SARS cutting a lifeline for these taxpayers in South Africa

SARS and the National Treasury have moved to allay concerns around changes to the definition of “bona fide inadvertent errors” in tax filings, noting that the stricter interpretation has corporates and high-net-worth individuals in mind.

Earlier this year, the tax service appeared to cut one of the biggest lifelines to taxpayers that helped them avoid penalties.

Under Section 222(1) of the Tax Act, taxpayers face severe penalties for understatements in their tax assessments.

These penalties can run up to 200% of the shortfall between what taxpayers declare and what a revised assessment concludes.

However, these penalties could be avoided if the understatement were a “bona fide inadvertent error.”

Under the draft 2025 Tax Administration Laws Amendment Bill (TALAB), the definition of this error had been “clarified” to show that this protection was only ever meant to be used in cases of substantial understatement.

This led to a flurry of warnings that taxpayers with any other understatements would now be penalised for mistakes, even if they were made through genuine mistakes.

While the new draft laws do not delete or rewrite section 222(1), the National Treasury made it clear that it views the wider use of the phrase as “contentious and adverse” to a coherent penalty framework.

The statute still has the broad language, and nothing in the written law confines its application to only one category (ie, “substantial understatements”).

However, any taxpayer challenging SARS on understatements would immediately run into the clarification.

This signalled to tax practitioners that SARS would no longer accept the excuse that tax mistakes were genuine errors and would simply see them as negligence and impose penalties.

Not going after the average taxpayer

Presenting to the Standing Committee of Finance this week, SARS and the National Treasury cleared the air about the change, saying that taxpayers making genuine errors should be safe.

Specifically, the NT said that Section 222(1) of the Tax Administration Act (TAA) makes it clear that understatement penalties cannot be imposed unless taxpayers exhibit certain behaviour.

It said that the penalties are intended to act as a disincentive to taxpayers taking aggressive positions where large amounts are at stake.

Currently, these taxpayers act in the knowledge that if they are detected and successfully challenged, the worst that can happen is that the tax that should have been paid is paid, along with interest at market-related rates.

Notably, the NT stated that the concern here relates to large corporations and high-net-worth taxpayers in particular.

“If none of (these) behaviours are present, then no element of culpability exists on the side of the taxpayer, and no penalty can be imposed,” it said.

Further, it added that the onus remains on SARS to prove available facts on which it based the imposition of the understatement penalty and from which one of the behaviours it can be inferred.

It will be up to the taxpayer to demonstrate that an understatement was the result of bona fide inadvertent error.

“Whether an understatement results from a bona fide inadvertent error is uniquely within the taxpayer’s knowledge,” it said.

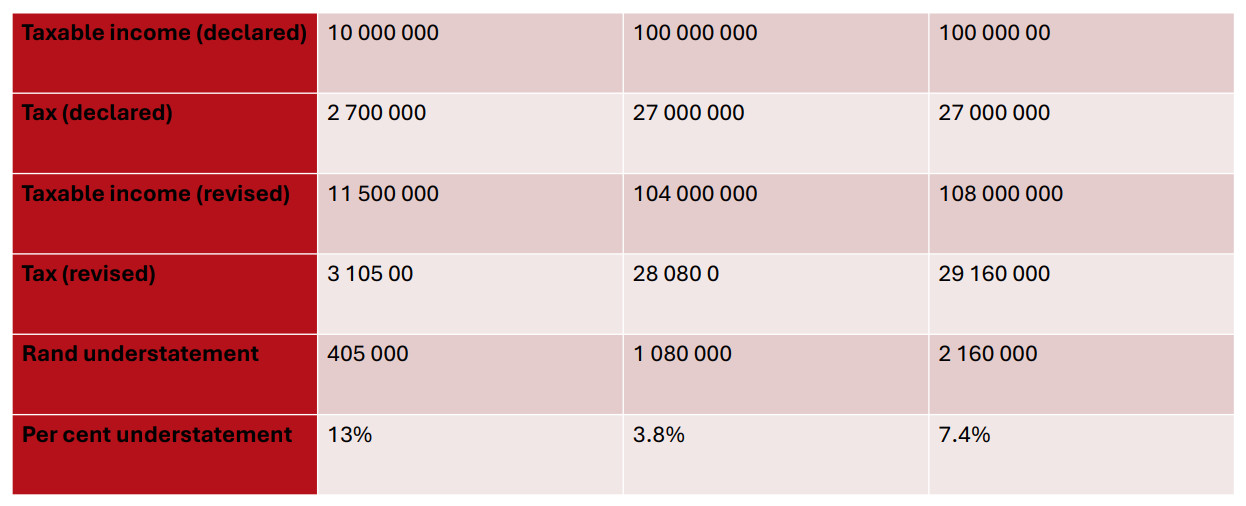

It provided examples of understatements:

In these examples, SARS only flagged circumstances where the understatement exceeded both 5% of the amount of tax properly chargeable and R1,000,000.

“Only in this example (does the) substantial understatement penalty apply,” it said.

The National Treasury said that it is willing to provide additional clarity in the amended definitions to allay concerns of commentators related to the current proposed amendments.