South Africans hanging by a dangerous thread

South African households are overly reliant on short-term or payday loans to make ends meet, putting them in an extremely precarious position.

The latest DebtBusters Debt Index for the second quarter of 2025 has revealed that households have buckled under financial pressure, with a 6% increase in demand for debt management and counselling.

A clear trend among all those who have gone this route is that they have active personal loans, with the group tracking a 95% hit rate.

Worse still, at least half had one-month or payday loans attached.

According to DebtBusters executive head Benay Sager, these worrying statistics come even as inflationary pressure has subsided in South Africa.

Despite this, consumers continue to use loans to make ends meet, ultimately eroding their income.

This is because, while convenient in addressing short-term needs or even being a needed lifeline for the family, these types of loans are extremely expensive, attracting more than 23% interest per annum.

Sager said the compounding effect of these high interest rates is clear.

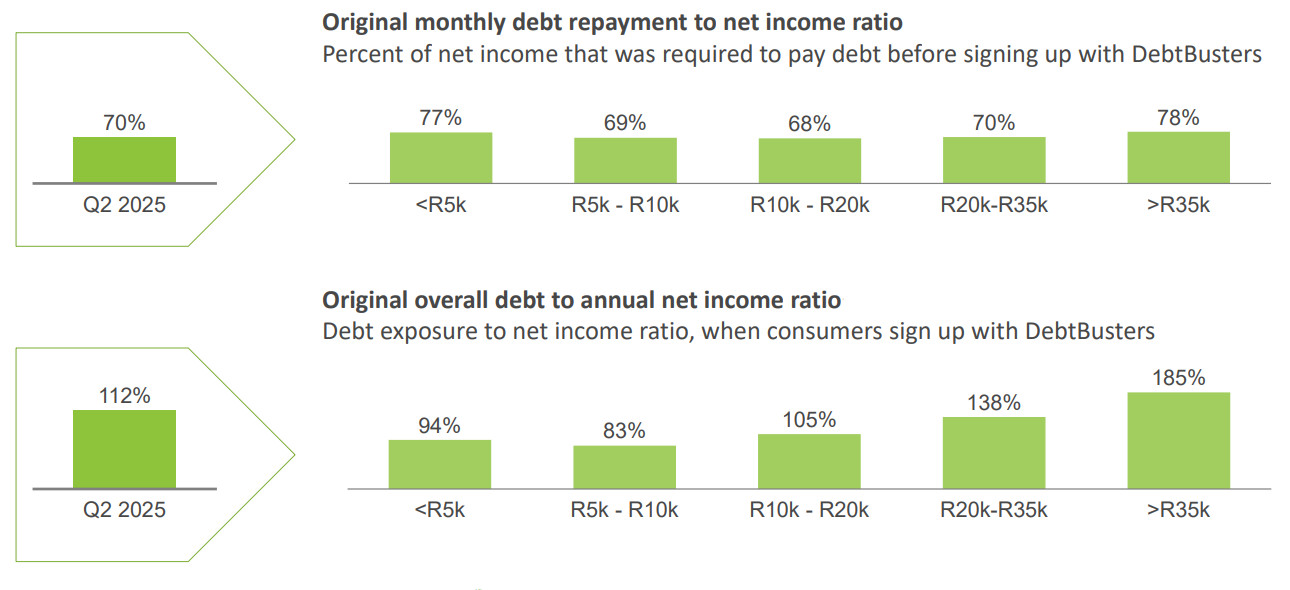

The median debt-to-annual-income ratio has increased to 112% after declining for most of 2024. Further, the share of income required to service debt has increased to 70%—the highest level since 2017.

On average, consumers need 70% of their take-home pay to service debt. Those earning R35,000 or more a month spend 78% on debt repayment.

Debt-to-annual income ratios for top earners are at or near the highest-ever levels.

For people taking home more than R20,000 a month, the ratio is 138% and for those earning R35,000 or more, it is 185%.

Sager noted that high-income consumers have high and increasing levels of unsecured debt, currently 33% higher than in 2016.

For those taking home R35,000 or more, unsecured debt levels were 79% higher than nine years ago. “This is simply unsustainable,” he said.

Purchasing power has crumbled

Sager noted that many households have no choice but to take out costly loans to balance their budgets.

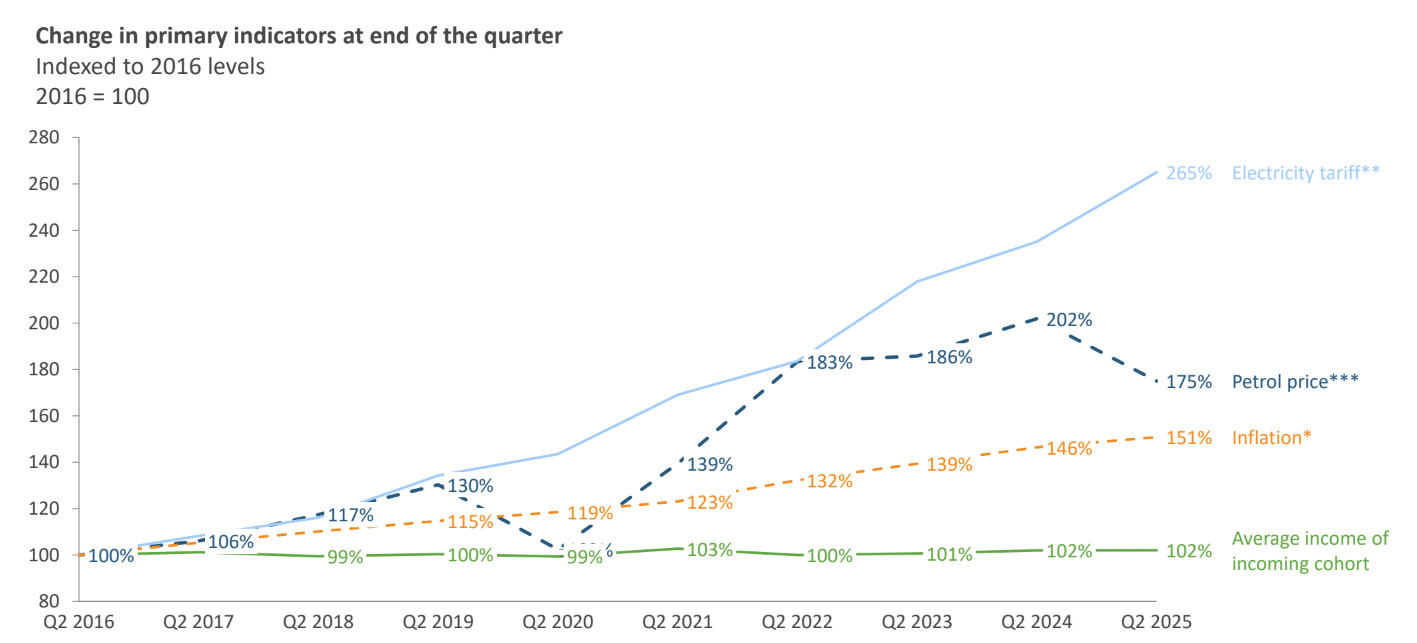

While inflation has eased, regulated expenses like electricity, rates and taxes have not. Worse yet, salaries have not kept up with inflation, destroying any hope of consumers maintaining purchasing power.

“Compared to 2016, electricity tariffs have more than doubled and are now 2.65 times higher; the petrol price has increased by 75%; and the compound impact of inflation is now 51%,” Sager noted.

In the major metros, municipal rates continue to increase by double digits every year. This all adds to the financial pressure on South African households.

This was confirmed by Stats SA, which reported a significant uptick in inflation for July, when municipal rates and taxes were hiked, driven in large part by these costs.

With high levels of inflation over the past decade, amid low growth and financial strain on businesses, South African salaries have not kept up with the rising costs.

DebtBusters’ data shows that purchasing power has crumbled, with nominal income only increasing by about 2% against the cumulative impact of inflation at 51%.

This means that a salary today buys 49% less than it did almost a decade ago.

The impact is even more severe in the R5,000-R10,000 per month and R20,000-R35,000 per month brackets, where nominal salaries have declined 1%- 2%.

As a result, households have been using credit, loans, borrowing, and even retirement savings to compensate for the lost purchasing power.

Some South Africans have managed to mitigate the pressures by tapping into resources like withdrawing funds from the two-pot retirement system, but this carries consequences of its own.

Sager said that access to retirement funds appears to have become a staple for many, with more than 2.2 million South Africans having accessed the two-pot retirement system for a payout of some amount.

However, withdrawals from retirement funds often kick financial strain down the road, with fund managers constantly urging members to leave their retirement funds alone.

For greater context, while households on average spend 70% of their disposable income paying off debt, only 2.1%—the average among higher income earners—goes into retirement savings.