Tough times for shopping malls in South Africa

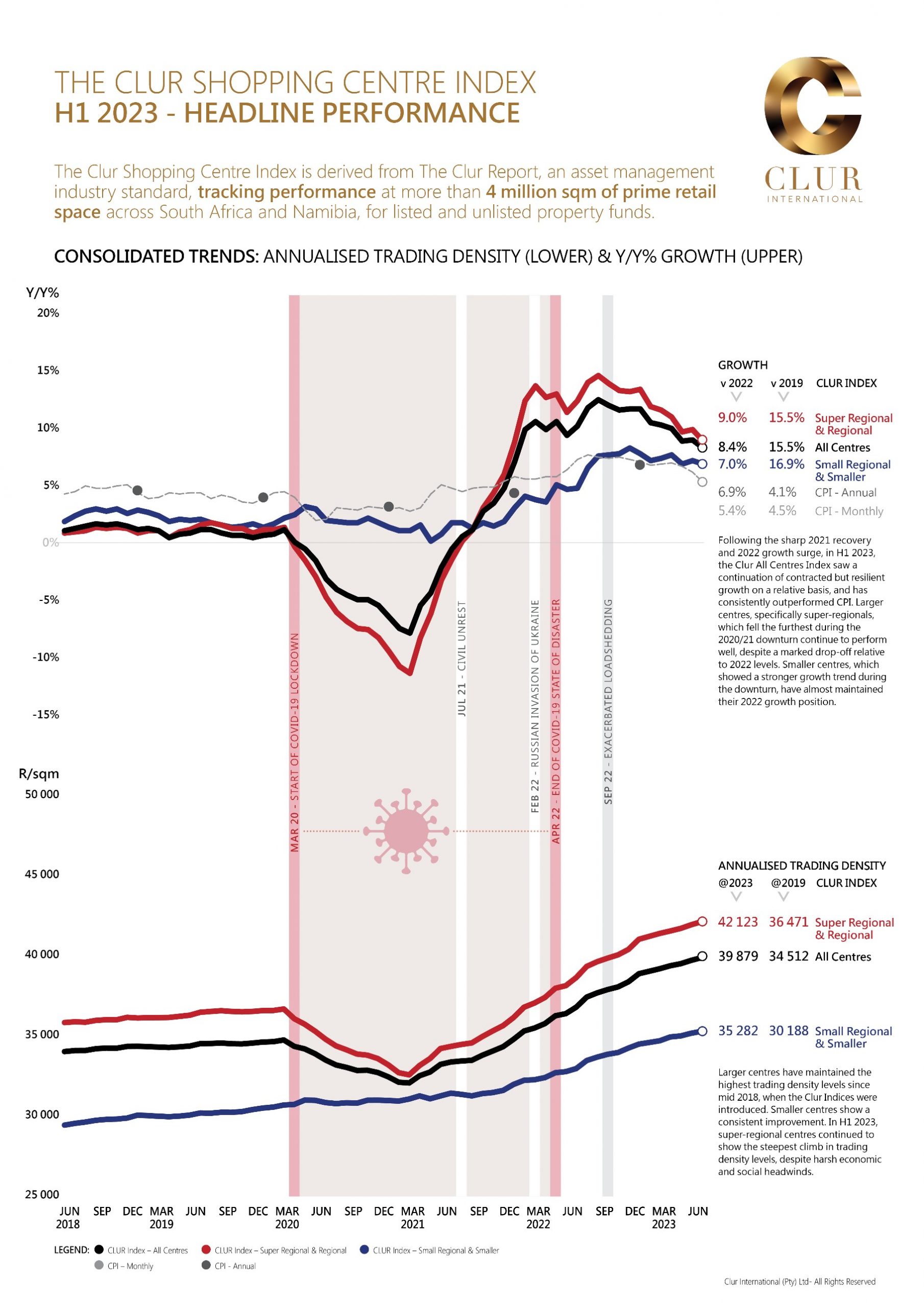

Trading densities at South African shopping centres continued to contract in the first half of 2023.

This is according to the Clur Shopping Centre Index, which tracks the performance of listed and unlisted property funds at South Africa and Namibia centres.

Belinda Clur, managing director of Clur International, said that the continued fall-off was expected as consumers have been constrained by the harsh economic climate and GDP growth is predicted to be muted for the rest of the year.

“This market position requires an acute strategy to capitalise on a powerful combination of under-traded opportunities and over-traded cautionaries amid bustling leasing activity and increased risk appetite,” Clur said.

The Clur Index for all centres in Q2 2023 saw an annualised trading density of R39,879/sqm, marking a growth rate of 8.4% compared to June 2022.

However, it was down 3.4% on the growth figure from Q4 2022 and down 1.7% from Q1 2023. That said, it did beat the 5.4% headline inflation figure for June.

Larger malls had the largest trading density levels, recording a 9% rise year-on-year over the June 2022 figure, however, there was a 2.1% decline from March 2023.

Super regional centres saw an 11.5% year-on-year growth on the June 2022 figure to R47,327/sqm – the best-performing segment.

Smaller centres still show strong resilience despite the difficult trading environment, as the annualised trading density for Q2 2023 stood at R35,282/sqm, representing 7% growth but only 0.8% lower than both Q4 2022 and Q1 2023.

Clur said that the signs of the overall fall-off started to appear in September 2022 when load shedding intensified.

“The retail property market is now finding a more natural position. As people have returned to a more interactive world, recent years have seen a swing from a Covid survival tenant mix to a post-Covid curated lifestyle mix,” Clur said.

“This is now evolving into a bolder balanced mix, containing clear elements of experimentation and depth of texture as the market responds to a more settled consumer. “

“Key trends emerging from this leasing activity are a greater appetite for risk, which we have seen building over the year, as well as asset management preparations in the lead up to Black Friday and festive season trading, and an increase in new concept local and international brand entries.”

Opportunities and risks

The dominant categories across the index, accounting for three-quarters of new leased space, are apparel, grocery/supermarket, speciality, homeware, furniture and interior, and food service.

Apparel is leading the way with 28%, with shoes having the largest footprint and taking up 5% of space.

“From a consumer perspective, trendy trainers and elegant flat options are favoured– a shift caused by the Covid-casual-comfy athleisure approach to clothing,” Clur said.

This is followed by unisex wear and women’s wear, at 3.2% and 1.8%, respectively, with there being a preference for either boutique or large stores and no middle ground.

“This reinforces the current increased appetite for risk, with a shift away from small size stores – a message of be distinct, make a statement, don’t be in the middle and bland,” Clur said.

The supermarket/grocery category, the second biggest new lettings lender, had a 15.1% take-up across the whole index in Q2, with the huge supermarkets between 1,000 and 4,999 sqm at 13.5%

However, Clur has warned that the apparel sector, which represents 20.4% of the overall index, is becoming over-traded and could tip over in terms of space over-representation.

“This could have a dilutionary effect on trading densities. By contrast, the grocery/ supermarket and food service sectors show signs of being under-traded, with room for a responsible space take-up. That is encouraging as these together make up over 20% of the full index.“

Clur emphasises that mall and retailer strategies for these sectors should not ignore the growing consumer movement toward ethical food and clothing decisions, which will increasingly define future consumption patterns.

“Digging deeper into Clur Index apparel findings points to sound growth opportunities within athleisure wear, men’s wear and small format unisex wear stores, which show signs of being under-traded. “

She has also cautioned that department stores are becoming overtraded.

“That is a critical finding given that the sector makes up 22.8% of the full index. The category is signalling a need to be pruned back to protect trading densities for this large space component and open opportunities for better performers,” she said,

On the other end of the scale, Clur said that technology, second-hand dealers, pet/vet stores, health, beauty and wellness, food speciality and bottle stores, as well as accessories, jewellery and watches, are all currently under-traded and have great growth opportunities.

The Clur Shopping Index can be found below (mobile users can click on this hyperlink):

Read: Another of South Africa’s biggest malls is up for sale