South Africa’s Ouma is doing great

South African grocery, baking and sugar producer RCL Foods has seen a nearly 40% jump in earnings for the six months ending December 2024, presenting a remarkable boost in operations post its restructuring.

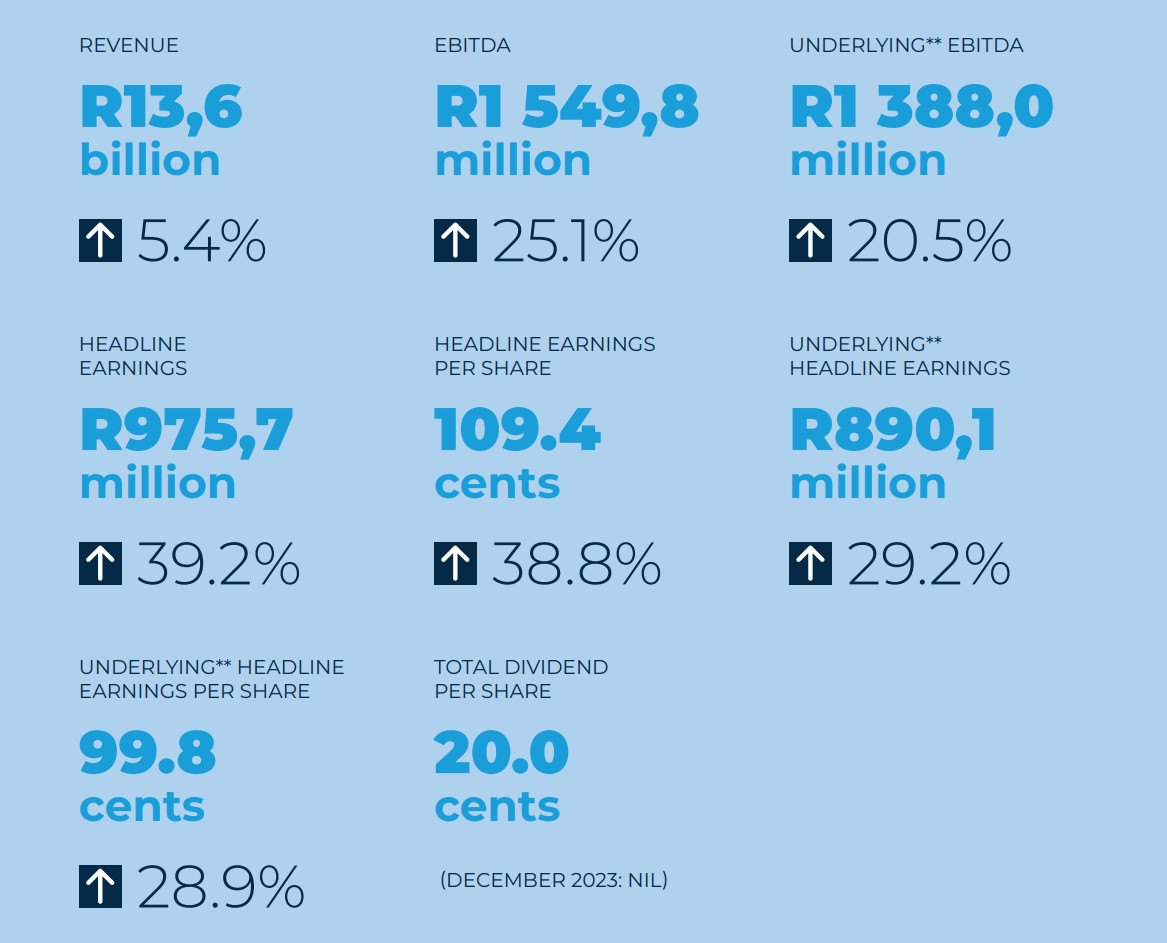

This represents headline earnings of R975 million for the period, up 39.2% from R701 million in the comparable period ending December 2023.

Revenue was up to R13.56 billion from R12.85 billion before, with operating profit at R1.2 billion.

Headline earnings per share were up 39% to 109.4 cents. The group declared a dividend of 20 cents.

This is the group’s first set of results since restructuring its portfolio in 2024, where it disposed of Vector Logistics and unbundled Rainbow Chicken.

According to the group, this allowed it to focus on growing its branded businesses and its stronger brands.

It said the main drivers of its positive results were the baking segment, which saw earnings before tax increase by R195 million, and the groceries segment (up R88 million).

This is despite the continued challenging environment for South African consumers, who remain under pressure despite more positive turns in the wider economy.

RCL said it has navigated this by managing price increases while being mindful of consumer pressures and constraints.

This has been aided by price relief in commodities like wheat, the absence of load shedding and lower fuel costs.

The group has also managed to keep its market share stable, with its brands remaining relevant to consumers.

RCL carries many well-known and beloved brands, including 5Star Maize, Ouma Rusks, Nola, Sunbake, Yum Yum Peanut Butter and Selati Sugar.

It also owns many pet and pet food brands like Bobtail, Catmor, Dogmor and Ultra Pet.

Some of its brands are dominant in the market, with the group touting a 60% share of the rusk market with Ouma Rusks.

Sugar rush

While the group’s business has been boosted significantly since the restructuring, it is still struggling in certain sectors, particularly in sugar, where margins have thinned.

The sugar segment saw revenues jump 7.1%, but underlying margins narrowed by 3.7% in rand terms.

Despite lower world market prices and increased imports, the group benefitted from a higher share of the local industry and having managed to contain costs.

The group said it is actively involved with a ‘Sugar Master Plan 2.0’, which entails working with the Department of Trade, Industry and Competition to mitigate regulatory issues.

Notably, RCL said that the department is supporting a delay in changes to the Health Promotion Levy (aka, the “sugar tax”) while the industry explores ways to diversify.

“The industry is currently seeking a review of the mechanism used in determining the import duty, which is a regular occurrence over time as duties of this nature become ineffective,” it said.

“Given the level of subsidies offered internationally and the conducive climatic conditions in key exporters, we hope to receive an outcome from the review that levels the playing field.”

Looking ahead, the group said it is optimistic that sugar will continue to perform well but remains wary of lower international pricing and inadequate import protections.

For its wider business operations, RCL said that it remains focused on the basics and its strong brand portfolio.

It expects 2025 to deliver a turnaround in the economy, but still expects households to remain under pressure, leading to tough trading conditions in the short to medium term.