Reserve Bank gives its worst-case scenario for interest rates in South Africa

The South African Reserve Bank’s (SARB’s) Monetary Policy Review for April 2026 shows deep uncertainty around the war in the Middle East, with the bank’s “severe” case scenario pointing to interest rate backs at 8%.

Fortunately, this is not the SARB’s base-case scenario, which still assumes the war will be shorter in duration and that its secondary effects will simmer out within its forecast horizon (2028).

If this proves to be the case, South Africa will weather the choppy waters currently rocking global economies, and energy prices and inflation will simmer down by 2028.

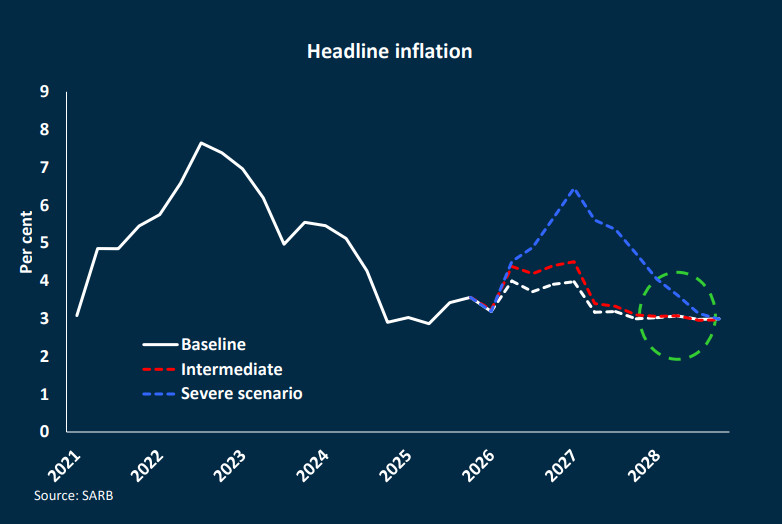

According to the SARB, the conflict between the United States and Iran in the Middle East has interrupted global disinflation and shifted the inflation outlook higher.

Prices for oil, gas, fertilisers and aluminium have risen sharply amid emerging supply shortages, and central banks around the world have halted rate-cutting cycles to wait and see what happens next.

The key issue is that uncertainty remains high regarding the conflict’s duration and intensity, the SARB said, while infrastructure destruction may delay supply normalisation even after hostilities end.

“Inflation pressures may also arise from countries replicating supply chains to strengthen resilience,” it said.

“With uncertainty elevated, global financial markets are likely to remain volatile.”

The bank noted that South African assets have also sold off amid risk aversion but have so far been relatively resilient, supported by improved macroeconomic fundamentals.

Because of this, spillovers from the shock are expected to affect but not derail South Africa’s transition to the 3% inflation target.

“Headline inflation is projected to rise this year but remain within the plus or minus 1 percentage point tolerance band and return to target by late 2027,” the SARB said.

Despite this, “uncertainty remains high, and the scale of second-round effects is difficult to quantify,” it said.

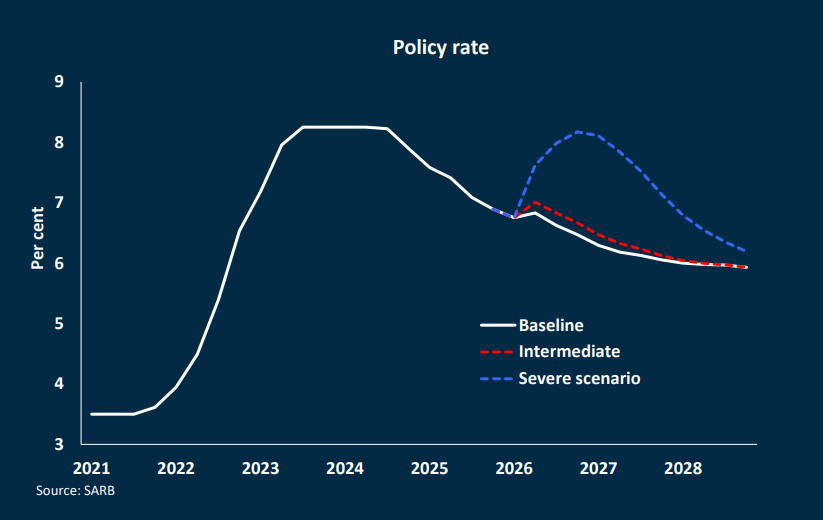

As a bottom line, the bank said that monetary policy will be more cautious, warning that “overall, interest rates are likely to remain elevated for longer”.

Three scenarios for oil, inflation and interest rates

The Reserve Bank presented three main scenarios for how it sees the war playing out.

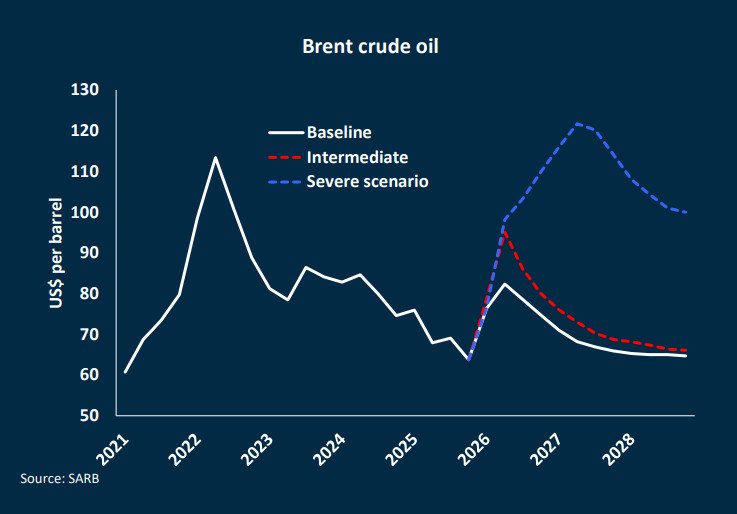

Broadly, the SARB’s baseline scenario—its current expectation—is for headline inflation to spike in 2026, though remain under 4.0% on a shorter war.

Inflation expectations are expected to continue deflating as various sectors look through the shocks, and the rand, while weakening against the dollar, maintains its resilience, trading around R17/$.

In this scenario, global oil prices average higher at $78 a barrel in 2026, but start easing, reaching $68 a barrel in 2027 and falling to $65 a barrel in 2028.

Interest rates continue to drop, albeit delayed to the end of 2026, with the nominal policy rate declining from 6.47% in 2026 to 5.93% in 2028.

From this baseline, the SARB’s scenario forecasts get much worse as it starts to factor in downside risks.

Intermediate scenario

The intermediate scenario assumes a short conflict of about two months, after which the Strait of Hormuz reopens, oil flows gradually normalise, and prices ease.

The risk premium is assumed to rise by 10% at its peak, and the rand to depreciate by about 5% at its peak, relative to the first quarter of 2026.

In the intermediate scenario, price pressures will rise relative to the baseline but will be less persistent, with inflation converging to the target by 2028, consistent with the SARB’s convergence horizon when the 3% target was announced.

The Quarterly Projection Model (QPM)-implied rate path indicates modest tightening.

Severe scenario

The severe scenario assumes a conflict lasting more than a year, significant damage to energy infrastructure across Gulf states, a prolonged closure of the Strait of Hormuz, and continued disruption in the Red Sea corridor.

Accordingly, energy-commodity prices are materially higher and more persistent.

The risk premium is assumed to increase by 20% at its peak, and the rand is assumed to depreciate by around 10% relative to the first quarter of 2026.

In the severe scenario, inflation is expected to be sharply higher, and the target will not be achieved within the forecast horizon, reflecting a larger and longer-lasting shock.

Second-round effects are stronger, and the risk of de-anchored inflation expectations is higher, requiring a more forceful policy response to prevent inflation from becoming entrenched.

Reserve Bank’s Scenarios

| Variable | Scenario | 2026 | 2027 | 2028 |

|---|---|---|---|---|

| Brent Crude Oil (US$) | Baseline | 78.00 | 68.00 | 65.00 |

| Intermediate | 85.00 | 72.00 | 67.00 | |

| Severe | 97.00 | 118.00 | 130.33 | |

| Headline Inflation (%) | Baseline | 3.70 | 3.33 | 3.02 |

| Intermediate | 4.05 | 3.58 | 3.01 | |

| Severe | 4.56 | 5.53 | 3.45 | |

| Nominal Policy Rate (%) | Baseline | 6.47 | 6.05 | 5.93 |

| Intermediate | 6.67 | 6.12 | 5.93 | |

| Severe | 8.17 | 7.13 | 6.19 |