Absa feels the bite of South Africa’s stagnating economy as retail and corporate earnings take strain

Absa said Wednesday (11 March), that it recorded a ‘resilient performance’ for the year ended December 2019, considering the challenging macroeconomic backdrop.

However it saw a decline in its retail and corporate banking segments, as consumers and businesses alike felt the effects of the country’s stagnating economy, and credit impairments increased.

The group pointed out that South Africa’s GDP growth has consistently disappointed over the past five years. South Africa’s economy contracted in the third and fourth quarters by 0.8% and 1.4%, respectively – leading to the second recession in as many years.

The economy has been hit by short-term shocks, persistently weak business sentiment and periods of load shedding, it said, with GDP growth for full-year 2019 slowing to 0.2%, the weakest outcome since the 2009 recession.

Despite stagnant growth and challenging labour market conditions, household credit extension picked up gradually through the year, reaching 6.1% YoY in December, the bank said.

Headline inflation surprised on the downside in 2019 and reached a nine-year low of 3.6% YoY in November, reflecting weak demand and persistent slack in the economy, but picked up to 4.0% in December.

The South African Reserve Bank (SARB) reduced the repo rate by 25 bps in July 2019, citing the improved inflation outlook.

“The rand spent much of 2019 trading weaker, but recovered towards the end of the year to finish slightly higher as a favourable turn in global risk appetite helped offset a generally downbeat assessment of South Africa’s risks,” the lender said.

Absa said that it maintained balance sheet momentum, with underlying costs remaining well contained.

Group headline earnings grew 3% to R14.5 billion, and diluted headline earnings per share (HEPS) rose 3% to 1 747.6 cents.

The group’s RoE declined to 13.1% from 13.4% and its return on assets was 1.07% from 1.17%. Revenue, meanwhile, grew 5%, it said.

A final ordinary dividend of 620 cents per ordinary share was declared.

Absa disclosed International Financial Reporting Standards (IFRS) financial results and a normalised view, which adjusts for the financial consequences of separating from Barclays PLC, which is almost complete.

IFRS basis

- Headline earnings per share (HEPS) increased by 3% to 1 750.1 cents from 1 703.7 cents.

- The group declared a 1% higher full-year dividend per share of 1 125 cents.

- Diluted HEPS grew 3% to 1 747.6 cents from 1 700.4 cents.

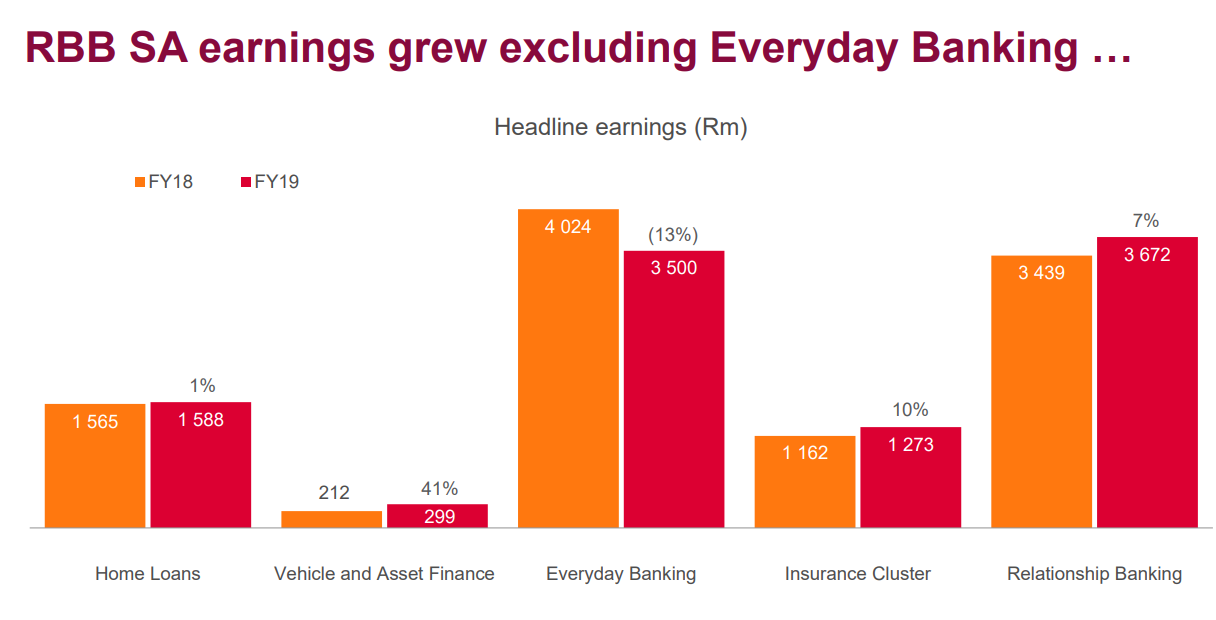

- RBB South Africa headline earnings declined 2% to R9.5 billion.

- CIB South Africa declined 6% to R3.2bn and Absa Regional Operations rose 16% to R3.6 billion.

- Return on equity (RoE) decreased to 13.1% from 13.4%.

- Revenue increased 5% to R80.1 billion and operating expenses rose 4% to R48.8 billion.

- Credit impairments grew 24% to R7.8 billion, resulting in a 0.80% credit loss ratio from 0.73%.

- Net asset value (NAV) per share rose 3% to 13 669 cents.

Normalised basis

- Diluted normalised HEPS grew 1% to 1 923.3 cents from 1 910 cents.

- Normalised earnings were 1% higher at R16.265 billion, up from R16.128 billion in 2018.

- RoE decreased to 15.8% from 16.8%.

- Revenue increased 6% to R80.0 billion and operating expenses rose 6% to R46.4 billion, resulting in a 58.0% cost-to-income ratio.

- Pre-provision profit increased 5% to R33.6 billion.

- NAV per share rose 5% to 12 605 cents.

Retail and corporate

Despite the overall growth, Absa’s Retail & Business Banking (RBB) saw headline earnings decline 2% to R9.51 billion – primarily due to 38% higher credit impairments, the group said.

Corporate and Investment Banking (CIB) South Africa’s earnings fell 6% to R3.23 billion, given 4% lower revenue. Total CIB headline earnings increased 3% to R5.95 billion, largely due to 48% lower credit impairments.

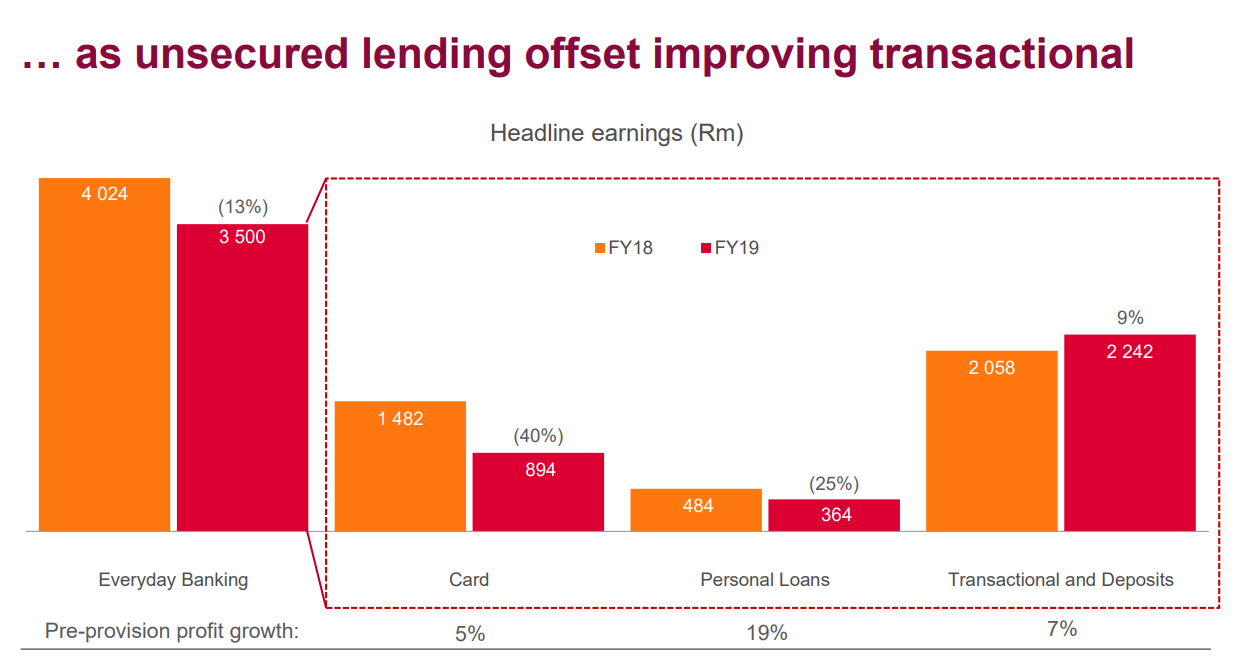

In the retail banking segments, division performance was mixed, with headline earnings decreasing by 13% in Everyday Banking. This includes a massive 40% decline in the card business and a 25% drop in personal loans.

However, transactional banking and deposit earnings grew 9%, the bank said.

Without providing any figures, the bank reported growth in both retail and corporate customers.

Prospects

Looking ahead, Absa projects 0.9% real growth for South Africa in 2020.

“We expect a continued difficult environment for the consumer, while heightened uncertainty will continue to dampen business confidence and investment.

“Downside risks are significant and include the risk of protracted load shedding, a sharper global slowdown due to the coronavirus outbreak and the impact of a potential sovereign credit rating downgrade from Moody’s,” the bank said.

The South African Reserve Bank decreased the repo rate by 25 bps in January and financial markets are currently pricing in a high probability of two further 25 bps rate cuts during 2020, Absa said.