Iconic 90-year-old company in South Africa goes from hero to zero

Analysts say South African pulp and paper group Sappi risks a $2 billion (~R32 billion) debt spiral as its losses mount.

Speaking to Business Day TV, All Weather Capital Chief Investment Officer Shane Watkins and PSG Wealth Manager Ricus Reeders raised major red flags with Sappi’s balance sheet and debt position.

Sappi was founded in 1936 as South African Pulp and Paper Industries Limited, later abbreviated to SA Pulp, and then to Sappi.

The 90-year-old group started out manufacturing paper from straw, but has since grown into a global woodfibre company with operations in 150 countries.

It focuses on dissolving wood pulp, packaging and speciality papers, graphic papers, as well as biomaterials and biochemicals.

However, the group has suffered significantly over the past few years, going from record profits amid a boom in demand for its products circa 2022 to major losses in its most recent reporting periods.

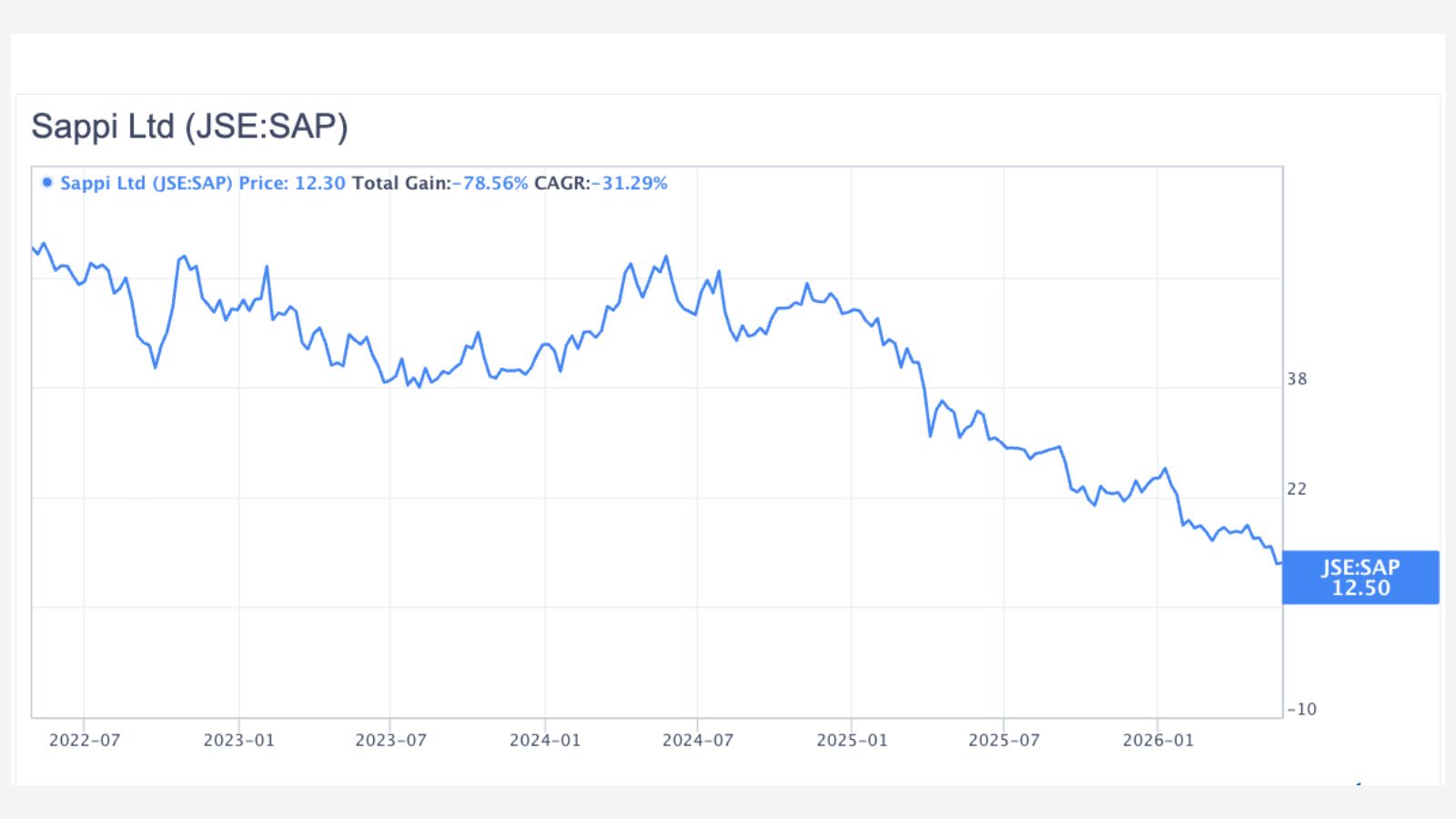

Over the period, the group’s share price has tanked, dropping from R59 a share in May 2022 to R12.60 in May 2026—a 78% decline, wiping out R20 billion in market value.

The group currently has a market cap of R7.5 billion, but was at about R28 billion in 2022.

The company has attributed the downturn to the prevailing operating environment, which it says remains challenging.

This includes a weak global macroeconomic backdrop and persistent geopolitical and trade tensions, which are undermining market confidence and consumer demand.

The group published its Q2 FY26 financial results for the period ended March 2026 in May, recording a loss of $413 million for the period.

This was significantly higher than the $20 million loss a year before. Revenue for the period was flat at $1.33 billion.

Concerningly, the group saw a notable uptick in net debt, which grew 17% to just under $2 billion (~R32 billion).

The group’s net-debt-to-Adjusted-EBITDA ratio increased to 6.1 times, which prompted it to renegotiate its covenants.

“Given the continued difficult and uncertain market conditions and elevated volatility, we proactively negotiated a suspension of the leverage covenant testing until March 2027,” it said.

The renegotiation was unanimously supported by its banking group, but the rollover has raised major red flags with analysts and portfolio managers.

Analysts warn of a downward spiral

According to All Weather Capital’s Shane Watkins, Sappi’s biggest issue isn’t necessarily its income statement, but rather its balance sheet, with the net debt a significant issue.

Watkins said that investors either look at companies from an income statement perspective, looking at the earnings, or they look at the balance sheet concerning the risk.

“The issue in Sappi is less about the income statement, and it’s more about the balance sheet. They’ve got $2 billion of interest-bearing debt,” he said.

He flagged that the company’s market cap is $500 million, meaning 80% of its enterprise value is debt.

Because of a declining market cap and debt not being paid down, this suggests that there is a very real risk that the group will have to go to market to raise capital.

“Every time you have to roll over this debt in a higher interest rate environment, the banks are going to demand a higher interest rate, which in itself exacerbates the problem,” he added.

“They could get into a very negative downward spiral where they have rising interest rates, and they are simply not able to service that debt, and then you’ve got to raise equity.”

He stressed that this may not be the case in reality, but it is a real risk that investors would want to take into account.

PSG’s Ricus Reeders echoed similar sentiments, noting that “if your operational environment isn’t helping you to pay off that debt, you’re in a bind.”

“How else are you going to do it, except for possibly going to the market and raising capital? It is the worst possible time in the market to do that,” he said.

Both analysts said it isn’t the end for Sappi, but were more bearish than the group’s CEO, Stephen Binnie, on its prospects.

“I think it probably will (survive), and it will have its time, but it’s not right now,” Reeders said.

Commenting on the group’s quarterly results, Binnie acknowledged challenges, but noted that the group was ramping up operations in the United States.

“We think that’s going to create a great platform for long-term growth,” he said.

He acknowledged the company’s debt issue but assured that the group had a strong focus on paying it down. However, this was at the cost of capital investments, he said.

“I think it’s going to be a progressive improvement…We are ramping up on volumes, particularly in the US, and that will deliver improved profitability as we go into 2027,” he said.

Sappi share performance 2022-2026