Nice surprise for South Africa – but the problems can’t be ignored

The mining and manufacturing sectors – two of South Africa’s most prominent contributors to GDP- are facing significant headwinds despite posting better-than-expected production data in October.

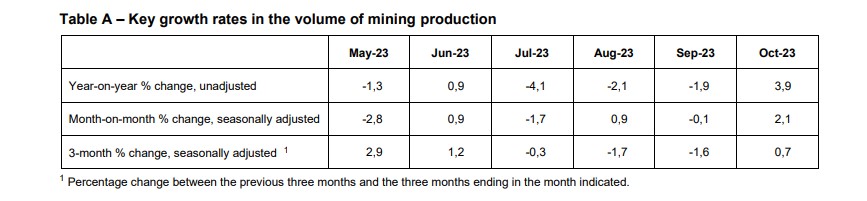

According to Stats SA, mining production increased by 3.9% y/y in October after September’s 1.9% drop – ahead of the Bloomberg consensus of a 1.2% y/y lift.

The main contributors to the increase were:

- PGMs (16,9% and contributing 4,0 percentage points);

- manganese ore (8,9% and contributing 0,7 of a percentage point);

- chromium ore (13,8% and contributing 0,6 of a percentage point)

Seasonally adjusted mining production also increased by 2,1% m/m in October 2023, following a 0.1% m/m decline in September.

Diamond production did, however, fall for the 13th straight month due to the strained global environment, with China’s demand rebound taking longer than expected, weighing on sales.

“Notwithstanding October’s result, which was buoyed by base effects, the fragile global environment, especially the subdued manufacturing sector continues to weigh notably on commodity demand,” Investec economist Lara Hodes said

“The results from the S&P Global Steel Users PMI Survey for October pointed to an overall deterioration in operating conditions, and to the greatest extent since November 2022”.

Manufacturing

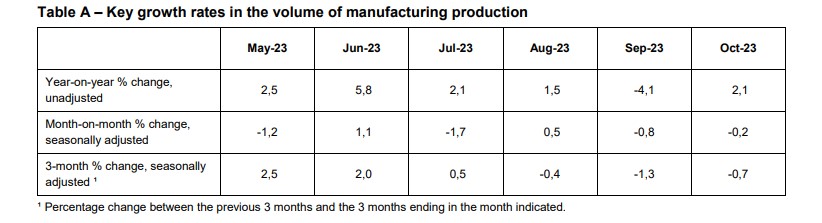

Manufacturing production jumped by 2.1% y/y in October 2023 following September’s reading of a 4.1% y/y decline – this was again ahead of the Bloomberg consensus of 1.7% y/y.

The largest positive contributions came from:

- Petroleum, chemical products, rubber and plastic products (7,8% and contributing 1,5 percentage points);

- Motor vehicles, parts and accessories and other transport equipment (6,0% and contributing 0,6 of a percentage point)

However, seasonally adjusted manufacturing production dropped by 0.2% m/m.

Seven of the ten manufacturing divisions reported negative growth, with the largest negative contribution coming from the food and beverages division (-3.5% and contributing -0.8 of a percentage point).

Strained global conditions and major domestic challenges affected the manufacturing sector activity and export potential during October.

Ultimately, the 2.1% y/y rise was supported by base effects after the massive Transnet strike in October 2022.

“Despite October’s result, the sector remains lacklustre. Indeed, the seasonally adjusted (SA) headline Purchasing Managers’ index (PMI) moved further into contractionary territory (below 50) at the start of the fourth quarter.”

“The unfavourable outcome was largely underpinned by a slump in the business activity index. According to the BER, the weak activity reading most likely reflects continued strained demand conditions in SA.”

Outlook

Mining output is down 1.3% YTD, even if it is less severe than the 7.1% decline seen in 2022.

“The lingering impact of load-shedding, as well as rail and ports infrastructure inefficiencies, is expected to continue to disproportionately weigh on the sector’s activity. Slowing global growth, including in China, bodes ill for South Africa’s major mineral exports,” Thanda Sithole, FNB Senior Economist, said.

However, manufacturing is up by 0.2% YTD, highlighting some improvement from 2022, with more growth expected in the future.

“The subdued manufacturing activity underscores manufacturers’ concerns about unfavourable operating business conditions. Nevertheless, we envisage a modest pick-up in activity over the medium term as demand and infrastructure conditions gradually improve,” Sithole said.

Read: Government’s R175 million plan to protect tourists ahead of the festive season