South Africa’s middle class is in serious trouble

South Africa’s middle class continues to struggle with debt repayments amid a subdued economy, with more pain expected in the months ahead.

Eighty20’s 2026 Q1 Credit Stress Report has broken down how credit behaviour and key economic events affected South Africans over the period.

It noted that South Africa’s economic outlook has shown modest improvement over the quarter, with GDP growth revised up to 1.6% for the year, while inflation eased to 3.2% in the quarter.

Retail sales, measured in real terms, also increased by 2.8% YoY. That said, unemployment climbed to 32.7%, driven by rising youth unemployment due to weak job creation.

There were also losses in entry-level sectors, and losses in sectors like construction and informal trade constrained opportunities.

Overall, credit active consumers and loan balances, especially personal loans, rose, but overdue debt rose 5.6% QoQ, with 35.5% of loans in arrears.

Total open loans grew by 875,000, or 1.6%, in the quarter, to 56 million loans, while outstanding balances grew by R41 billion, or 1.4%, to R2.7 trillion.

Over-indebtedness also increased, with 41% of credit-active South Africans in default, which involved three or more months in arrears, on one or more loans.

The number of defaulters grew by close to 400,000 people, and the number of loans in arrears grew by more than 1 million – the largest proportion of loans in arrears since 2024 Q3.

The number of credit-active individuals increased by 5.9% YoY, largely due to an 11% increase in personal loan holders.

The total sum of overdue balances increased in Q1 by R12.6 billion, which is 5.6% growth for the quarter, and 14% YoY to R237 billion, which accounts for 8.8% of total outstanding debt.

The middle class is suffering

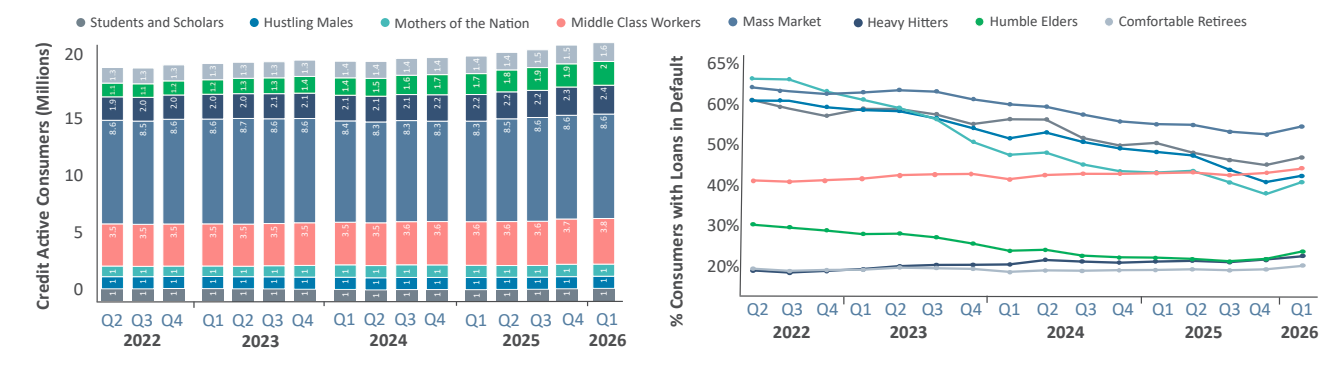

The number of credit-active individuals in the Middle Class Workers segment reached 3.8 million in the

quarter, marking a 5% YoY increase.

The segment had 13.3m open loans, up from 12.5m in 2025 Q1. Personal loan balances accounted for 25% of the total loan balance, while vehicle asset finance accounted for 20%.

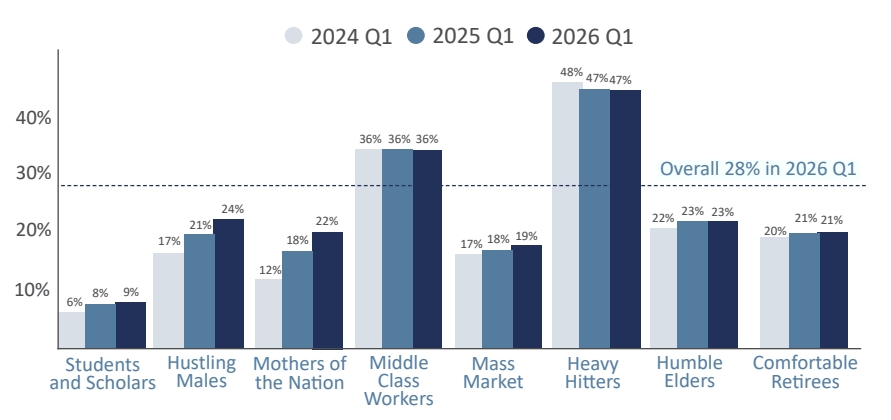

Total overdue balances increased to R92.5 billion, rising by 4.9% QoQ, while the percentage of defaulters jumped by 2 percentage points to 43% in 2026 Q1.

The average overdue balance rose by 4.4% to R24,583. While this is a large increase, it is still a far smaller jump than the 12.6% increase to R26,163 for the average overdue amount for the nation’s wealthiest.

The heavy hitters segment saw an increase in credit active individuals QoQ, rising 1.9% to 2.4 million. The total open loan balance amounted to R1.8 trillion.

The number of personal loan holders in the heavy hitters segment saw the largest annual and quarterly increases among all segments, rising 11% YoY and 3.3% QoQ, respectively.

The total overdue balances among Heavy Hitters increased 5.7% QoQ to R62.2 billion. The percentage of loan defaulters rose to 24%, from 23% in 2025 Q1.

Meanwhile, the Mass Market segment reported the highest default rate at 52%, up 4% from the previous quarter. The total overdue balance on open loans also increased by 6.6% QoQ to R46.2 billion.

Pain incoming

Eighty20 warned that the Q1 report marked the end of a recent run of positive economic news. In Q2, oil traded above $100 per barrel, and the nation was then hit by two of the largest fuel price increases in history.

On top of the fuel price pain, there was also an 8.76% rise in electricity tariffs, and inflation was climbing to 4%. The impact of the Iran war is also expected to hit food and fuel prices.

The Reserve Bank also responded by hiking rates by 25 basis points last week, and warned that three further increases are possible depending on the economy’s response to the Iran war.

“The hope is that the Middle East conflict is a short one, and the government’s plans with the 2026 budget will provide the calm needed to weather this storm,” said Eighty20.