This is how SARB determines which banks are most important in case of a financial collapse

The South African Reserve Bank (SARB) has published a new discussion paper looking at which banks are ‘systemically important’ in South Africa.

In a statement, SARB said that its primary objective is to protect the value of the currency in the interest of balanced and sustainable economic growth in South Africa.

It added that it had a mandate of protecting and enhancing financial stability in South Africa.

“Following the failure of several large international banks during the financial crisis that started in 2007, a high degree of public sector intervention was required by governments to restore financial stability,” SARB said.

“The significant economic, financial and social costs associated with these interventions as well as the resulting increase in moral hazard necessitated the implementation of additional measures to deal with the challenges that arose from the failure of global systemically important financial institutions (SIFIs).

“The objective of these policy measures is firstly aimed at reducing the probability that a SIFI will fail (e.g. through prudential regulation such as higher capital requirements), and secondly at making them more resolvable without having to use taxpayers’ money and without disrupting financial stability,” it said.

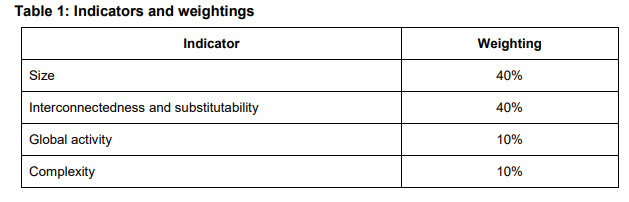

Methodology

The Reserve Bank said that it would use the following indicators to identify potential Domestic Systemically Important Banks (D-SIBs) in South Africa.

In addition, the discussion document notes that the Reserve Bank Governor will still have some additional discretion in these weightings.

This is because numerical methodology can never accurately reflect the real world, and there may be instances where a bank’s overall score underestimates its actual systemic importance, it said.

Size (40%)

According to SARB, the larger an institution:

- The more likely its failure will damage the economy, financial markets and confidence;

- The more difficult it will be to speedily replace its service offering; and

- The wider the potential impact will be on its clients, customers and employees.

A 40% weighting is given to the size indicator (compared to the 20% weighting given in the international methodology) due to the concentrated nature of the South African banking sector, the SARB said.

Interconnectedness and substitutability (40%)

The degree to which a financial institution is linked or connected to other parts of the financial system determines the channels through which, and the speed at which, any distress is spread to the rest of the system, the SARB said.

“Interconnectedness is measured through the bank’s exposure to other financial institutions and through its participation in the financial markets.”

The substitutability of a financial institution, together with the products and services that it provides, is another factor that can affect its systemic importance.

“The less substitutable a financial institution, the more systemically important it becomes, especially if the functions it performs are deemed to be critical to the functioning of the wider economy,” the SARB said.

“In the South African methodology, the interconnectedness and substitutability indicators were combined because there was a significant degree of overlap in the variables utilised to measure these indicators.”

Global activity (10%)

“The international impact of a bank’s failure and the complexity of resolving it vary in line with its share in the banking sector’s cross-jurisdictional assets and liabilities,” the SARB said.

“Accordingly, the higher a bank’s share in the cross-jurisdictional assets and liabilities, the greater the spillover effects will be.”

However, the SARB nored that South African banks’ cross-border operations do not carry the same systemic risk as those G-intenrational banks with a full global reach.

Therefore, the weighting assigned to this indicator was reduced to 10%, compared to the 20% weighting used in international weightings, the SARB said.

Complexity (10%)

The systemic impact of a bank’s failure is influenced by the complexity of its business model, organisational and group structure, and operating model, the SARB said.

“The greater a financial institution’s complexity, the more difficult it becomes to resolve the failure, and therefore the disruption to the financial sector could be more severe. In addition, the more complex a bank’s operations, the more difficult it becomes to assess its contribution to systemic risk.”

Within the South African context, the complexity indicator received a 10% weighting compared to the 20% weighting allocated by the international methodology.

The main reason for the lower weighting is that South African banks, in general, do not extensively engage in complex derivative and trading activities, the SARB said.

In addition, the indicators prescribed in the international methodology do not fully capture complexity in the South African context, and a degree of judgement would still be required.

Read: FNB detected ‘abnormally high’ debit order fraud in December and January