Mr Price CEO earns R52.6 million – 843 times more than the lowest-paid employee

Mr Price CEO Mark Blair earned R52.6 million in total remuneration for the 2026 financial year, despite the group’s share price tanking after the deal to acquire NKD was announced.

Blair’s R52.6 million, which included R10.1 million in total guaranteed pay (TGP), is 843.4 times higher than the R63,000 earned by the company’s lowest-paid employees.

Mr Price has started reporting the pay disparity between the highest- and lowest-paid employees at the company, following the effective implementation of part of the Companies Amendment Act.

The new sections of the Act, which came into effect in late May, require specific wage gap disclosures amongst listed and state-owned companies.

In line with the law, Mr Price has now had to disclose the total remuneration for its highest- and lowest-earning employees, as well as the average and median remuneration.

The new law comes amid heightened scrutiny of executive pay in South Africa, given the nation’s massive income inequality and questionable performances of state-owned and listed companies.

The company’s average total remuneration for its employees stood at R158,000 per year. However, the median, which is not skewed upwards due to higher earnings, stood at just R82,000.

The ratio of the companies’ top 5% to bottom 5% of employees across total remuneration stood at 19.

The remuneration disclosures include information on 27,472 employees at the group, but exclude learners and interns.

The total remuneration figure also includes bonuses, dividends, and long-term incentives settled during the year.

Mr Price said that its remuneration was annualised and normalised to a uniform monthly working hours where applicable.

| Mr Price Remuneration Stats | Total Guaranteed Package | Total remuneration |

| Highest-paid employee | R10,117,000 | R52,570,000 |

| Lowest-paid employee | R63,000 | R63,000 |

| Average remuneration of employees | R140,000 | R158,000 |

| Median remuneration of employees | R79,000 | R82,000 |

| Ratio of top 5% vs bottom 5% of employees | 14 | 19 |

Fallout over NKD deal

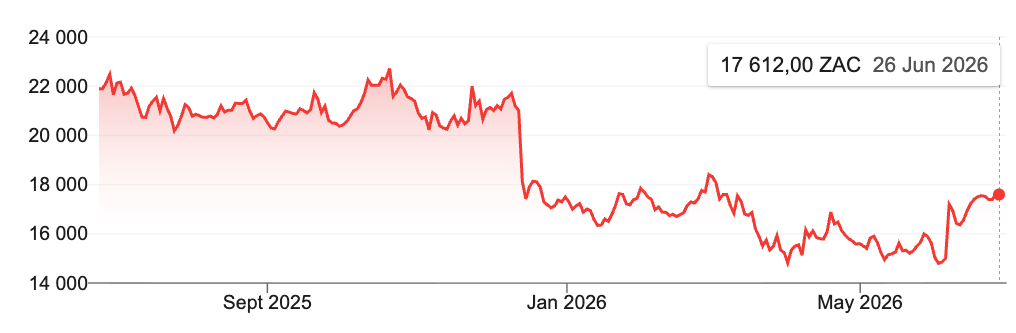

The massive pay disparity comes amid a significant drop in Mr Price’s share price following the acquisition of European retailer NKD.

The deal was valued at €487.00 million (about R9.6 billion in December when the deal was announced) and was funded by a combination of cash and debt.

NKD has over 2,000 stores in Germany, Austria, Italy, Croatia, Slovenia, the Czech Republic, and Poland. The company generated net sales of €684.57 million in 2024.

The reaction to the deal was largely negative, with R6 billion wiped off Mr Price’s market cap on the first day of trading.

Analysts were concerned about NKD’s relatively weak financials, including low profit margins, as well as the massive amount of debt Mr Price was taking on for the deal.

Mr Price’s balance sheet now includes R7 billion in interest-bearing loans following the acquisition.

While the group’s share price has risen somewhat since its strong financial yearly results were announced, it is still down roughly 20% year over year.

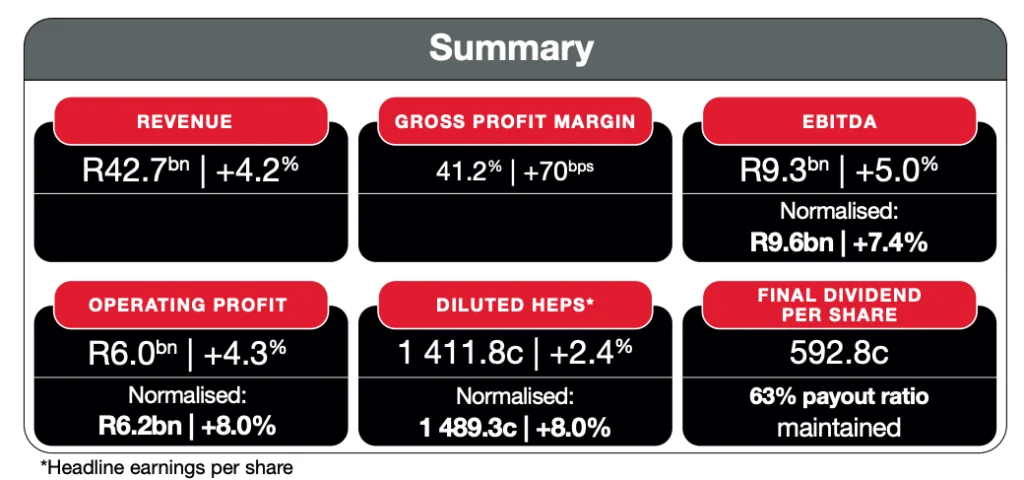

For the 52 weeks to 28 March 2026, Mr Price Group increased total revenue by 4.2% to R42.7 billion, but its earnings were impacted by once-off transaction-related costs relating to the NKD deal.

When using normalised figures, which exclude those costs, basic, headline and diluted headline earnings per share increased by 8.0%, 7.7% and 8.0%, respectively.

On a statutory basis, basic, headline and diluted headline earnings per share of 1,449.5 cents, 1,453.9 cents and 1,411.8 cents, increased by 2.3%, 2.1% and 2.4%, respectively.

The group also declared a final dividend of 592.8 cents per share, maintaining a pay-out ratio of 63%.

Although the group said household income improved in 2025, the discretionary retail sector was not an immediate beneficiary of this improvement, whereas the prior year’s results benefited from the two-pot system.

Despite the challenging year, the group still opened 196 new stores. For FY2027, the group will invest R1.1 billion in capex in South Africa, with 180 new stores planned.

Due to the rise of structural debt, the group noted that it will focus on balance sheet and treasury management.

In Europe, NKD’s capital expenditure is forecast at €24m (R454 million) and incorporates about 150 new stores.