More South Africans are falling behind on their car payments

While consumer debt stress levels improved during the first three months of 2018, vehicle loans remain a cause for concern, as the first-time credit default rate rose to above average levels among many South African households over the time period.

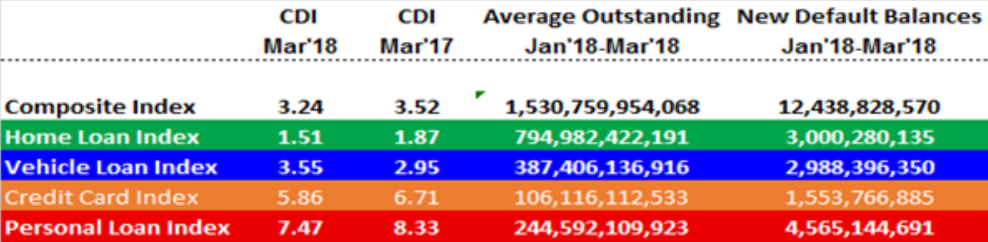

This is according to the latest Experian Consumer Default Index (CDI), which found that there was a 0.28% year-on-year decline in total credit defaults compared to the same period in the previous year.

“Though there has been a stabilisation of first-time credit default value and a slowdown in credit take-up and use, which contributed to the improvement over this period, vehicle loans continue to pose a risk for many South African households,” said David Coleman, chief data officer at Experian SA.

While year-on-year improvements were observed across personal loans, credit card and home loans, vehicle finance was the only product type to show annual and monthly deteriorations.

The Experian CDI for vehicle loans reached 3.55% in March 2018 which was significantly higher than the CDI of 2.95% in March 2017.

“Increased vehicle sales could have led to more loans for this product type being extended within a short period of time and contributed to this asset class’ riskier performance,” he said.

“As such, March represents the sixth consecutive month of increases for the Experian vehicle loan CDI.

“To put this further into perspective, the CDI for vehicle loans at 3.55% tracked higher than the overall CDI of 3.24%, indicating the extent of the defaults from this product type alone.”

Who is defaulting

The impact of first-time credit defaults for vehicle loans is evident among households with different classifications.

Experian found that the segment of middle-aged educated families with mid to high income levels and residing in suburbs around industrial and mining areas recorded a vehicle finance CDI of 2.83% in March 2018 compared to 2.51% in March 2017 – the highest outstanding vehicle loan debt.

Another significant movement in the overall CDI and for other product types was among the ‘minimum wage rural families’.

“This segment of mixed-age families on minimum wages living in small informal dwellings in the rural areas of the Northern Cape and the Free State, had the worst-performing overall CDI at 7.36% in March 2018, a deterioration from 7.42% in March 2017,” Experian said.

“This segment also had significantly the worst performance for the vehicle loan CDI at 7.54% in March 2018 compared to 6% in March 2017, as well as the worst performing for the credit card CDI of 10.28% in March 2018 from March 2017’s 8.03%.”

Meanwhile ‘Secured Affluence’ consisting of mature, well-educated wealthy couples living in free-standing high-value established homes in city suburbs showed the lowest overall CDI of 1.74% in March 2018 compared to 2.02% in March 2017, Experian said.

“This segment also fared well for other product types of vehicle loans (March 2018: 2.47% vs March 2018: 2.04%) and credit cards (March 2018: 3.94% vs March 2017: 4.51%).”

“More South African households, particularly those in the rural parts of the country, are having to come to terms with their credit purchasing decisions over the December spending season with stress continuing to grow in the vehicle finance sector,” Coleman said.

Read: Petrol price increase could be even higher than expected in June: Dawie Roodt