South Africa turmoil highlights emerging-market political risk

South Africa’s unfolding turmoil is putting emerging-market political risks at the fore, and traders are hunting for currencies vulnerable to political hazards and playing them off against their more stable peers.

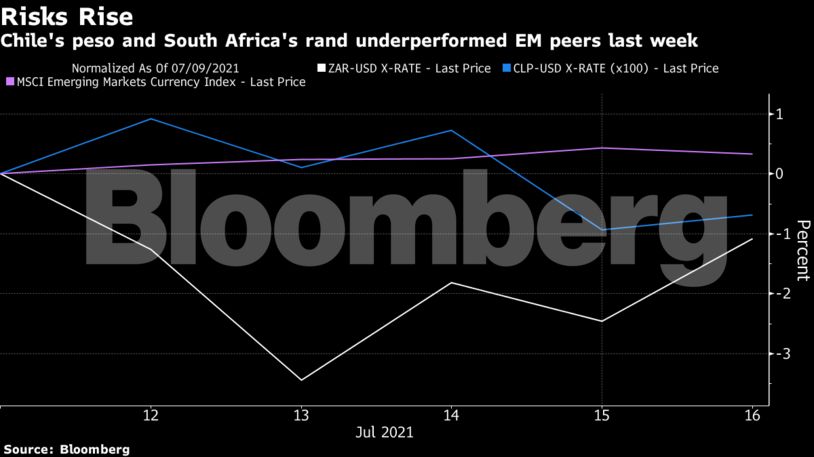

Citigroup Inc and Deutsche Bank AG were among the lenders recommending investors to short the South African rand last week as deadly riots threatened to derail an incipient economic recovery. Chile’s peso could also swing in the coming months, depending on the outcome of the nation’s presidential vote.

With elections coming up in many major developing nations over the next three years and the pandemic worsening socio-economic fault lines, “political long Covid” may cast a widening pall, according to Bank of America Corp.

Of particular concern is what that means for monetary policy, as central banks weigh the risks of quicker inflation against the need for economic support.

“Part of what’s happening in South Africa is the delayed effect from the social and economic devastation triggered by Covid, which we are likely to see more of in the future,” said Francesc Balcells, London-based chief investment officer of emerging-market debt at FIM Partners.

“You want to stay away from crowded trades that have embedded a lot of political risk.”

While the rand remains this year’s top emerging-market performer, it has fallen as the violence that erupted following former president Jacob Zuma’s jailing presented a deepening crisis for his successor, Cyril Ramaphosa.

Last week, the currency touched its weakest against the dollar since March as the potential blow to the economy from the turmoil and a spike in Covid-19 cases reined in expectations for tighter monetary policy.

South Africa will likely keep its interest rate unchanged on Thursday, economists predict. With a more hawkish policy stance in Russia, UBS AG said it prefers the ruble to the rand, with a potential weakening in metal prices adding to pressure on the South African currency, according to Manik Narain, head of emerging-market cross-asset strategy at UBS in London.

Russia is expected to raise its benchmark rate by 75 basis points on Friday.

Kota Hirayama, an emerging-market economist at SMBC Nikko Securities Inc in Tokyo, suggested selling the rand and buying Turkey’s lira after that country’s central bank resisted President Recep Tayyip Erdogan’s calls for lower rates and vowed to maintain its monetary stance until a major drop in price growth.

“As for the rand, the riots have caused considerable economic damage, may quell market expectations for a rate hike while raising concerns that funds may flow out of the country,” Hirayama said.

“Being long in the lira, which has higher interest rates, and shorting the rand is a rational trade as investors can earn yield differentials.”

Others see the rand’s slump as a buying opportunity. Commerzbank AG now favors it against the lira, betting the Turkish currency’s gains against the rand since early June are likely to be reversed by October, according to Tatha Ghose, a London-based senior economist at the firm.

Credit Agricole CIB said it closed a strategy to buy Chile’s peso against the rand, booking a 2.3% profit after South Africa’s turmoil sparked a selloff.

“We are getting concerned about rising political risks in Chile,” strategists Sebastien Barbe and Olga Yangol wrote in a note. “As investors’ attention increasingly turns to the political developments, we prefer to take the chips off the table tactically.”

On Sunday, one-time student protest leader Gabriel Boric and former government minister Sebastian Sichel won the country’s presidential primary in upset victories, potentially calming some investor jitters.

The rand and Chilean peso were among the biggest developing-nation currency decliners against the dollar last week, along with Hungary’s forint and Poland’s zloty. Brazil’s real, Peru’s sol and Turkey’s lira advanced.

Election Risks

The sol has suffered the second-biggest loss in the developing world over the past three months, with leftist outsider Pedro Castillo winning the June 6 runoff.

Investors are concerned that another less market-friendly candidate may emerge in Latin America as Brazilian president Jair Bolsonaro’s popularity falls to the lowest since assuming office ahead of general elections next year.

“There is a strong correlation between countries where you are seeing the potential for political instability – i.e. South Africa and much of South America – and a poor track record at combating Covid which is resulting in lagging growth vis-a-vis countries that were much more successful in dealing with the virus,” said Todd Schubert, head of fixed-income research at Bank of Singapore Ltd.

In South Africa, just 7% of the population has gotten at least one vaccination jab, compared with rates of around 50% or above for most European nations. It’s about 20% in Peru, while 44% of Brazilians and 29% of Colombians have received at least one jab, according to Bloomberg’s vaccine tracker.

Schubert is “less enthusiastic” about Peru, Colombia and Brazil because of the “potentially enhanced political volatility,” he said.

Colombia’s credit rating was cut to junk by S&P Global Ratings and Fitch Ratings as the nation’s debt outlook worsened after the government withdrew a bill to raise taxes which triggered mass civil unrest.

“Governments often indulge themselves in fiscal extravagance prior to elections, a choice not so readily available given the Covid-related fiscal largess of many countries,” said Marshall Stocker, a money manager at Eaton Vance Corp in Boston.

“That could make incumbent governments more vulnerable at the ballot box and in the streets.”

Read: 8 ways the last week of violence and looting will hammer South Africa