Steinhoff has spent R626 million on accountants and consultants since December

The most important passage in Steinhoff International Holdings NV’s regulatory filing late Friday, was a section attesting that management still believes the retailer is a going concern.

A formality for most companies, Steinhoff’s confidence that it can keep the lights on isn’t self-evident. The acquisitive South African group’s shares have lost almost all their value and its bonds trade at a steep discount following a warning of accounting regularities and the resignation of its chief executive, which triggered a liquidity crisis in December.

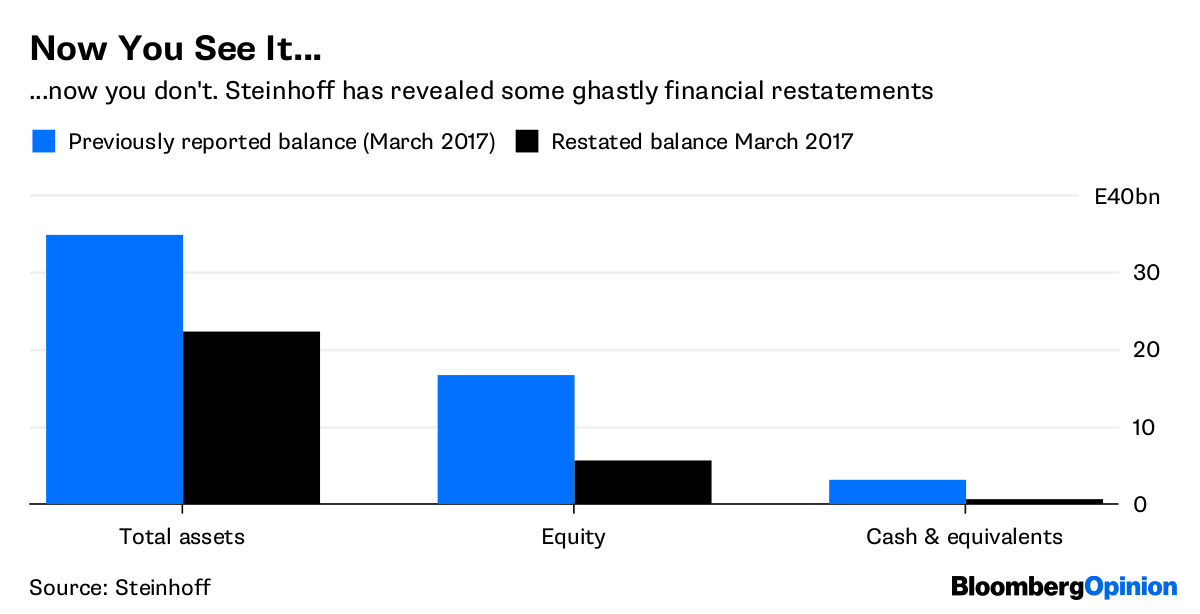

The new unaudited figures for the six months to March include a shocking 11 billion euros ($12.8 billion) back-dated restatement of shareholders’ equity, including the disclosure that much of the 3 billion euros of cash it reported a year ago didn’t exist (or shouldn’t have been consolidated) and that its profits were overstated by about one billion euros.

It reported a 600 million euro net loss.

It’s a bleak picture for Steinhoff’s new management team as it tries to meet obligations on a 10.6 billion euro debt, recover some value for shareholders and reassure customers and suppliers that it’s still a reliable partner. As is often the case in these types of situations, only Steinhoff’s financial advisors seem to be doing well from its implosion.

Equity investors are naturally furious about what’s happened and some are suing the company. Holders of Steinhoff’s debt are fortunate that those claims won’t be resolved quickly, so any cash penalties will only come due later – possibly allowing some time for the retailer to stagger to its feet again.

The company hasn’t yet made a provision for possible litigation payouts, nor quantified the potential liabilities.

For now, that’s helping to stop Steinhoff from giving up the ghost. But it means that even these unvarnished accounts are a pretty sketchy guide to its true financial condition.

The numbers published Friday are unaudited, so think of them as a best guess. There’s a risk of more irregularities coming to light because of the ongoing probe of various off-balance sheet structures and non-arms length transactions. And that’s not the only problem.

Writing off 11 billion euros of equity sounds like a clearing of the decks, but Steinhoff’s accounts still show a a big chunk of goodwill and intangible assets, a legacy of its free-wheeling M&A days.

Take Mattress Firm, whose inflated purchase price I explored here. The US store chain is losing money and has recognized a 1.5 billion euro goodwill impairment in view of its diminished prospects.

That’s pretty shocking given the unit was acquired less than two years ago. But there’s still another one billion euros of Mattress Firm goodwill on the Steinhoff books.

In total, the Steinhoff accounts show just 3.8 billion of net assets, meaning it can ill afford further impairments. Steinhoff’s market capitalization is just 363 million euros, which suggests shareholders aren’t optimistic.

A more pressing concern is paying creditors. Steinhoff’s liabilities due within 12 months vastly exceed current assets. Agreeing a restructuring plan and repayment rescheduling with bondholders should ease those cash pressures somewhat, but not entirely.

Steinhoff’s operations bled 800 million euros of cash over the six months to March because suppliers have tightened payment terms. Don’t expect them to cut Steinhoff any slack. Similarly, it’s difficult to convince a customer to put down a deposit for made-to-order furniture when they might wonder whether the company will still be operating in 12 months’ time.

The retailer has sold some businesses, property and a corporate Gulfstream jet to help fund its obligations but the weak cash generation makes more asset sales quite likely.

It’s no small irony that the task of boosting cash flow is made harder by the expense of hiring forensic accountants (PwC) and consultants (Moelis and AlixPartners) to clean up the mess. Steinhoff spent 39 million euros on professional fees since December and expects that to rise “substantially.”

This cost is unavoidable but it will irk Steinhoff investors. They’ll wonder why the external auditor Deloitte LLP felt able to attest the now discredited accounts as a “true and fair” reflection of its financial position. Although Deloitte did eventually raise concerns about Steinhoff, as of Friday we know its “true and fair” assessment was off by about 11 billion euros. Another triumph for the bean-counters.

Read: Steinhoff asks creditors for more time to avoid insolvency