South African investment legend backs struggling retailer

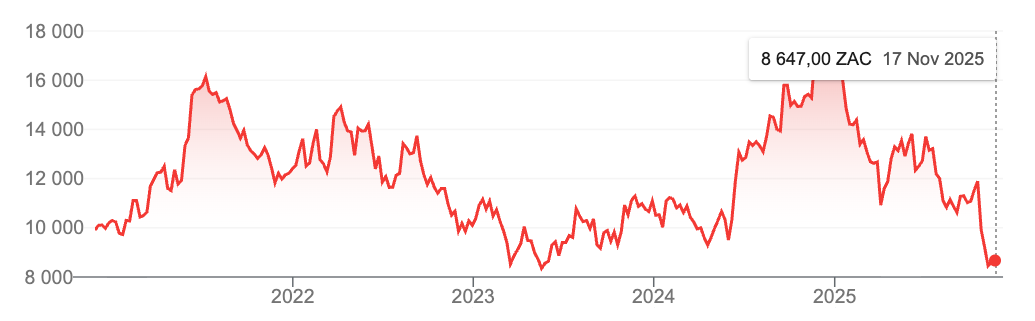

The Foschini Group (TFG) has experienced a significant decline in its share price in recent weeks, but investment legend David Shapiro of Sasfin Securities remains incredibly bullish on the stock.

In August, TFG held a Capital Markets Day, during which the company’s management team painted a rosy picture of South Africa’s prospects.

Management said that TFG was outperforming the market via consistent share market gains and category leadership.

There was also sustainable growth via organic expansion, strategic acquisitions, and diversification.

However, a trading statement published in October 2025 saw the group report relatively weak results.

When recently acquired White Stuff was excluded, sales only rose by a subdued 3.5% over the six months ending 30 September 2025.

This caused a sharp decline in the company’s share price immediately following the release of the trading statement.

Shane Watkins, Chief Investment Officer at All Weather Capital, stated that the reason for the decline was not due to a poor trading statement.

Watkins explained that the drop was due to the unexpectedly bad result, considering what management had told institutional investors during the capital markets day.

TFG’s management team painted a more rosy picture of TFG’s results, and did not communicate the challenges the company was facing in South Africa, the UK and Australia.

The poor trading environments in all three countries were reflected in the official interim results published on November 7, 2025.

Basic earnings per share (EPS) decreased by 21.0% to 290.8 cents, and headline earnings per share (HEPS) decreased by 21.3% to 292.6 cents in the interim results.

The group also cut its interim dividend by 18.8% to 130.0 cents per share (Sept 2024: 160.0 cents per share).

Shapiro is optimistic

Speaking with Business Day TV, Shapiro was shocked by the performance of TFG’s stock, which had declined by around 50% over the past few weeks. This has brought the stock to levels seen five years ago.

He said that the company is facing some balance sheet struggles, including being overgeared.

However, he highlighted that the company has good brands, strong management, a nationwide store network and a diversified base. He thus believes that the stock is incredibly well-valued.

Shapiro is also bullish on the market and believes that the stock market is set for a strong year. He said that TFG is his “punt of the year,” with the company set to see a recovery in its share price.

Although he warned that the stock could go further down with stores forced to close, he doesn’t believe that this will happen.

The current data on TFG supports Shapiro’s view, with the company having a price-to-earnings ratio of 10 and a dividend yield of over 4%. These point to an undervalued stock.

The TFG board also seems to believe that the share is trading at a discount and has initiated a massive share repurchase.

The company is looking to repurchase R1.0 billion in shares, and had repurchased R377 million in shares by 30 September 2025.

| Metric | Interim Results |

| Group revenue | Up 12.2% to R31.4 billion |

| Group sales | Up 12.7% to R29.2 billion (3.5% excluding White Stuff) |

| Group gross profit | Up 12.3% to R14.4 billion |

| Group gross margin | Contracted 20 bps to 49.3% |

| Operating profit | Down 9.9% to R2.3 billion |

| Basic EPS | Down 21.0% to 290.8 cents |

| HEPS | Down 21.3% to 292.6 cents |

| Interim dividend | 130.0 cents per share (Sept 2024: 160.0 cents), down 18.8% |

| Share buyback | 3,420,485 shares repurchased for R377 million as at 30 Sept 2025 |