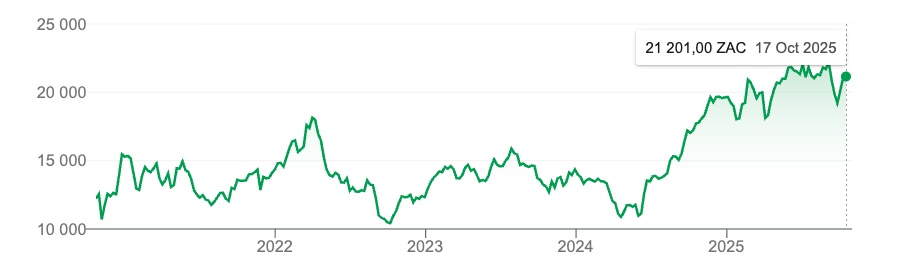

Investors like what they see from Discovery

Discovery’s recent financial results have been strong, with PSG Wealth putting a buy recommendation on its stock.

In its financial results for the year ended 30 June 2025, Discovery saw massive profits, with Discovery Bank becoming profitable for the first time.

Discovery said that its headline and normalised headline earnings increased by 30% to R9,625 million and R9,781 million, respectively.

The group’s normalised return on equity increased to 15.4%, from 13.5% in the prior year.

Despite the strong rise in earnings, the company noted that economic growth was below potential in many regions that it operates.

The group declared a final dividend of 152 cents per share, adding to the 87 cents per share in the year’s first half.

However, it noted that the interest rate cut provided a better backdrop for investment markets.

“Discovery has emerged strongly from its significant investment cycle, which focused on creating new avenues for long-term growth,” it said.

“This has positioned the Group for a new distinct phase of scaled organic growth, with focused execution through its recently formed global composite, Vitality, and its domestic business, Discovery South Africa.”

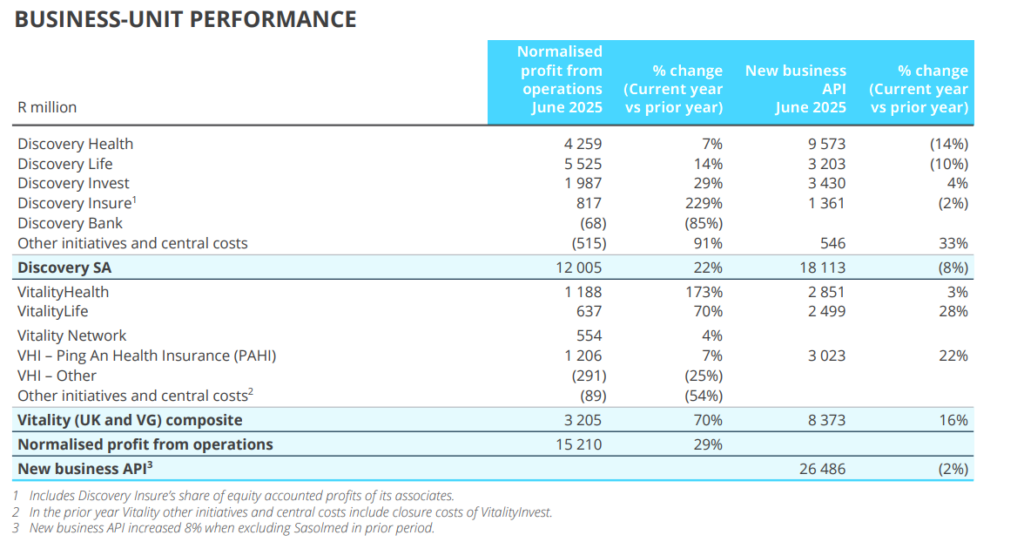

Discovery South Africa saw 22% growth in normalised profit from operations to over R12 billion.

This included a stronger performance from Discovery Bank, which saw its total number of clients increase by 30%. Its advances rose by 39%, while deposits rose by 26%.

The group’s performance resulted in strong revenue growth, and the bank saw its first profitable period during the second half of the financial year, which was ahead of plan.

The bank still declared a R68 million loss for the full financial year, but this was an 85% improvement from the previous financial year.

Discovery Health (7%), Discovery Life (14%), Discovery Invest (29%) and Discovery Insure (229%) saw mild to extreme normalised profit growth.

A buy recommendation

Amid the strong performance, PSG Wealth Equity Analyst Marnus Piekaar has placed a buy recommendation on Discovery.

PSG Wealth noted that Discovery’s brand serves affluent, health-conscious consumers who value rewards, which allows for higher pricing while maintaining strong customer loyalty and brand strength.

It added that the data-driven Vitality platform drives deeper engagement and cross-selling opportunities.

As the latest results showed, earnings are well spread across health, life, banking and other fee-based services, which creates predictable cash flows.

The broad product suite also enables Discovery to increase value per client by cross-selling health, life, banking and investment products. This then increases revenue without incurring heavy new customer acquisition costs.

Regarding growth, there is long-term upside from further International Vitality partnerships, new product extensions, and Discovery Bank’s continued expansion.

However, Piekaar said that there are still potential risks facing the financial services provider, including a low-growth environment, which reduces discretionary spending.

Although insurance is seen as a need, it is often one of the first things cut by consumers in challenging financial situations.

Another risk facing Discovery is the National Health Insurance (NHI) risk. As per the current legislation, it remains unclear what items medical aids can cover.

Although the NHI is still 10 to 15 years away, it may be an issue for Discovery and other healthcare insurers if it comes into effect sooner.

Competition also remains a concern for Discovery, with Sanlam and TymeBank teaming up to offer personal loans.

Old Mutual has launched its own bank, which, like Discovery Bank, will operate digitally and not feature any branches.