South African households have a R2.4 trillion problem

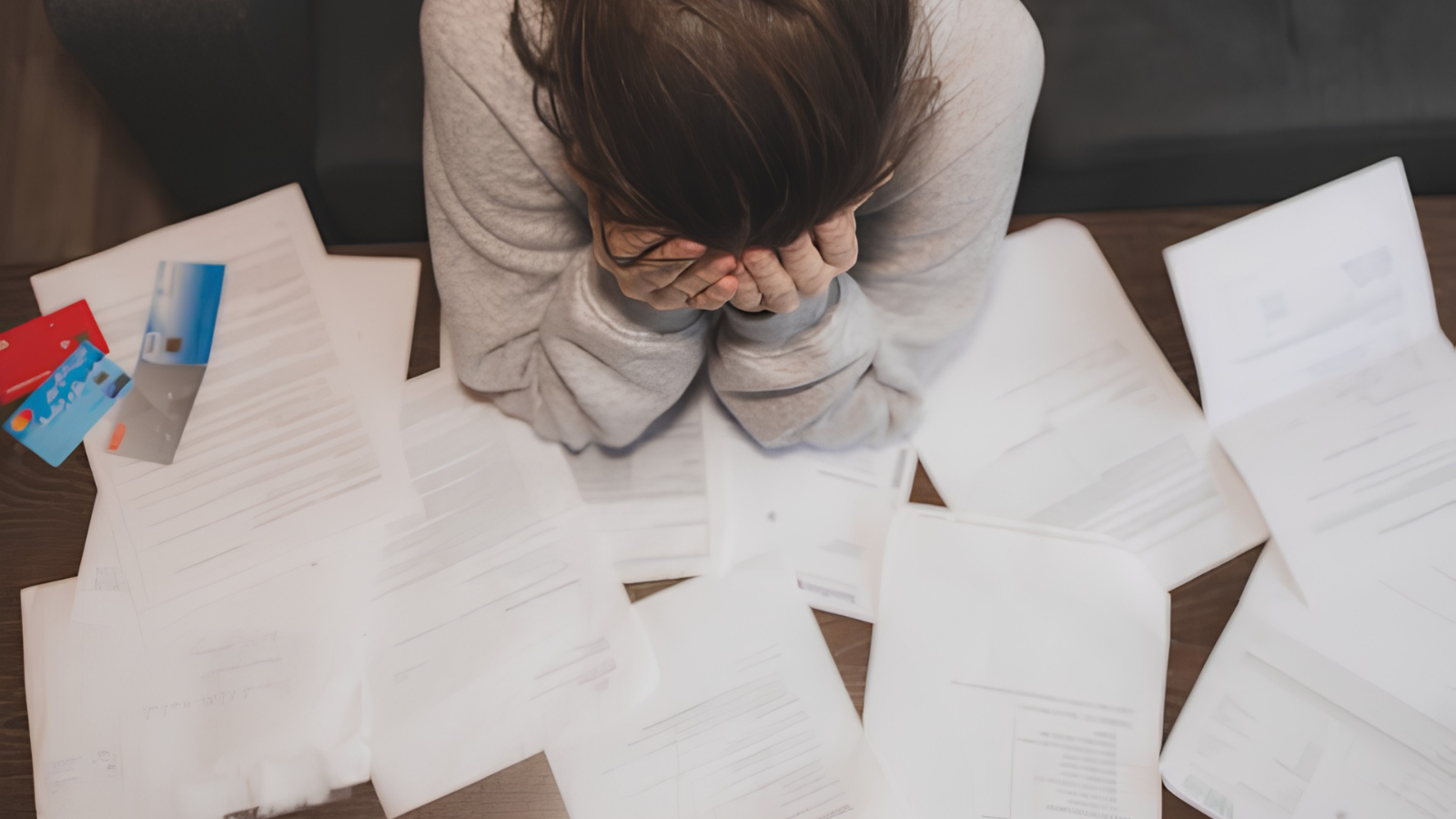

South Africa’s household debt burden has reached an alarming R2.4 trillion, and according to experts, its impact extends beyond bank statements and credit records.

National Debt Advisors said this burden is now evident in the physical and mental health of individuals, manifesting as sleepless nights, anxiety, panic, shame, and the stress of living under constant pressure from creditors.

National Debt Advisors Head Sebastien Alexanderson said that South Africa is misdiagnosing the crisis.

Financial distress, he said, appears as a financial issue, is experienced as a health concern, and is often misclassified as a mental health matter in isolation.

“The medication is treating the output. Nobody is treating the input. And the input is a credit environment that has put their entire nervous system on high alert, sometimes for years,” Alexanderson said.

According to the National Credit Regulator, 4.9 million consumers have impaired credit records, indicating poor credit histories.

Additionally, 6.3 million are in early-stage arrears. Household debt is currently at R2.4 trillion.

An impaired credit record indicates that your financial history contains missed payments, defaults, or judgments.

This negatively impacts your credit score, making it more difficult or costly to obtain loans or credit cards.

To rebuild your credit, Standard Bank recommends checking your credit report, paying off any overdue debts, and avoiding new debt.

Alexanderson said that the most significant damage is not represented in any official records.

“Nobody counts the panic attacks. Nobody counts the marriages that ended because of the financial stress. Nobody counts the children who grew up watching their parents flinch every time the phone rang,” he said.

For many households, debt is no longer just a financial issue; it has turned into a daily psychological struggle.

Individuals often experience insomnia, chest tightness, avoidance behaviours, irritability, shame, secrecy, and dread as the month-end approaches.

Financial debt leads to physical stress

Research from the University of Pretoria’s psychology department has shown that when creditor pressure is alleviated, there are measurable improvements in anxiety and depressive symptoms among those who are over-indebted.

This finding aligns with the experiences of debt counsellors, who regularly witness similar changes.

An existing legal framework addresses this problem. Under Section 86 of the National Credit Act, once a consumer submits a debt review application, credit providers are legally obligated to stop enforcement actions and direct contact.

Alexanderson stated that those most in need of protection are often the least likely to be aware of its existence.

“In 15 years of debt counselling, I have never met a client whose anxiety disappeared while the collection calls were still coming. You cannot heal in a warzone,” he said.

Alexanderson said that when patients experience anxiety, insomnia, or stress-related symptoms, debt may not simply be incidental; it could actually be the root cause.

In many instances, he said the issue requires legal intervention. “Debt is not a moral failure. It is a circumstance,” he said.

Below is a list of points for South Africans who feel that financial stress is impacting their physical or psychological well-being.

- View symptoms as data, not flaws: Waking up at 03h00, experiencing chest pain before the end of the month, and avoiding phone calls are responses to stress, not signs of weakness.

- Communicate fully with your GP: If you are being treated for anxiety or insomnia, inform your doctor that financial stress is a primary cause of your symptoms.

- Know your rights as a debtor: Creditors cannot legally call you at unreasonable hours, contact your employer, or use coercive language, all of which are prohibited under the National Credit Act (NCA).

- Understand Section 86: Filing a debt review application will legally stop enforcement actions and direct contact from debt collectors immediately.

- Don’t keep secrets: Concealing the extent of your debt from your spouse is a significant predictor of marital breakdown, according to the cases handled by Alexanderson.