How would a downgrade impact South Africa’s bond market?

Considering the market noise around a credit rating downgrade, and the growing negative sentiment in South African consumers and investors, it’s important to ask the question: How would a downgrade impact the South African bond market?

The short answer is that a downgrade would lead to it being more expensive for the South African government to borrow money, said Eugene Visagie, portfolio specialist, Morningstar Investment Management South Africa.

“Let’s first look at what it means to be downgraded. Think of it as a credit score from your bank manager – the less likely you are to default on your debt repayment, the better your score will be, whereas a weak score would indicate that you are more likely to default, and not be able to repay your debt.

“When you have a bad credit score and you are seen as someone that could potentially not repay a loan, the establishment extending the credit to you assumes more risk in lending the money to you – as opposed to someone with a good credit score.

“Therefore, the credit provider will charge you a more expensive rate in order to be compensated for the increased level of risk it assumes in lending you the money. In the same manner, South Africa is rated on its ability to repay its debt and charged more when it has a bad credit rating,” Visagie said.

So, what would the implications of a downgrade be for South Africa?

Morningstar said that the rand could weaken against the US dollar due to foreigners selling local bonds.

A sub-investment grade rating by all three major rating agencies would result in South African government bonds being removed from some major world bond indices such as the World Government Bond Index (WGBI), the financial services company said.

This could translate to a forced selling of South African bonds by international investors that are mandated to only hold investment-grade credit. “In other words, certain investors would have to sell SA bonds as they won’t be allowed to hold such an investment,” said Visagie.

Over the past decade, foreigners have bought a lot of government bonds and at the peak, they owned close to 40% of our bond market. However, of late, they have been selling our bonds and this number is now closer to 30%, which is still meaningful, the portfolio specialist said.

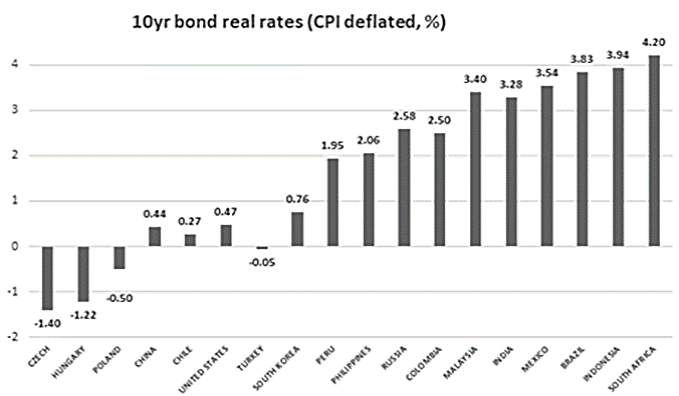

“Whilst market pricing would suggest that these risks are priced into S.A. bonds (given that they are offering investors a real yield of close to 4%), it is possible that we could see yields creeping higher on the day of the downgrade, along with a weaker rand. Remember, if bond yields rise, it results in capital losses for bond holders.

“With that said, rising yields could also create buying opportunities for investors. Times of panic and stress often present golden opportunities to enhance returns if one can price risk appropriately.”

If history is the best teacher, what have we learned?

Like South Africa, Brazil has also suffered from political uncertainty over the last couple of years. Midway into 2015 Standard & Poor’s (S&P) changed the status of Brazil’s sovereign credit rating outlook to negative.

The change in the outlook (not an actual downgrade) led to the demand for the government’s ten-year bonds dropping. This is similar to the conditions that South Africa is currently faced with, Morningstar said.

“Upon the news of Brazil’s outlook change, yields went from 12% to exceeding 16%. The currency followed suit and depreciated by roughly the same amount against the US dollar in approximately the same period – all without the country being downgraded.”

Expectations were paved and the market priced in a downgrade. In September 2015, as predicted, Brazil took the plunge from investment grade to junk status (a move from BBB- to BB+ in Standard & Poor terms), Morningstar pointed out.

“It is interesting to note that both the currency and the yields started to strengthen/contract as if the market had predicted the worst-case scenario, priced the risk accordingly, and then pro-actively managed this risk before it even came to fruition,” said Visagie.

“It would seem, at the moment, that the global market has taken the same stance with South Africa and is virtually pricing in the worst-case scenario – before the actual event has occurred.”

As illustrated in the graph below, South Africa is currently one of the few countries globally to offer healthy real yields (this is after taking inflation into account) but is still required to pay more than countries such as Brazil and Mexico, both of which are already rated at sub-investment grade.

Read: South Africa should look to pensions instead of an IMF bailout: ANC