversification.

He said they focused on store optimisation and were on track to achieve a 5-year compound annual growth rate (CAGR) of 12.5%.

He added that they drove margin expansion through initiatives like optimising inventory management and expanding in-house production capabilities.

There was also continued focus on cost control, which includes optimising store space utilisation and efficient resource allocation.

“There is a rigorous focus on managing operational expenditure, overheads, and supply chain costs,” Buddle said.

TFG has even started to use AI to reduce costs across various business functions by optimising and improving decision-making and process automation.

The TFG CEO added that their Africa Financial Services division is focused on enhancing Return on Equity (ROE) by leveraging origination of Value-Added Services (VAS).

He further said the management team ensures the strategic distribution of resources to maximise returns for investors.

A rude awakening for investors after TFG’s trading update

On Tuesday, 21 October 2025, TFG published a trading update for the six months ended 30 September 2025.

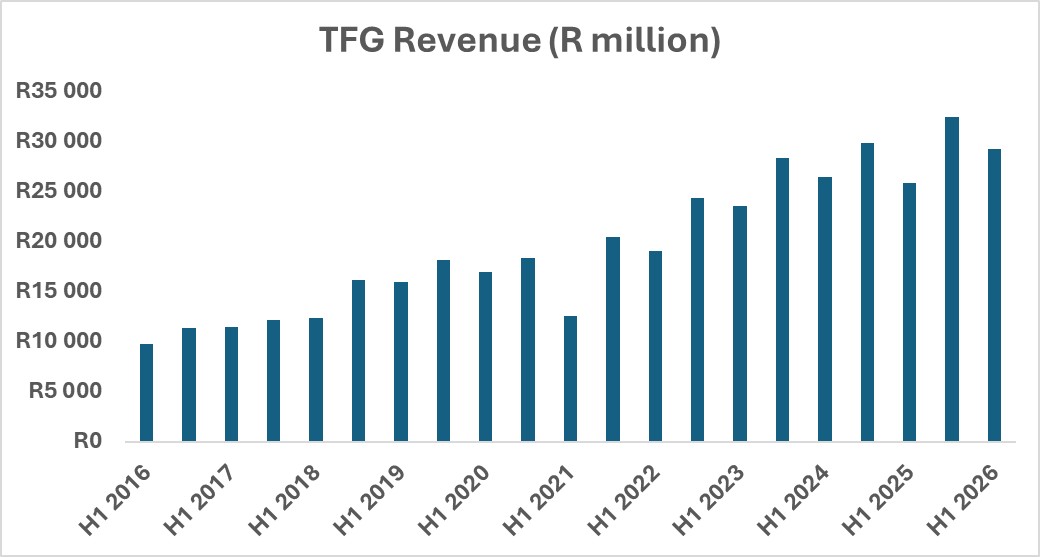

Over the reporting period, group sales grew by 12.7% to R29.2 billion. This included revenue from the recently acquired UK retailer White Stuff.

However, when the impact of White Stuff is removed, sales only rose by a more subdued 3.5% over the last six months.

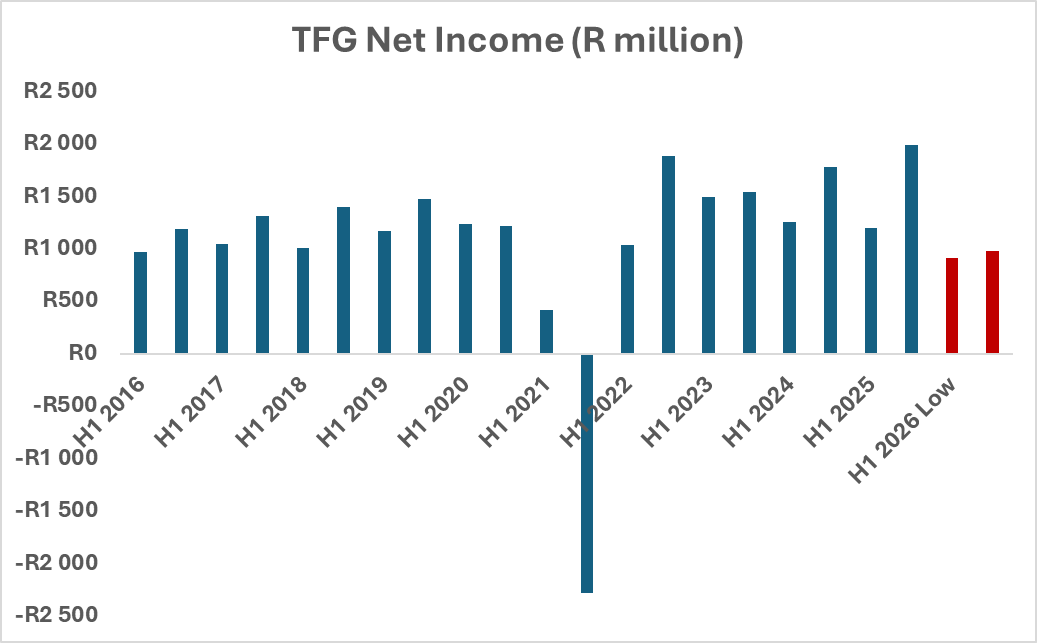

TFG further informed the market that its basic earnings per share will decrease by between 20% and 25%.

TFG explained that its acquisition of White Stuff resulted in finance costs doubling to £4 million (around R92.74 million).

TFG’s Australia segment also recorded a tough half-year, with sales down 0.5%. The company said this was due to subdued discretionary spending.

In addition, due to expenses growing ahead of sales, driven by costs from new stores and continued inflationary pressure, this segment’s EBIT declined by 18.4%.

The only true positive in the results was online sales, powered by Bash, which performed well over the period.

Group online sales grew by 55.3% in the six-month period, including White Stuff, and now contribute 14.7% to total retail sales. TFG Africa online sales grew by 40.2%.

Bash, under the leadership of e-commerce veterans Claude Hanan and Luke Jedeikin, brought all TFG brands together in a single platform.

It is widely seen as a game-changer for the company, reaching over eight million downloads within three years of its launch.

The company attributed much of its success to forward thinking and spotting the opportunity to launch an e-commerce platform at the right time.

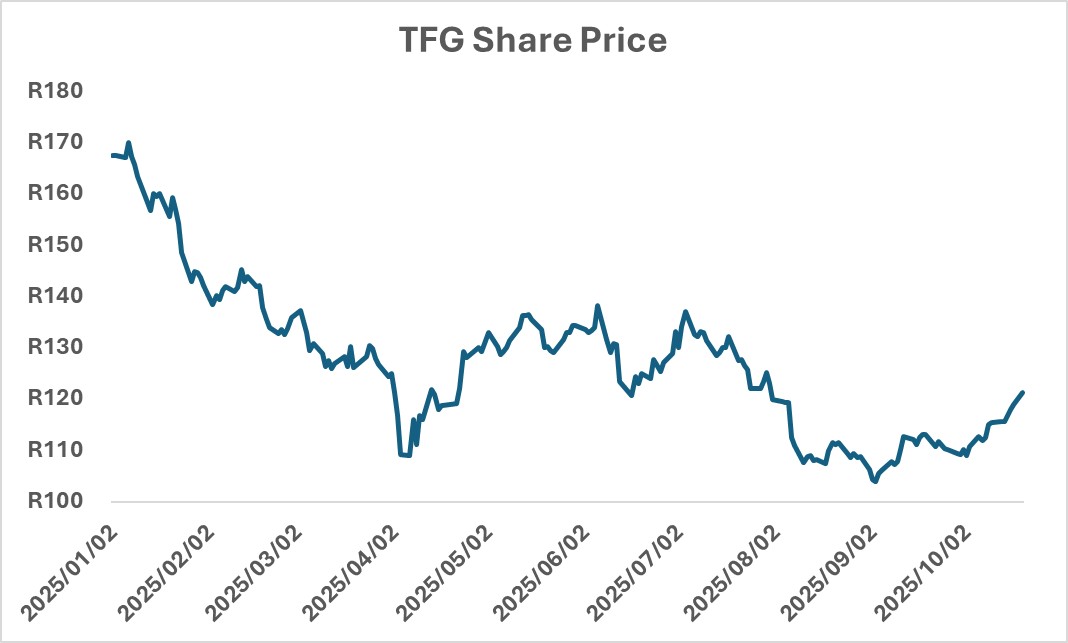

The poorer-than-expected results caused investors to dump the stock, and the TFG share price plummeted by 16.64% on Tuesday.

It wiped out R6.7 billion from the TFG market cap in a day, which showed the impact of the disappointing trading statement.

Analysts explain the TFG share price plummeted

Shane Watkins, Chief Investment Officer at All Weather Capital, explained that the reason for the sharp share price decline was not a poor trading statement.

Instead, it was “unexpectedly bad, considering what TFG, and its CEO, Anthony Thunström, told the market three months ago”.

The TFG management team recently engaged with large groups of institutional investors at their capital markets day and at a global bank’s conference.

“During these engagements, the TFG management team did not communicate the extent of the bad results they announced in their trading statement,” he said.

This means the market was surprised by the TFG trading update for the six months ending 30 September 2025.

This caused many investors to dump the stock, which caused the TFG’s share price to decline by 16.64% on Tuesday, 21 October 2025.

Watkins explained that TFG has grown largely through acquisitions over the last decade. However, these acquisitions did not strengthen the bottom line.

The TFG management team has, through the acquisitions, grown sales growth but not earnings growth.

“Despite growing revenue enormously, there has not been earnings growth,” Watkins told Business Day TV’s Stock Watch.

The result is that the TFG share price is the same as it was ten years ago, making it a poor investment.

The latest results, with fairly strong revenue growth but a big decline in earnings, continued the trend over the last ten years.

“This trend alarmed investors and made people question whether TFG’s acquisitive strategy is working,” he said.

Ricus Reeders from PSG Hole in One Ruimsig agreed, saying revenue growth and a decline in earnings show that margins are under pressure.

“This means that TFG’s acquisitions are not really doing the job they are supposed to be doing,” he said.

He added that TFG’s promise of earnings growth is taking longer than promised and is not fulfilling market expectations.

TFG Financial Performance

TFG’s Share Price in 2025