The dark side of Eskom’s miraculous turnaround

The latest utility-scale power generation statistics in South Africa, compiled by the Council for Scientific and Industrial Research (CSIR), show that Eskom has staged a miraculous turnaround in 2025.

However, the utility’s tariffs have been surging above inflation for more than a decade, pushing customers away as it gradually prices itself out of the market.

The CSIR report covers utility data from 1 January to 30 June 2025, and provides a detailed analysis of load shedding and energy availability during this timeframe.

As many in South Africa would have experienced first-hand, load shedding was significantly reduced this year, with only 749 GWh shed from the grid, compared to 4,126 GWh in 2024.

This is a reduction of 82%, reflecting a pretty miraculous turnaround and improved power system performance and supply availability from a utility that was on the brink just two years ago.

According to the CSIR, the turnaround is a function of three key factors.

Firstly, Eskom’s generation capacity is up.

Installed capacity increased by 720 MW in the first half of 2025 compared to the same period of 2024; therefore, energy generated from coal is relatively higher, and additional capacity was added from independent wind and concentrated solar power (CSP) producers.

Eskom’s capacity is expected to continue to ramp up in the remainder of the year as Kusile units reach commercial operation.

Secondly, Eskom’s power plant reliability has improved.

The Eskom fleet energy availability factor (EAF) marginally improved in the first half of 2025 compared to the previous year and reached an annual average of 58%, which is 1% higher than the 57% reached in the same period of 2024.

Since mid-year, EAF has continued to rise, with the utility hitting over 70% in September and reaching its best performance peak in four years.

The third factor at play is that Eskom’s peak demand is down.

“Electricity demand continues to trend down; peak demand is 3% lower in the first half of 2025 compared to the peak demand recorded in the first half of 2024,” the CSIR said.

This reflects a move away from Eskom by customers, moving to energy alternatives. The CSIR said this was mostly due to the sustained growth of the private sector embedded generation.

“A combination of lower electricity demand, new generation capacity and a gradual increase in Eskom’s EAF helped to reduce the impact of load shedding,” the CSIR said.

However, the group did note that the utilisation of diesel generators nearly doubled from an average of 7% in the first half of 2024 to 12% in the same period of 2025, which has also contributed.

Electricity prices are bleeding South Africans dry

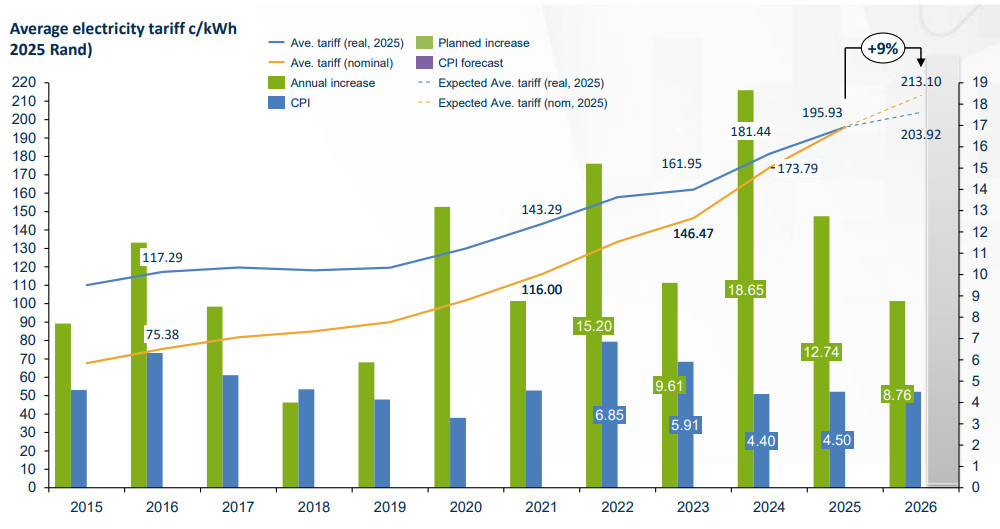

Another crucial factor hitting demand is higher electricity prices, which are pushing customers away.

The CSIR noted that Eskom’s tariffs are going up and exceeding inflation, with the national average tariffs having risen 190% since 2014.

“Increases in the price of electricity prior to 2008 were mostly below inflation. Electricity prices increased significantly in 2008, which coincided with the start of load shedding,” the CSIR said.

The national average electricity tariff increased by an average of 10% per year from 2014 to 2025, compared to an average inflation rate of 5.2% over the same period.

With the projected 2026 hike of 8.76% again exceeding the 4.5% Consumer Price Index forecast, the trend is not slowing down.

Notably, the CSIR pointed out that Eskom’s electricity tariffs are now above the utility‑scale solar photovoltaic levelised cost of electricity.

The implemented NERSA tariff increase of 12.74% this year takes the average tariff to c/kWh 195.93. The proposed tariff escalation of 8.76% will increase the national average tariff to 213.92 c/kWh in 2026.

This is compared to the levelised cost of renewable generation resources, which range between 50 c/kWh and 60 c/kWh for solar PV and wind utility-scale power plants in the REIPPP programmes, the CSIR said.

Eskom’s sharp tariff hikes have been widely criticised, and the resultant impact on the economy is being factored in to everything from inflation forecasts to the Reserve Bank’s interest rate moves.

Producer price inflation data out this week flagged the 2026 and 2027 tariffs as sore points for producer costs, likely to push prices higher next year.

Consumers will face a double-blow, having to suffer the direct costs of the price hikes as well as the higher costs of goods and services as PPI feeds into CPI.

At its latest meeting, the Reserve Bank flagged the “dysfunction” in administered prices like electricity as a risk factor for inflation, and thus its longer-term view of policy decisions.

With Eskom’s price hikes likely to push inflation higher in 2026, the Reserve Bank is more cautious about cutting interest rates. However, the longer-term view is to look through the expected spikes and work towards reaching the new “preferred” 3% target.