Hammer blow to salaries in South Africa

South African salaries are under significant pressure, with data showing real take-home pay is steadily eroding and placing additional strain on households already battling rising costs and debt.

Investec chief economist Annabel Bishop has noted the latest numbers point to a worrying trend that could have broader implications for consumer spending and economic growth.

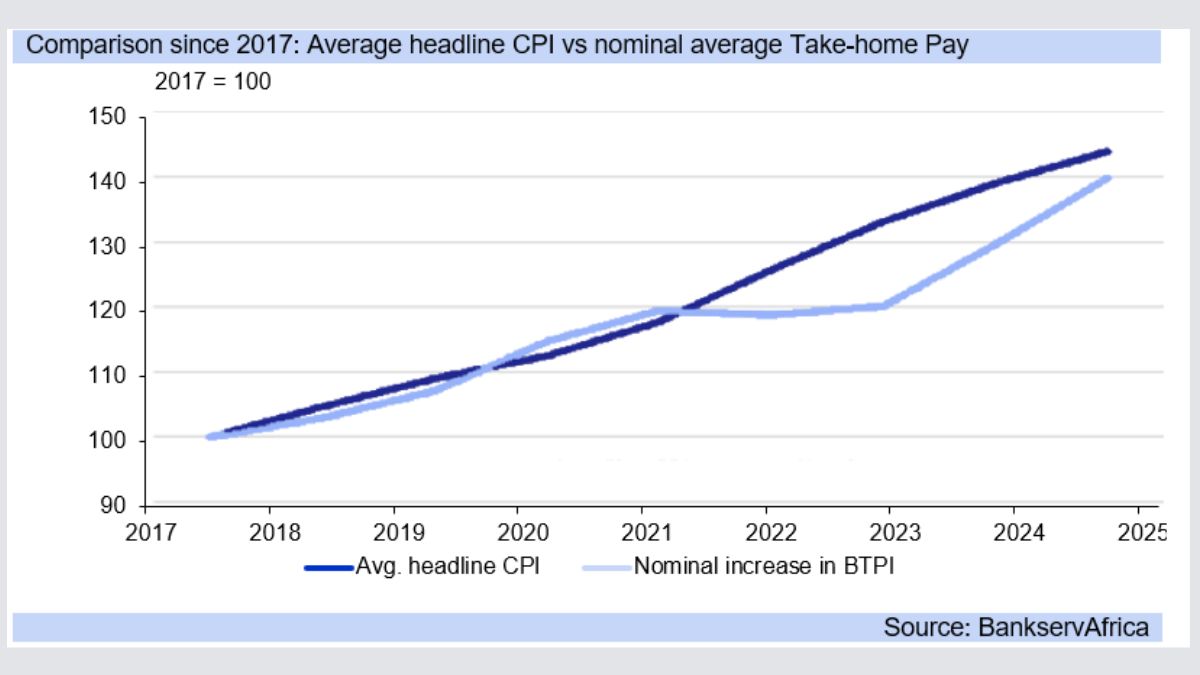

According to BankservAfrica’s real take-home pay index, or BTPI, real incomes adjusted for inflation fell by 0.9% month-on-month in July after contracting by 4.6% in the second quarter of 2025.

“Real incomes have fallen persistently since March, correcting for the substantial 5.2% surge in January and a further lift in February,” Bishop explained. From February to the end of July, real incomes declined by 7.1%.

This means that real monthly incomes are now below December 2024’s level, coming in at R14,660 in July and approaching October 2024’s outcome of R14,608.

Bishop pointed out that this drop coincides with weaker sales activity in the wholesale and motor trade sectors, which fell by 2.8% and 4.8% respectively over the same period.

While the July figure represents a decline, the average real monthly income remains above last year’s level, up 8.2% year-on-year.

However, Bishop cautioned that this is misleading. “The pace of growth is slowing steadily, falling from 12.8% in January to 8.2% by July.”

BankservAfrica also noted that although incomes are still higher than a year ago, the moderation is concerning and likely to persist due to base effects and ongoing economic constraints.

Additionally, actual nominal incomes, which are not adjusted for inflation, also fell by 1.1% in July and have declined every month since February, contracting by 4.6% in the second quarter.

“The ongoing drop in both real and nominal incomes is concerning, as it weighs on household consumption and ultimately GDP,” Bishop said.

Growth expectations for the economy remain muted. Bloomberg’s economic consensus shows GDP growth of just 0.4% quarter-on-quarter in the second and third quarters of this year, up slightly from 0.1% in the first quarter.

Economic growth on a knife’s edge

Bishop warned that without the boost from agricultural production earlier in the year, growth would have slipped into contraction. For 2025 as a whole, the consensus forecast remains at a modest 1.0% year-on-year.

She stressed that the marked drop in real incomes is likely to have negative consequences for household consumption expenditure, which is a key driver of GDP.

“Monthly data for the second quarter is mixed, but the decline in real incomes has direct implications for consumer spending power,” she said.

Rising inflation since March has also eroded household earnings. BankservAfrica noted that shifts in salary structures, with additional salaries being paid at lower levels and losses at higher-income levels, could also help explain the depressed trend.

Debt data paints an even bleaker picture. DebtBusters reports that 95% of South Africans who applied for debt counselling in the second quarter had a personal loan, while more than half also carried payday loans.

“Although recent interest rate reductions are welcome, high-interest personal loans continue to place consumers under severe pressure,” said Bishop. On average, households now need 70% of their income to service debt, the highest level since 2017.

For higher-income earners, the situation is just as worrying. Those taking home R35,000 or more are carrying unsecured debt levels that are 79% higher than in 2016.

“Consumers are still experiencing a notable degree of financial stress, with income growth significantly behind expense growth,” she said.

According to the latest debt index, the average pay packet today buys 49% less than it did nine years ago, once inflation is taken into account.

The strain is also visible in retail and trade sentiment. The Bureau for Economic Research (BER) retail trade survey showed retailer confidence fell by 8% in the second quarter, with 58% of retailers dissatisfied with operating conditions.

“The decline over two consecutive quarters suggests a moderation in retail sales growth, particularly as spending linked to two-pot retirement withdrawals winds down,” Bishop noted.

Sales and order volumes have deteriorated, with durable goods retailers—particularly in hardware—reporting weaker confidence. Semi-durable retailers started the year on a high but have also pulled back amid a deteriorating macroeconomic outlook.

For Bishop, these signals confirm that household spending will remain constrained in the months ahead, keeping overall growth subdued.

“Mixed data indicates GDP growth of around 0.5% quarter-on-quarter for the second quarter, which is hardly enough to suggest a meaningful recovery,” she said.