5 JSE stocks investors have eyes on right now

Five prominent South African investment analysts and portfolio managers have selected five local companies that offer excellent prospects and future value – Standard Bank, OUTsurance, MTN, Siemens, and Anglo American.

The investment analysts and portfolio managers are:

- Mark du Toit from Oyster Catcher Investments;

- Ashley Daswa from Sanlam Investments;

- Jonathan Fisher from PSG Wealth Sandton Grayston;

- Rowan Williams from Nitrogen Fund Managers; and

- Jacobus Brink from Novare

The companies have been selected for their attractive share price and encouraging prospects for medium to long-term investors.

The five local stocks you should consider, explaining why these investment professionals find these companies to be a good buy, are listed below.

Standard Bank

Standard Bank Group Limited is a major South African bank and financial services group and is Africa’s biggest lender by assets.

Du Toit said Standard Bank offers good value in 2023 as it now wholly owns Liberty, allowing the group to reorganise its capital stack – meaning it’ll have more capital to inject into the business.

The bank also has a lot of space for cost optimisation, as the market has seen with Nedbank.

Over the past year, Standard Bank showed returns of around 15%, outperforming both the industry average and the South African market – which returned 2.3% and -5.8%, respectively.

Prospective investors can expect a continued return of around 15% from Standard Bank over the next few years.

At its current trading price of R177.97, Du Toit added that the stock is currently trading at 21.8% below its historical high, and one could expect a dividend yield of between 7% and 8% – which offers a great return on your investment.

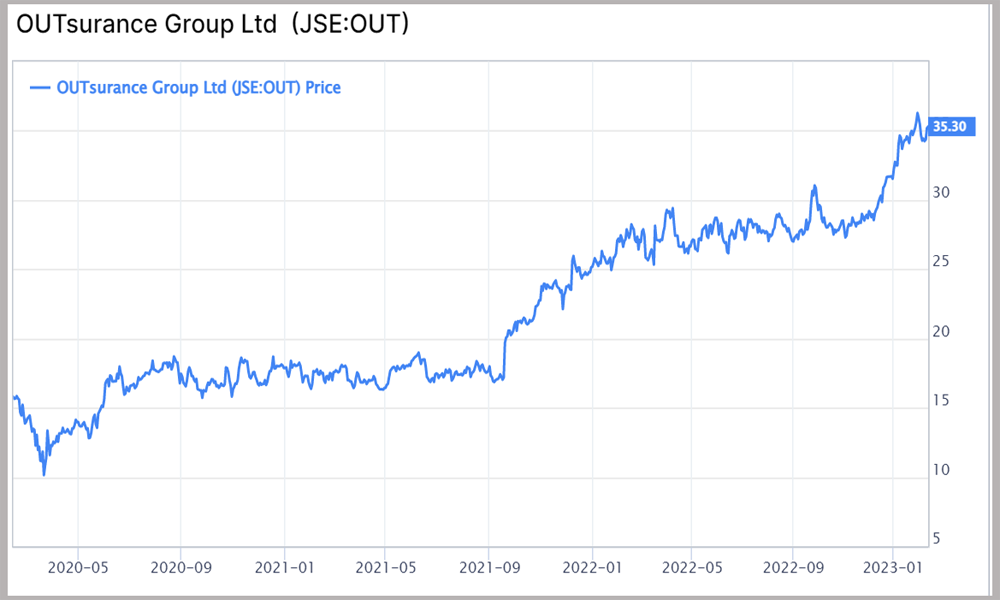

OUTsurance

OUTsurance Holdings Limited, commonly referred to as OUTsurance, is a subsidiary of OUTsurance Group Limited, a South African-based financial services investment holding company.

Daswa said the group looks promising, with a strong management team that recently executed the company’s transition and rebrand from Rand Merchant Investment Holdings (RMI).

OUTsurance also has enough cash to cover all of its debt, and its financial situation is stable.

The group’s price-to-earnings ratio is also close to its 10-year low of 2.35, while its stock dividend yield is close to a 1-year high.

OUTsurance’s share price is currently trading at R35.3, which is 3% below its historical high – offering a current dividend yield of 2.4%.

MTN

MTN is a South African multinational mobile telecommunications company that operates in many African countries and holds a 37% market share in South Africa.

The Group’s revenue has grown by 152.2% over the past year, with an earnings forecast of around 16.5% per year in the near term.

Based on its latest financials, Fisher believes that the business is showing resilience in a dampened economy, with a turnover growth forecast in the mid-teens.

He added that MTN is also looking to drive its return on equity up to around 25% in 2023.

Fisher believes MTN is performing exceptionally, noting that expectations of an increase in headline earnings of 30% for the full year’s financials are still underplaying it.

MTN is currently trading at R144.4, and some estimate this to be 58.9% below its fair value, with Fisher adding that PSG currently values the share at around R218.

The group also indicated a dividend of at least R3.30 a share – making it a very attractive buy.

Super Group

Super Group Limited provides logistics and supply chain management services throughout South Africa.

The Group provides truck rental, third-party distribution services, cross-border transport, freight management, and trading operations – with a big portion of its operations in Australia.

Williams believes that Super Group offers a great opportunity for buyers as the rand has weakened, making the group quite defensive in its earnings.

He added that its latest financials are also in good standing, with earnings up over 30% over the past year.

Super Group is currently trading at R32 and has increased year-to-date by 19.3%, outperforming the all-share and the top-40 indices by 10.1% and 1.7%, respectively.

Anglo American

Anglo American is a British-listed multinational mining company and the world’s largest producer of platinum, accounting for about 40%, and is a major producer of diamonds, copper, nickel, iron ore and steelmaking coal.

The company showed a solid performance in its latest financials, and Brink noted that it’s well-diversified, with operating margins expanding – which is a really good sign.

Anglo American is currently trading at R702 per share, which is close to 15% below its historical high – with a forward PE of just over 9 times.

Brink believes the company is a really good buy in February 2023, offering a forward dividend of 4.3%.