How much you think you’ll earn over your entire career is probably way off

A new report reveals that South Africans drastically underestimate how much they are worth over their chosen careers.

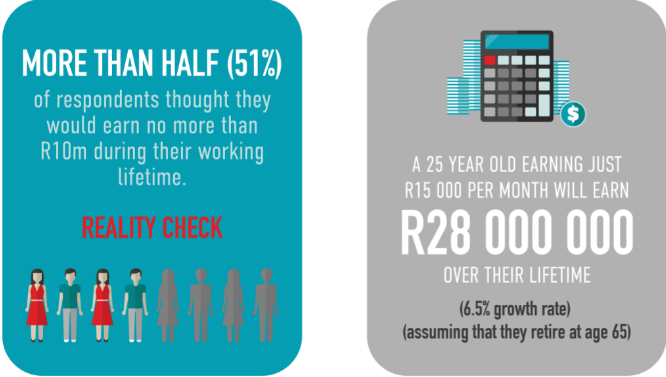

A survey conducted by Durban based life insurance provider, FMI shows that more than half of respondents thought they would earn no more than R10 million during their working lifetime.

However, a 25 year-old male earning R15,000 per month will earn as much as R28 million over their lifetime.

This calculation assumes a 6.5% growth rate and a retirement age of 65.

The most recent BankservAfrica Take-Home Pay Index (BTPI) showed that the average take-home salary in South Africa was R14,290 in current terms for May 2018.

FMI said that South Africans are dreadfully underinsured.

The Association for Savings and Investment South Africa (ASISA) has estimated that 14 million families face a combined insurance shortfall of almost R29 trillion should the main breadwinner become unable to generate an income.

“We conducted the survey to understand the perceptions of our industry, and introduce the realities that affect advisers and clients. Our aim is to change the life insurance industry for the better, and help protect the income of millions of South Africans when illness, injury or death occur,” said FMI CEO, Brad Toerien.

He said that there is still a general misunderstanding regarding the difference between life insurance and death cover. The survey showed that 48% of respondents believe that life insurance is death cover.

“This is a problem for the industry and one of the reasons why there are so many South Africans uninsured. The perception of death cover effectively means people don’t have cover because they simply don’t see the need for it. This could also mean that many have life cover, when they actually don’t need it, and may have an incorrect mix of cover,” Toerien said.

In the past, insurance providers have offered mainly lump sum benefits – especially for Disability, Critical Illness and Life Cover. Toerien warned that while this is a great way to settle debts or once-off expenses, they’re usually insufficient to cover unexpected monthly expenses.

“Income benefits are far easier to understand, as you don’t need to calculate the lump sum required to provide an entire future income.

“They’re also typically far more affordable than lump sum benefits, and income benefits make servicing the policy simpler in the long-term as all you would need to do is update salary amounts or monthly income with the insurer in order to ensure your client has the correct cover,” Toerien said.

Read: Are you richer than the ‘average Joe’ in South Africa?