Diamonds in South Africa are losing their sparkle

Diamond mining in South Africa, historically pivotal to the economy and livelihoods of many across the country, faces challenges as production recently hit a decade low.

Despite this downturn, reinvestments by the one of the biggest diamond companies in South Africa, and some developments in the electricity and logistics sector, offers hope for a resurgence.

South Africa, renowned for its significant role in diamond production, has a rich history with the trade dating back to 1867 when diamonds were first discovered near the Orange River, leading to a widespread rush and solidifying its prominence in the global diamond industry.

However, a recent analysis by The Outlier shows that the country’s diamond production has taken a dip.

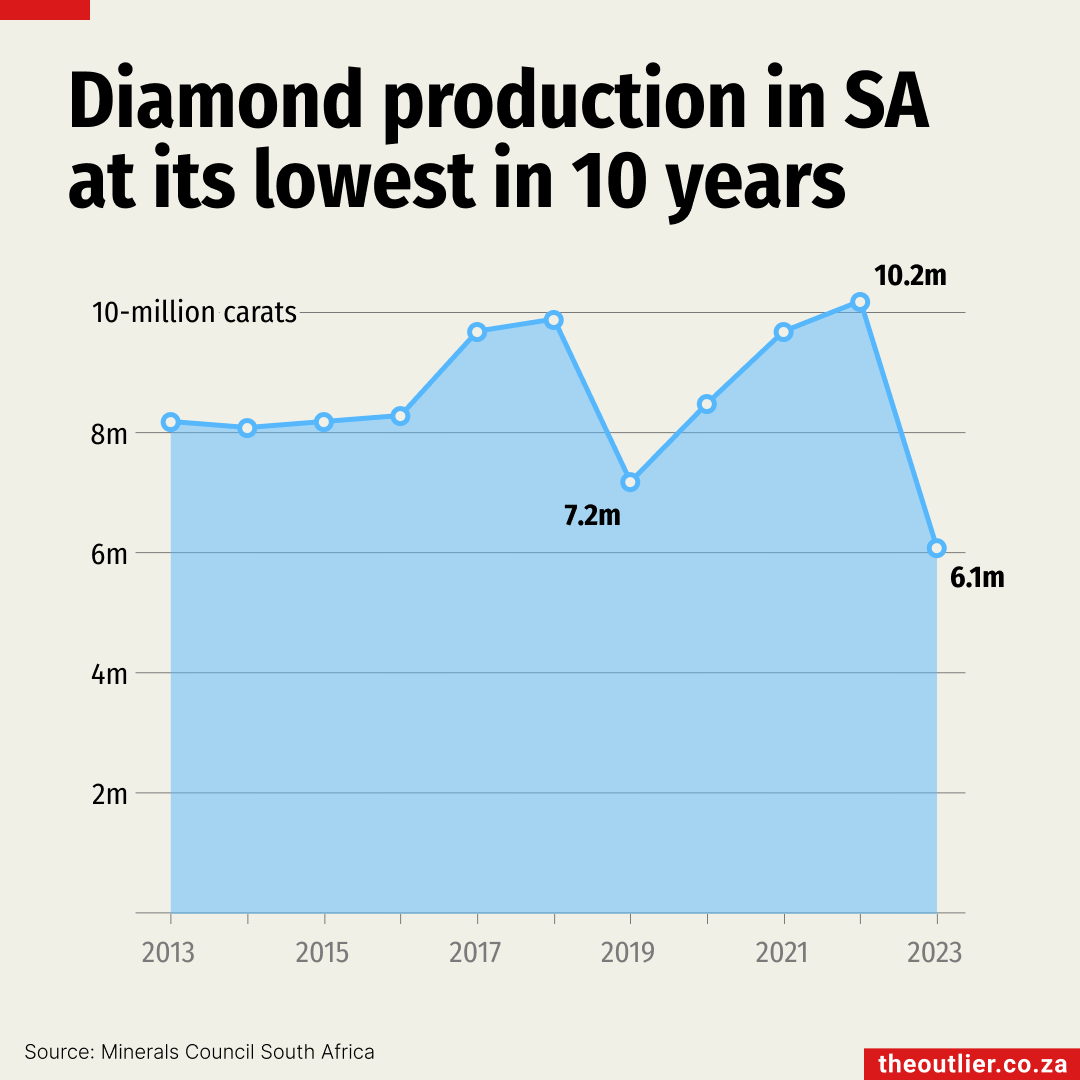

Before 2023, the country produced an average of 8.5-million carats a year, hitting a peak of 10.2-million carats in 2022 where sales amounted to R27.7 billion.

However, by 2023, production had dropped to 6.1-million carats.

There are numerous reasons given for the drop; however the key contributor for this is the fact that the De Beers’ Venetia diamond mine in Limpopo reached the end of its open-pit operations in December 2022.

According to the Mining Review Africa, until it ceased open-pit operations at the end of 2022, it contributed 40% of the country’s annual diamond production.

Additionally, the Minerals Council has said that there are various factors that continue to greatly hinder diamond mining in South Africa, which includes:

- Rising costs, particularly in salaries, wages, and electricity;

- The scarcity of water necessitates the continual development and implementation of water efficiency measures to reduce consumption in the industry;

- Lack of investment in diamond mining and emerging markets;

- The diamond mining sector experiences a skills shortage, making skilled employees essential for its sustainability;

- Synthetic diamonds boom pose a risk to the diamond mining industry.

Looking at the synthetic boom, while synthetic diamond production techniques continue to advance, the Minerals Council believes that natural diamonds are expected to remain the premium product.

This does not mean that the demand is not there. According to Statista, the market value of lab-grown diamonds amounted to more than $20 billion (R362.25 billion) in 2021 and is expected to grow to nearly $52 billion (R941.86 billion) by 2030.

Peter Major, director of mining at Modern Corporate Solutions, told Kaya Biz that the demand for natural diamonds and their supply are declining. “This is probably the scariest threat diamond mining has faced in the past 100 years,” he said.

Crucially, South Africa’s mining industry relies on the country’s infrastructure (roads and railway lines) in order to operate a streamlined business.

However, there have been numerous woes in this regard which have greatly inhibited this, particularly in rail volume. Transnet went from moving around 226.6 million tonnes along its rail in 2015, to just under 150 million tonnes.

However, recent developments in Transnet, such as selling rail slots to third parties or private sector players, among numerous others as part of a Recovery Plan, has meant that there has been an uptick in the volume handled by its railways and ports and its revenue – albeit below targets.

South Africa’s mining industry as a whole has been up against the ropes, with widespread job cuts becoming seemingly endemic in some mining companies attempting to stay afloat.

Recently, the Reserve Bank echoed much of what the Minerals Council said about the diamond sector, saying that the mining sector as a whole is continuing to be hampered by:

- High operating costs;

- A difficult policy environment;

- Inefficient rail and port infrastructure;

- Lower commodity prices (which are cyclical and are largely determined by events outside the country’s control);

- Electricity-supply disruptions.

Retrenchments and lay-offs have been prevalent in the South African mining industry of late, largely as a result of world prices for commodities such as platinum and diamonds remaining suppressed.

Earlier this year, PETRA Diamonds issued retrenchment notices to employees at its South African operations as it intensifies cost-cutting measures while forging ahead with the disposal of its stake in the Koffiefontein diamond mine.

Regardless, South Africa remains among the top 10 diamond-producing countries, contributing 5% of the world’s diamonds.

The largest producers are Russia with 37.3-million carats and Botswana, with an output of 25-million carats, according to 2023 Kimberley Process data.

An uptick can be expected, with De Beers’ development of an underground mine at Venetia to extend its operational life until 2045.

Although the open-pit operations are over, the company expects to extract 4.5 million carats of diamonds per year, and their goal is to achieve a fully automated underground mine by 2027.

Back in 2013, De Beers announced that it would invest US$2.3 billion dollars in the Venetia Underground Project, marking the single biggest investment in the country’s mining sector in decades.

“While diamond mining has been taking in place in South Africa for almost a century and a half, the country’s diamond sector is far from reaching the end of its life,” said the Minerals Council.

“Developments at the country’s three largest mines are designed to expand their outputs and to extend their lives to anywhere between a quarter and a half a century,” it added.