Major win for South Africa’s middle class

South African consumers are getting better at paying off their credit debts, with the country’s middle class experiencing a shift and improvement in repayment habits.

According to the latest Eighty20/XDS Credit Stress Report for the third quarter of the year, the total loan balance in South Africa increased by 0.8% quarter-on-quarter, reaching R2.6 trillion.

This points to a cautious response from consumers to mixed economic signals.

GDP growth is still muted, and unemployment remains high, despite the rate reducing, but with lower interest rates and low inflation, the appetite for credit has expanded.

Eighty20 noted that both active accounts and outstanding credit balances grew significantly year-on-year, with vehicle finance showing particular strength.

“The number of car loans and consumers with vehicle asset finance reached their highest levels in three years,” it said.

When looking at overdue balances, however, things are looking positive. These balances decreased by R3 billion or 1.4% quarter on quarter, down to R212 billion.

This brought the proportion of overdue debt down to 8.1% of total loan balances, down from 8.3% in Q2.

This decline in overdue balances was driven by a R2.5 billion decrease (2.5% QoQ) in overdue personal loans and a R1.1 billion decrease (6% QoQ) in vehicle asset finance (VAF) overdue balances.

The number of open loans grew by roughly 900,000 in the quarter.

The number of loans in arrears (at least one month past due) fell by 89,575 to 17.9 million, bringing the percentage of loans in arrears down to 33.1% in Q3 from 33.8% in Q2.

While this is still significant, this proportion has been dropping consistently since 2023 Q1, Eighty20 notes.

The number of loans in good standing—which has grown consistently for the past seven quarters—grew by 1 million, or a 2.9% QoQ increase.

This shows a continued upward, positive trend as more consumers work at paying off their debts and not falling into arrears.

South Africa’s middle class shows positive signs

Middle-class South Africans, or credit-active adults earning roughly R8,000-R30,000 per month (or R25,000 as a household), have been struggling over the past few years in particular to keep their heads above water.

But the data points to a cautiously optimistic shift.

Middle-class worker volumes in the credit space have remained stable QoQ at 3.6 million, accounting for 12.9 million active loans.

Of the 1.2 million new loans taken out by the segment this quarter, 73% were personal loans.

By balances, personal loans comprise 25% of the total credit balances held by the segment, while overall

balances have risen by 2.2% YoY to R541 billion.

Overdue balances have risen by 5.5% over the same period, with the average middle-class consumer having R23,000 overdue.

However, the percentage of those in the segment with at least one loan in default has fallen to 41.5%.

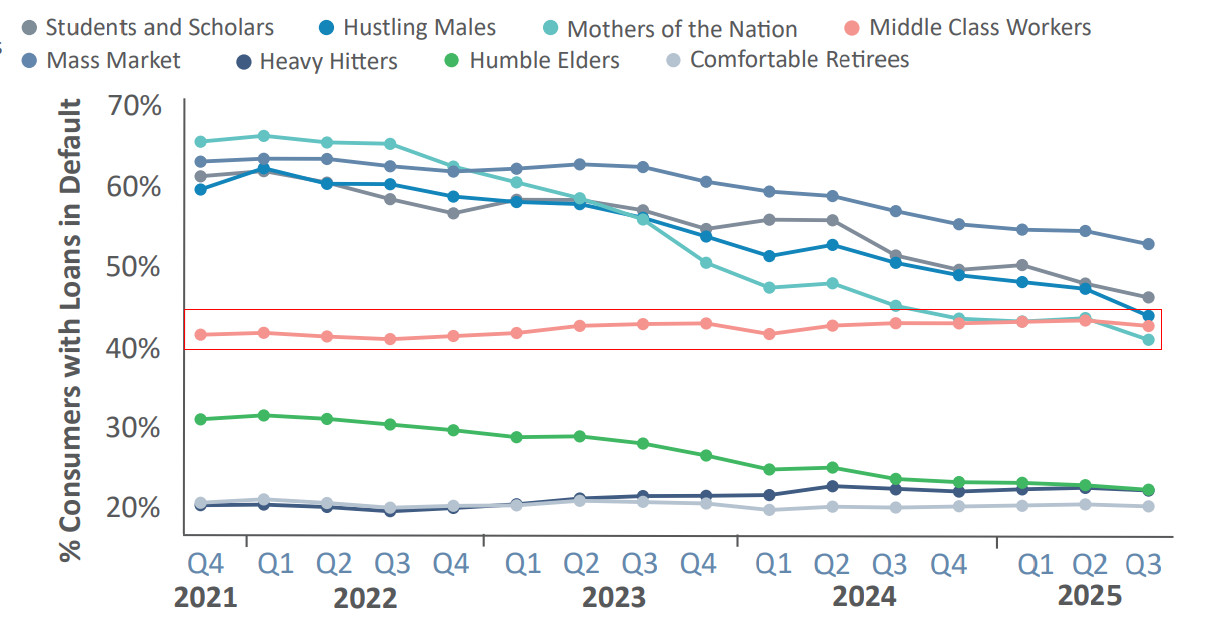

This tracks with the broader data, which shows that most market segments are getting to grips with their loans.

Default levels (three months overdue) remain lowest for Heavy Hitters, Humble Elders and Comfortable Retirees, while the Mass Market continues to show the highest default prevalence at 51%.

For the middle class, the levels have been generally flat, but the latest data marks a positive turn.

According to data from DebtBusters, South Africans earning more than R20,000—falling into a similar classification as the middle class here—are spending almost three-quarters of their income paying off loans.

Eighty20’s data shows that the average loan repayment in the segment is R9,388 per month, accounting for around 37% of monthly income.

DebtBusters’ data relates specifically to those who have entered into debt rescue processes, with Eighty20’s data reflecting a broader consumer profile.

Overall, credit-active individuals spent 28% of their net income on debt repayments in Q3, meaning between a quarter and a third of income goes toward servicing debt.

The heaviest burden falls on Heavy Hitters, who allocate 48% of their monthly income to instalments, followed by Middle Class Workers at 37%.

These markets have higher loan responsiblities due to them being for larger assets like vehicles or homes.

The Mass Market spends 19% of its income on debt, while Comfortable Retirees spend 22% of their monthly income on repayments, up from 20% in 2023.