FNB hits R1 trillion goal

FNB has seen its deposit base exceed R1 trillion despite the ‘Big Four’ bank seeing minimal growth in customer numbers.

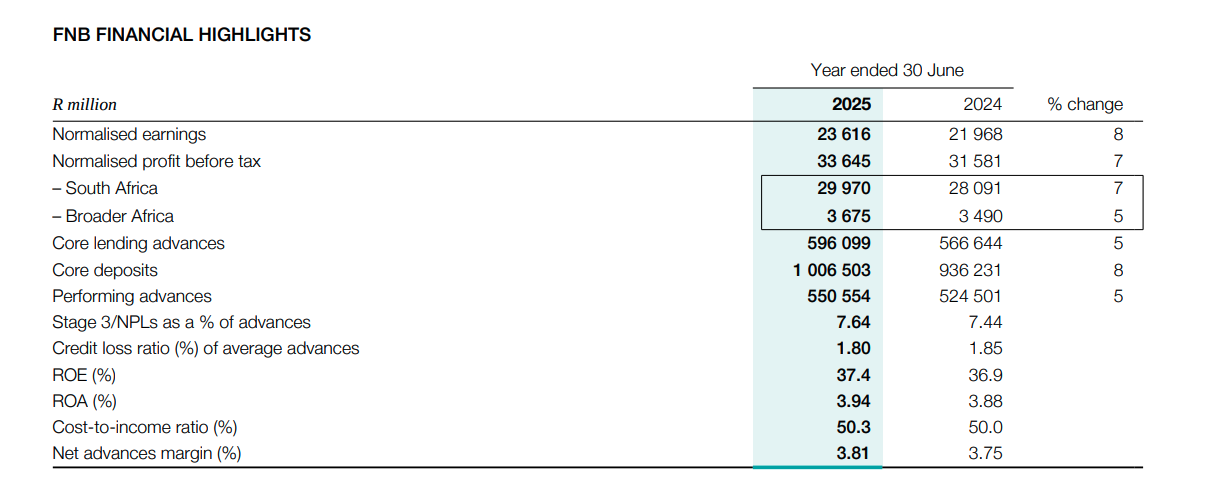

In its parent FirstRand’s results for the year ended 30 June 2025, FNB said it delivered normalised profit before tax growth of 7% to R33.6 billion, and an ROE of 37.4% in the year under review.

FNB’s net interest income growth of 6% resulted in growth from both advances and deposits.

The deposit franchise in South Africa grew 7% off an already high base, with broader Africa’s deposits also continuing to scale, delivering 11% growth.

Notably, a significant milestone reached during the year is FNB’s deposit base exceeding R1 trillion.

FNB grew advances by 5%, targeting commercial customers as household affordability remained under pressure.

The overall commercial book grew 11%, with lending anchored to targeting specific sectors and subsegments (i.e. SMEs) informed by lending capacity assessments.

It noted that retail advances required some risk cuts in the first half of the financial year and origination strategy adjustments, resulting in 3% growth, weighted towards unsecured portfolios.

FNB did see non-interest revenue increase by 6%, with fee and commission income increasing by 6%.

Non-interest revenue increased due to moderate fee increases across retail and commercial accounts, new customer acquisition, improved volumes and cross-sell.

This was partially offset by the cost of increased eBucks rewards on the back of the roll-out of new partnerships and higher transaction processing fees.

It added that growth in secured lending remained subdued at 3% due to the pressure on customer affordability and weak demand.

Property prices, particularly in Gauteng and KwaZulu-Natal, also continued to be depressed.

FNB’s credit impairment charges increased 3% to R10.5 billion, while the credit loss ratio decreased to 180 basis points

This year-on-year movement was partly driven by elevated credit impairments in the commercial segment.

This included strong growth in the SME client segment and transactional lending products in commercial at higher coverage ratios.

There was also a rise in arrears and debt review inflows, and more accounts for a significant increase in credit risk, which reflects continued strain in specific customer segments.

FNB’s total number of clients increased by a mere 1%, as retail customers increased to 8.66 million.

Notably, the personal segment, which includes South Africans earnings less than R750,000, reduced by 1% to 7 million customers, from 7.05 million in the prior period.

Private customers increased by 7% to 1.66 million, while commercial customers grew by 6% to 1.35 million.

FirstRand’s results

FirstRand said that it delivered a strong operational performance, with all of its large domestic operating businesses delivering high-quality growth in earnings and improved returns.

This rise in earnings and returns comes despite ongoing macroeconomic challenges in the group’s jurisdictions.

The strong performance enabled the group to absorb the impact of a further pre-tax accounting provision of R2.7 billion relating to a UK motor commission matter related to commissions given to dealerships.

In addition, the UK court matter incurred a further R253 million (£10.8 million)of legal and professional fees.

Together, the total pre-tax impact of these two items relating to commission stands at R2.96 billion for the 2025 financial year.

Despite the provision, normalised earnings increased 10% to R41.8 billion, and the group produced a normalised ROE of 20.2%.

With the rise in earnings, the board increased the total dividend by 12% to 466 cents.

The overall credit performance for the group is also broadly in line with its through-the-cycle (TTC) expectation, with the credit loss ratio at 85 bps remaining at the bottom end of its TTC range.

The four-bps increase in the credit loss ratio was partially driven by the emerging strain in the FNB commercial book.

| FirstRand Results | 2025 | 2024 | % change |

|---|---|---|---|

| Normalised earnings per share (cents) | |||

| – Basic | 746.4 | 677.2 | 10% |

| – Diluted | 745.6 | 677.2 | 10% |

| Headline earnings per share (cents) | |||

| – Basic | 748.8 | 679.0 | 10% |

| – Diluted | 748.0 | 679.0 | 10% |

| Earnings per share – IFRS (cents) | |||

| – Basic | 748.7 | 681.4 | 10% |

| – Diluted | 747.9 | 681.4 | 10% |

| Normalised earnings | 41 824 | 37 988 | 10% |

| Headline earnings | 41 881 | 38 054 | 10% |

| Normalised net asset value | 217 418 | 195 664 | 11% |

| Normalised net asset value per share (cents) | 3 884.1 | 3 488.1 | 11% |

| Ordinary dividend per share (cents) | 466 | 415 | 12% |

| ROE (%) | 20.2% | 20.1% | – |

| Net asset value per share (cents) – IFRS | 3 875.4 | 3 484.7 | 11% |

| Advances (net of credit impairment) | 1 748 639 | 1 611 541 | 9% |

| Credit loss ratio (%) | 0.85% | 0.81% | – |