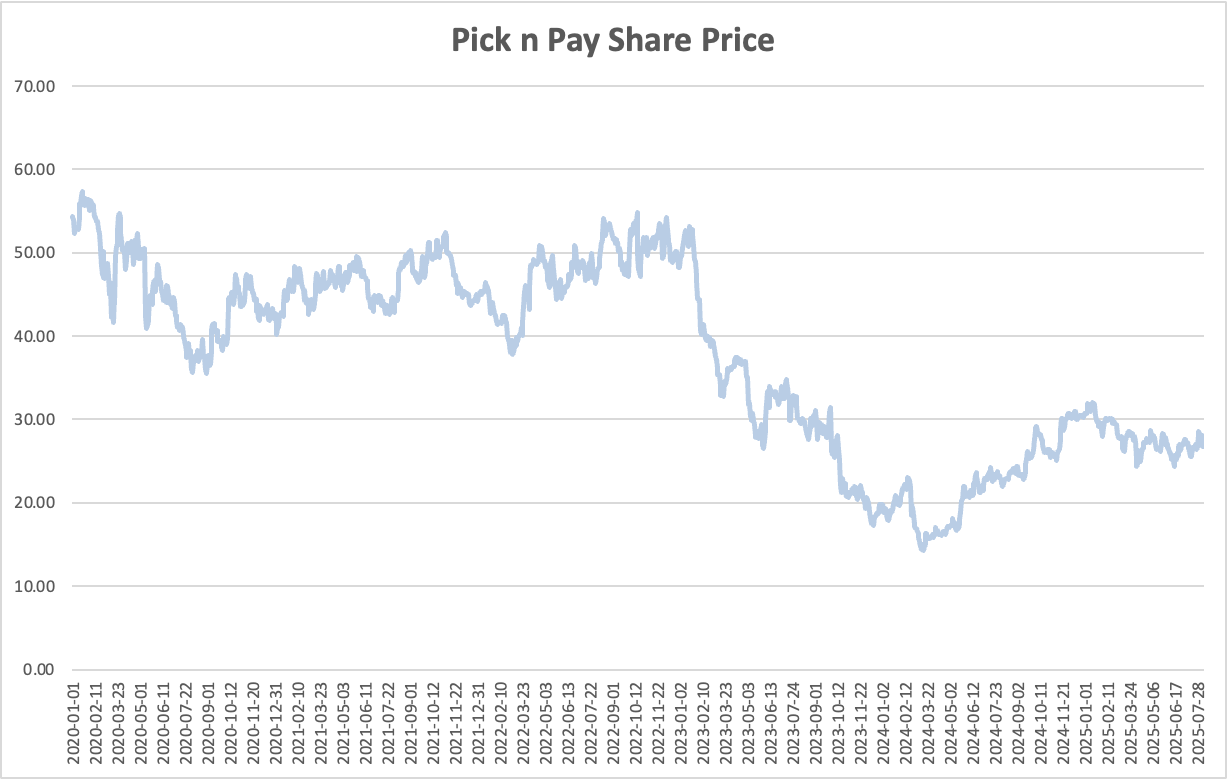

Pick n Pay is worth zero

Chantal Marx from FNB Wealth and Investments believes that there is value in Pick n Pay despite the current price implicating little to no value when excluding Boxer.

Pick n Pay has been one of South Africa’s largest retailers for around seven decades, but has recently fallen on hard times.

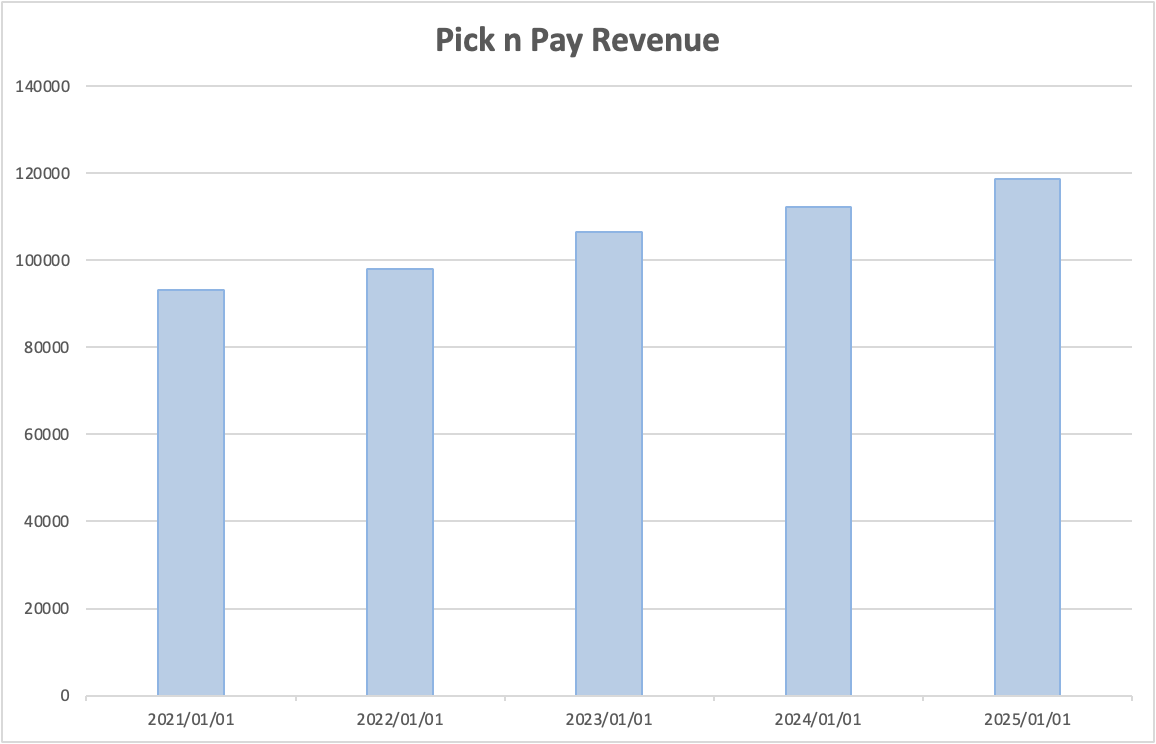

The group reported cumulative losses of roughly R4 billion in the 2024 and 2025 financial years amid the poor performance of its core Pick n Pay grocery business.

This led to massive structural changes at the group, with the founding Ackerman family giving up majority control following a rights offer in 2024.

Gareth Ackerman, the son of Pick n Pay founder Raymond Ackerman, also stepped down as chairman earlier this week.

Former CEO Sean Summers also returned to the group in 2023 to turn operations around, despite being in his early 70s.

On top of the rights offer, the group also launched an IPO for Boxer in late 2024 to help raise about R8 billion in cash. As per the IPO, Pick n Pay retained a roughly 65% share in Boxer.

The discount retailer has been one of the group’s best performers, driving revenue growth and rapidly expanding its store base.

In its latest trading statement for the 17 weeks to 29 June 2025, Boxer said it aimed to open 60 new stores – 25 Superstores and 35 liquor stores.

This came off the back of the group’s turnover for the period, growing by 12.1% and 3.9% like-for-like in the context of low internal selling price inflation and a highly constrained consumer.

Unfortuntely for Pick n Pay, the market sees its Boxer spin-off as being far more valuable than its core operation.

Should be worth more

Speaking with MoneywebNow, Marx said that it was not fair that Pick n Pay outside of Boxer is valued at zero by the market.

Pick n Pay’s market cap currently stands just shy of R20 billion, while Boxer’s sits at R31 billion.

Pick n Pay stores in isolation thus seen to have zero or minimal value. Marx said that execution risk and holding company dynamics may explain this in part.

Although Pick n Pay’s growth rate is far slower than its largest rival, Shoprite, it is still heading in the right direction.

In its latest trading statement for the 17-week period to 29 June 2025, the Pick n Pay group saw its turnover increase 4.3%, with like-for-like sales up 3.8% against last year’s same period.

Pick n Pay South Africa (SA) like-for-like sales for the period grew by 3.6%, with online sales also increasing by 33.0%, driven Pick n Pay ASAP!, and Mr D.

Marx was particularly impressed by the Pick n Pay clothing business, which saw growth of 12.1% over the period.

The group is also progressing with cleaning up its operations, with stores under challenging positions converted into Boxers.

The group noted that its Store Estate Reset Plan resulted in turnover growth lagging like-for-like sales momentum, which resulted from the planned store closures and conversions.

It noted that closures and conversions are expected to contribute to achieving the medium-term break-even objective of the Pick n Pay segment.

Although Pick n Pay is not expected to profit in the next 6 months, Marx believes that the group will break even ahead of management’s expectation of 2028.

Financials

*The article has been updated with further commentary from Chantal Marx.