What to expect from the South African Reserve Bank in 2020

It was the year central banks jumped back into the fray, cutting interest to deal with a slowdown driven by a trade war and subsequent decline in manufacturing.

Some, like the Federal Reserve, had at least made some headway on rate hikes before 2019, creating room to loosen amid the weakest growth since the financial crisis. But others, like the European Central Bank, found themselves in a more difficult position and had to cut benchmarks further below zero, stoking resentment about subzero rates.

2020 looks like it might be a quieter year for monetary policy. Fiscal may take up some of the lifting work, and growth prospects are looking a little brighter.

The economic numbers are mostly mixed rather than positive, though. On balance, the monetary policy bias still leans to the dovish side. While the big guns are set to hold fire, others, especially in the emerging markets, are projected to cut again.

What Bloomberg’s Economists Say: “A moment of calm in the global economy is obscuring a serious challenge for the world’s central banks. Low rates for most and negative for some means policy space is severely depleted. We don’t think the next downturn is coming in 2020. When it does come, central banks won’t have all the answers.” — Tom Orlik

Here is Bloomberg Economics’ quarterly review of 23 of the top central banks, which together set policy for almost 90% of the global economy:

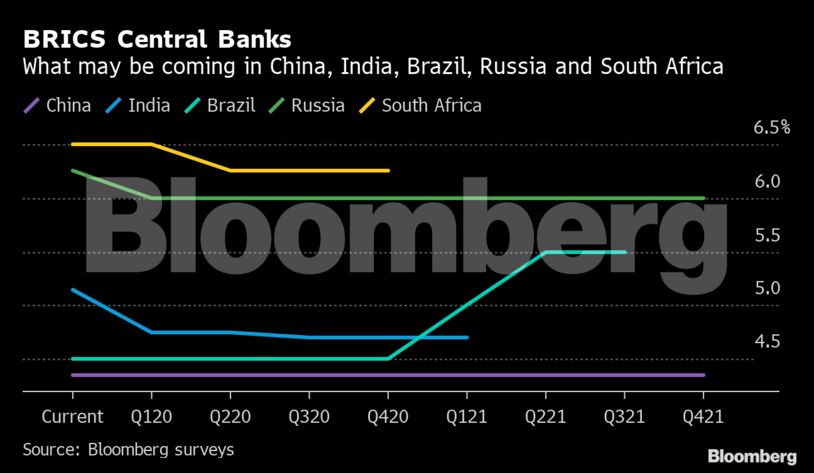

Here is the focused review of the BRICS banks, including South Africa:

BRICS banks:

South African Reserve Bank

- Current repo average rate: 6.5%

- Forecast for end of 2020: 6.25%

The South African Reserve Bank is facing pressure to ease after the economy unexpectedly contracted in the third quarter and power cuts raised the risk of a second recession in as many years. Inflation is at a nine-year low and close to the bottom of the target range of 3% to 6%.

Still, the Monetary Policy Committee has made it clear that some of the factors weighing on economic growth — such as policy uncertainty and the deterioration of government finances — will probably prevent it from cutting rates. Using monetary policy to compensate for government failures “is not the way forward,” Governor Lesetja Kganyago said at the final MPC meeting of 2019.

The prospect of the country a losing its last investment-grade credit rating at Moody’s Investors Service in 2020 may also prevent easing. While the move is largely priced in, it’s likely to weaken the rand. A downgrade could result in a selloff of between $5 billion and $8 billion of South African bonds, Deputy Governor Kuben Naidoo said.

People’s Bank of China

- Current 1-year best lending rate: 4.35%

- Current 7-day OMO reverse repo rate: 2.50%

- Forecast for end of 2020: 4.35%: 2.35%

Analysts predicting the start of large-scale monetary easing by the People’s Bank of China in 2019 were persistently disappointed, and Governor Yi Gang has indicated he intends follow the modest, targeted path for stimulus in 2020. That said, if weakness in the world’s second-largest economy worsens, then economists expect the central bank to continue to release cash into the system via cuts to the reserve ratio, as has been a preferred method to shore up output this year.

The cautious approach to easing is determined by China’s current battle with a form of stagflation — consumer price gains driven beyond the PBOC’s target of 3% by food coupled with factory prices in decline. Economists currently forecast economic growth to slow below 6 percent next year, a development that Communist Party leaders seem comfortable with. A recent revision to 2018 GDP data means that the long-standing goal to double the size of the economy this decade is more easily in reach. That lifts some of the burden on the PBOC to artificially boost the expansion.

What Bloomberg’s Economists Say: “The People’s Bank of China is pushing down lending rates steadily and incrementally. The drop in the one-year LPR in November underlines its effort to prop up growth and counter disinflationary pressures. A similar fall in the five-year LPR — the benchmark for new mortgage loans — was a surprise and suggests that a cooling housing sector is giving the authorities more room for monetary stimulus.” — Chang Shu

Reserve Bank of India

- Current repo rate: 5.15%

- Forecast for end of 2020: 4.7%

India’s central bank is likely to resume easing interest rates, perhaps in the middle of 2020 and once headline inflation comes off the boil. Costly onions have pushed inflation closer to the upper end of the Reserve Bank of India’s 2%-6% target band, limiting policy makers’ ability to support an economy expanding at its weakest pace in more than six years.

A much higher than expected spike in inflation was the reason for the RBI’s surprise pause on rate cuts in December after delivering 135 basis points of easing in five back-to-back moves this year. However, Governor Shaktikanta Das has made it clear that there’s more space for monetary easing and a lot depends on how these actions are timed.

What Bloomberg’s Economists Say: “The Reserve Bank of India’s shock hold on rates in December signaled that it’s more concerned about a temporary surge in onion prices pushing headline inflation higher than slumping growth. We expect the central bank to keep rates on hold again in February due to the further surge in onion prices since then. RBI’s accommodative stance signals that room for further easing is available.” — Abhishek Gupta

Central Bank of Brazil

- Current Selic target rate: 4.5%

- Forecast for end of 2020: 4.5%

Brazil’s central bank is closing a monetary easing cycle that has taken its benchmark interest rate to an all-time low of 4.5%. While investors are still debating whether the rate may drop an additional 25 basis points, they mostly agree it should stay near the current level by end-2020.

The unprecedentedly long spell of low interest rates is supported by the fact that inflation expectations remain within the official target for the next couple of years, at least. Latin America’s largest economy is also gaining traction after nearly three years of disappointing performance, but the recovery remains gradual.

What Bloomberg’s Economists Say: “BCB started a new round of rate cuts last July but appears to be close to a pause. Anchored inflation expectations and ample economic slack base our expectation that it will remain at this level through end-2020, absent surprises. An additional, smaller 25bps cut in the February meeting cannot be ruled out if inflation and growth surprise on the downside, or if the currency strengthens until then.” — Adriana Dupita

Bank of Russia

- Current key rate: 6.25%

- Forecast for end of 2020: 6%

After years of struggle to bring down high inflation, Bank of Russia Governor Elvira Nabiullina is now facing a serious undershoot of her 4% target. Five consecutive rate cuts have so far failed to stoke price growth or do much to boost the sputtering economy, partly because of a delay to government spending in the second half of 2019.

Nabiullina said in December that the effect of easing will take time and the central bank needs to wait to evaluate the impact. Another rate cut is possible at the next meeting in February or later in the first half, but not guaranteed, she said. Russian local-currency government bonds have attracted inflows of about $16 billion this year due in part to faster-than-expected easing. Investors are waiting to see if 2020 will bring more of the same.

What Bloomberg’s Economists Say: “Sliding inflation will keep one more rate cut on the table in 2020, but policy makers are likely to pause to assess the impact of 150 basis points of reductions since June. If price pressure remains muted, as we expect, the next move could come as soon as March. Signs of a firmer rebound in inflation, as President Vladimir Putin’s fiscal stimulus finally gets going, might put policy on hold for longer.” — Scott Johnson