South Africa risks going from hero to zero

The searing rally across South African assets this year risks running out of steam unless economic growth picks up enough to make a dent in the nation’s sky-high unemployment rate.

Stocks, bonds and the currency have surged amid soaring commodity prices and government reforms. The benchmark equity index is up about 46% in dollar terms, local-currency government debt has returned more than double the emerging-market average, and the rand is on track for its strongest year against the dollar since 2022.

But it would be a mistake to assume those gains will continue in 2026, according to the country’s biggest private investor.

With gross domestic product growth struggling to accelerate above 1% and almost a third of the country’s working-age population unemployed, companies will find it hard to generate the kind of profits that would justify the returns their shares have seen in 2025.

“The question is job creation, job creation and job creation,” said Hendrik du Toit, chief executive of Ninety One Plc, which oversees about R3.5 trillion.

“Without it, you simply will not sustain momentum. Some of these businesses will do well, but the feast has been had.”

Finance Minister Enoch Godongwana delivered a-better-than-expected budget update earlier his month, with revenue overshooting previous projections and the National Treasury recommitting to its fiscal-consolidation plans.

S&P Global Ratings responded by upgrading South Africa’s credit assessment for the first time since 2005. Power cuts have virtually ceased and the nation’s coalition government has moved to tackle logistical constraints that have hamstrung exports.

The turnaround follows years of negativity over electricity shortages, state corruption, political uncertainty and surging living costs. Gross domestic product expanded by an average of less than 1% a year over the past decade, and the unemployment rate remains above 30%.

The National Treasury expects the average growth rate to accelerate to 1.8% over the next three years, but some investors caution that any investment surge is contingent on the improved outlook materializing.

“Structural reforms that create jobs are essential,” said JPMorgan Chase & Co. Vice Chairman Daniel Pinto at Bloomberg’s Africa Business Summit earlier this month.

“The government is doing some of the right things, and if reform deepens, the informal economy will shrink and living standards will improve.”

The FTSE/JSE Africa All Share Index is set for its best year since 2006, outperforming the emerging-market benchmark, the S&P 500 and the Stoxx Europe 600.

Much of the gain was driven by the surge in gold, silver, and platinum prices, which lifted an index of precious-metals miners more than 180%.

A net 75% of fund managers in a Bank of America Corp. survey conducted earlier this month are bullish South African equities, up from 69% in the previous poll.

Banks and retailers are among the most overweight sectors, suggesting they could lead the next leg of the rally along with industrials and renewable-energy-linked plays — provided government reforms unlock economic growth.

“Finance is very big here and continues to do well, but finance can only prosper if the economy comes through,” Du Toit said.

He estimates that South African companies have about $100 billion on their balance sheets that could be unlocked if the government overhauled regulations constraining investment.

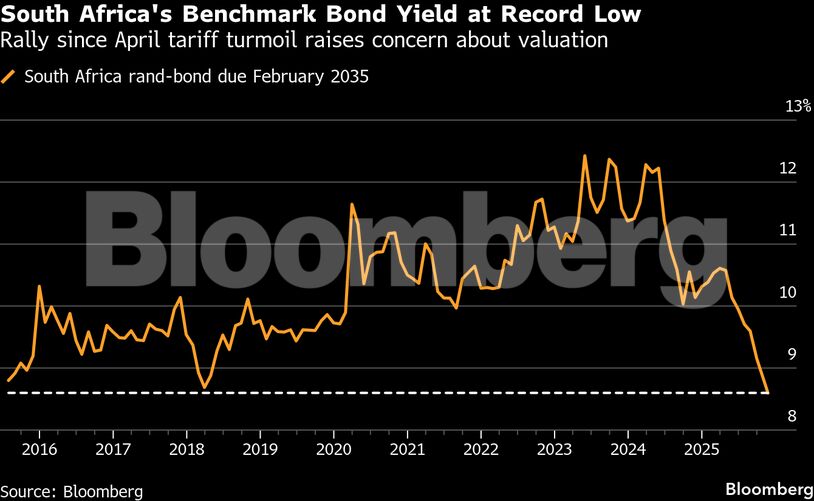

The bond market, meanwhile, has been supported by moderating inflation, lower interest rates and fiscal consolidation. Government rand bonds have returned about 32% in dollar terms this year, compared with 15% for a Bloomberg country-capped index of local-currency debt.

Foreign investors are flocking to the market, with net inflows of R175 billion in the year through October, compared with R73 billion in the whole of last year, according to National Treasury data.

Still, non-residents hold only about a quarter of outstanding government debt, down from as high as 43% seven years ago. That leaves plenty of room for upside as Federal Reserve interest-rate cuts prompt investors to look for better returns outside the US.

Some investors, however, say further gains will be harder to come by. Yields on 10-year government bonds have plunged more than 170 basis points this year and are near record lows.

That makes them expensive relative to history, even though the yields remain attractive compared with global fixed income, said David Austerweil, an emerging-markets deputy portfolio manager at Van Eck Associates Corp. in New York.

“We’ve moved to market weight in South African government bonds after having been very overweight all year, given major catalysts have been realized and bond valuations are less cheap,” he said.

“However, we think there is still upside next year. The fundamental story continues to improve and we think that will continue to support asset prices.”

The rand is benefiting from improved terms of trade due to rising values of commodity exports, as well as the attractive carry returns generated by the interest-rate differential with the US and historically low volatility.

The South Africa currency has gained 10% against the dollar this year, returning 13% for traders who borrow dollars to buy higher-yielding assets.

Yet options positioning shows traders are turning more bearish on the rand over the coming year, using current levels to lock in hedges against declines.

The premium of options to sell the rand over the next year versus those to buy it, known as the 25 Delta Risk Reversal, has climbed more than 50 basis points since the end of August to the widest since President Trump’s April tariff announcements roiled markets.

Bloomberg’s forecast model, based on the prices of options to buy and sell the rand versus the dollar, assigns a 46% probability to the currency strengthening from current levels over the next 12 months, versus a 54% probability of weakening.

“We expect the rand to continue to strengthen next year but are not expecting the performance to be as good as this year,” said Lee Hardman, a senior currency analyst at MUFG Bank Ltd.

Financial assets have already priced in a lot of good news in a short space of time. The foundations are in place, but a more durable cycle will require deeper policy reforms to spark an improvement in the real economy, said Lester Davids, an analyst at Unum Capital Ltd.

“Once the growth engine moves, capital will flow,” he said. “South Africa has advantages. It’s not that difficult, but we have to get the basics right.”