Dark clouds for South Africans earning less than R40,000 per month

Credit check data from PayProp reveals that South African renters earning under R40,000 per month are still under significant financial strain, spending over 50% of their income on debt.

The 475 basis point hikes in South Africa’s interest rates have driven consumer debt levels to unsustainable heights.

With the prime lending rate now at 11.75%, South Africans face increased repayment costs on loans, mortgages, and credit cards.

This has led to rising financial stress among consumers, as higher monthly payments are straining already tight budgets, making it difficult for many to manage their debts.

The result is a surge in credit impairments and defaults, reflecting the unsustainable debt burden carried by South African households amidst ongoing economic challenges.

PayProp highlighted that this has weighed heavily on renters in the country.

PayProp is the largest processor of residential rental transactions in South Africa, handling over R1 billion in transactions each month.

PayProp reported that in Q2 2024, credit check data indicated that tenants’ expenses have been increasing faster than their average incomes.

While rents as a percentage of income remained relatively stable year-on-year, debt repayments as a percentage of income increased from 43% to 46.7% for the average applicant.

The average disposable income has also decreased from 27.2% to 23% of net income compared to a year earlier.

This trend is in line with data from the South African Reserve Bank (SARB), which showed that household debt as a percentage of disposable income reached its highest level in over a decade in Q1 2024.

The SARB pointed out that the combination of higher interest rates and stagnant wages has put significant financial strain on South African households, leading to record-high debt levels and a rise in defaults.

Additionally, PayProp observed that those earning R40,000 per month or less are facing a heavier debt burden.

According to the PayProp Rental Index, on average, tenants who earn less than R40,000 per month are using more than half of their net income to repay debts.

Data from other credit firms show similar signs, with some indicating that the situation is even worse.

One of these firms is consumer analytics and research firm Eighty20, which aggregates its data from 42 million adult South Africans representing over R3.7 trillion in earnings per annum.

It noted that with interest rates rising and high inflation, lower to middle-income groups are starting to feel significant financial strain.

According to the firm’s latest data, this group, which includes large families and represents less than 10% of the population, holds two-thirds of vehicle asset finance (VAF) loans and three-quarters of home loans by value.

Eighty20 highlighted that these South Africans, with a take-home pay of about R42,100 after tax, have unsustainable levels of debt in the second quarter of 2024.

The company noted that this group holds around 30% of all home and vehicle asset finance (VAF) loans in South Africa despite representing only 20% of the total loan value.

For a typical affluent individual, debt repayments account for 66% of net income, with two-thirds of their debt secured.

In contrast, while those who earn more than R40,000 per month also have high debt levels, Pyprop highlighted that debt spending falls sharply, and disposable income rises to match.

Its credit check data showed those earning R80,000 and up have 54.1% of their net income left over after rent and debt expenses.

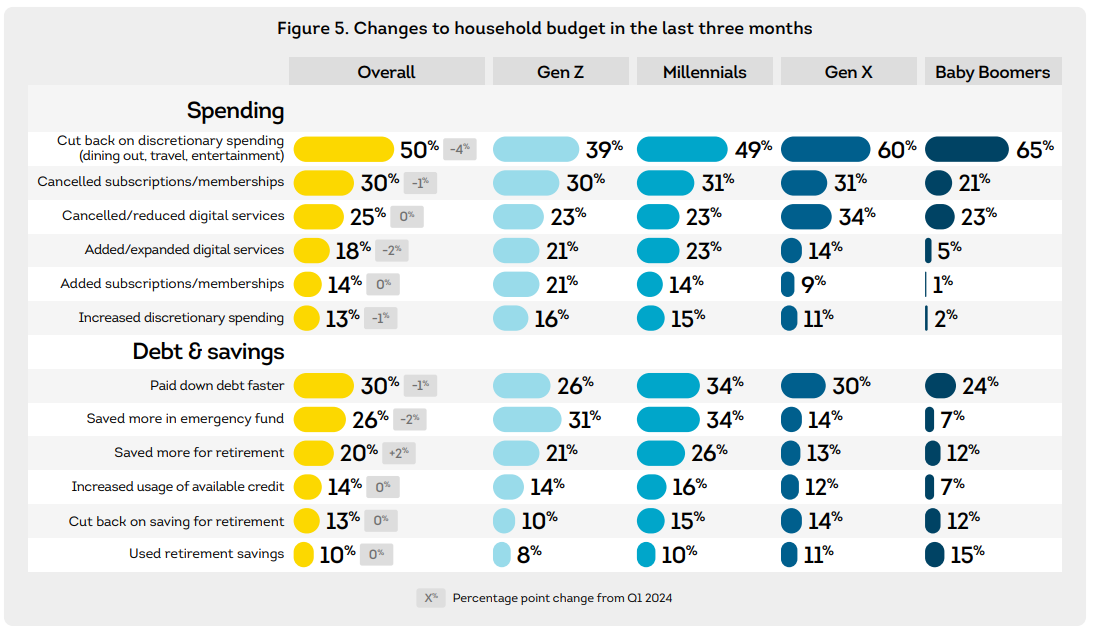

As a result, data from TransUnion’s Consumer Pulse Survey show that many South Africans, including those who earn under R40,00 per month, still have to cut certain expenses each month to make ends meet.

The survey noted that more (38%) consumers planned to spend more on bills and loans over the next three months, 13 percentage points more than those who indicated they’d decrease spending in this category.

It added that 50% of consumers surveyed are expected to cut discretionary spending.

This includes travel, dining out, in-store or online shopping, and large purchases like appliances or cars.