The 24-year-old company in South Africa set to become the new Capitec

WeBuyCars has gone from a single used-car dealership in Pretoria to being deemed a potential new Capitec or Discovery.

The company was founded in 2001 by brothers Dirk and Faan van der Walt, with the latter stating it all began with an eye for a bargain and the joy of discovering the price of cars.

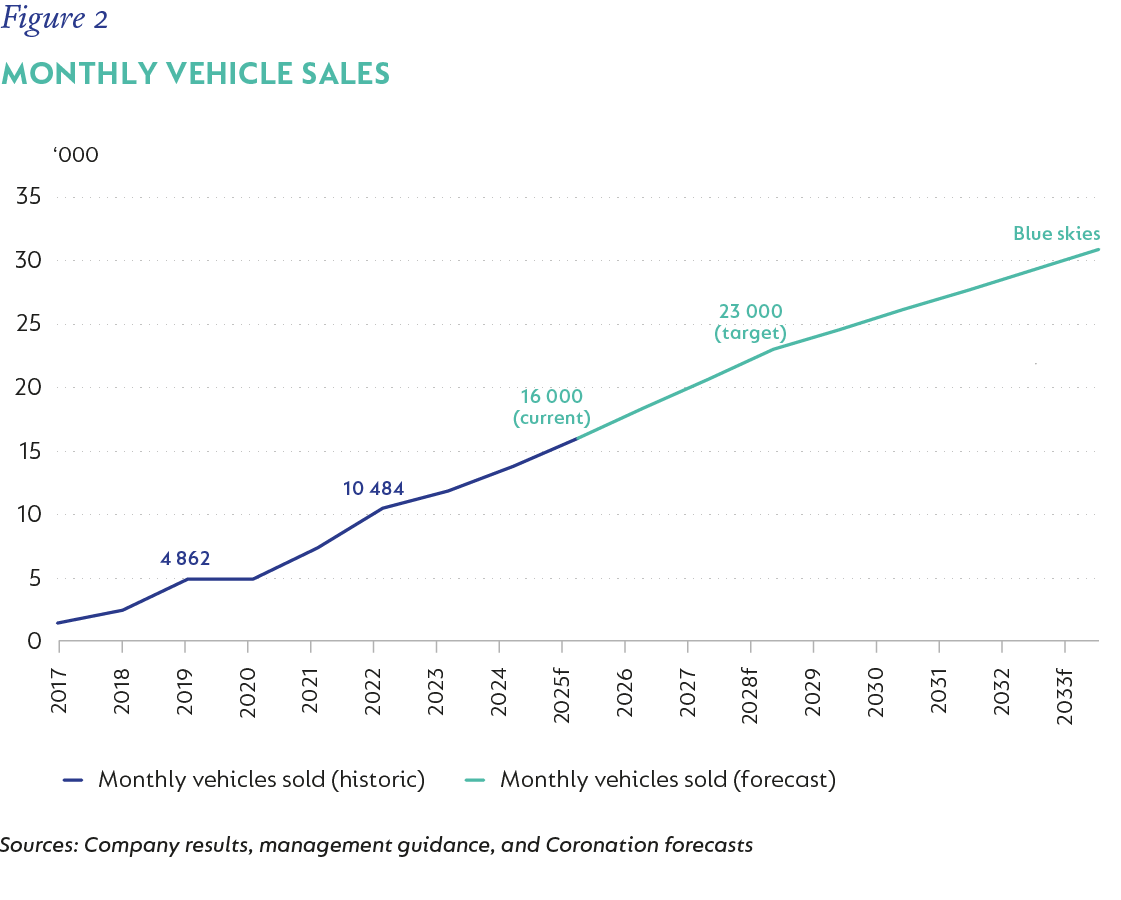

After opening its first dealership in 2001 with just two employees, WeBuyCars now sells over 15,000 vehicles per month and employs more than 3,500 staff members.

In 2020, Transaction Capital acquired a 49.9% stake in the company, and WeBuyCars saw its trade volume increase tenfold.

However, amid issues with its investment in SA Taxi, Transaction Capital announced its intention to unbundle and separately list WeBuyCars on the main board of the JSE.

Since its listing in April 2024, the stock’s share price has risen by over 130%. Notably, the market was sceptical of WeBuyCars at first.

Its bookruner is failing to place the full allocation of shares at the targeted valuation.

However, Coronation’s Ruan Koch said that WeBuyCars’ management was under pressure and had worked to defy the narrative that it was not meaningfully different from other retailers.

“We are great believers in the company and used the IPO to increase our shareholding, adding to the equity we had acquired during the pre-IPO restructuring process,” said Koch.

“At the time, we believed that the unbundling presented an outstanding opportunity for investors to own a high-quality company with the potential to disrupt the used vehicle market and meaningfully grow its market share.”

Koch said that unbundlings and spin-offs often create attractive opportunities for active investors, as these companies typically have limited coverage.

What makes WeBuyCars so attractive

Koch said that the consumer-to-business (C2B) vehicle acquisition is the cornerstone of WeBuyCars’ business model.

“The process is heavily digitised, and its successful scaling over more than two decades has resulted in a very low unit cost, which no competitor can match.”

“Tens of thousands of consumer leads are screened each month, with the best converting into profitable trades. This gives WBC unparalleled visibility into the overall vehicle market.”

The company also has cost advantages stemming from its brand, economies of scale, and low rental costs, as well as a 24-year head start on its competitors.

The company is also developing its own vehicle-assessment scorecard, which is expected to enhance transparency and bolster pricing confidence.

Although Coronation remains confident in WeBuyCars’ long-term advantages, it continues to monitor shorter-term factors, including new entrants testing the market and pressure from cheaper new vehicle imports.

WeBuyCars highlighted the challenge of competing with cheap Chinese cars in the market, which impacted consumer behaviour.

However, it believes that these Chinese cars will be a net positive for the used car market, as they will soon expand its acquisition base and opportunity set.

“We believe WBC’s scale and experience in sourcing and pricing should help it manage these challenges,” said Koch.

He added that WeBuyCars has the scope for a higher market share in the decades ahead, potentially as much as 30%-40%

The South African precedent supports this, with several companies in South Africa seeing sustained market share gains.

This includes Capitec in banking, which, over the course of two decades, has become the most valuable bank in the nation, serving 25 million customers.

Clicks and Dis-Chem have also grown their share across South Africa’s pharmacies, while Discovery Health has become the dominant player in medical schemes.

“These businesses grew market shares well beyond initial expectations by reinvesting lower cost advantages into unlocking superior value for consumerism,” said Koch.

“This is one of those businesses that gets better as it gets bigger. We expect WBC to replicate the kind of market share gains that these businesses have achieved over time.”