A better year for South Africa

Barring a surprise Christmas rally or a visit from the Market Grinch, we have a reasonably good idea what the calendar year returns for 2019 should be, says Dave Mohr, chief investment strategist, and Izak Odendaal, an investment strategist at Old Mutual Wealth.

On one level this doesn’t matter, since most investors’ financial horizons don’t neatly overlap with calendar years – unless, for instance, you retire on 31 December.

Still, humans like compartmentalising, and we also like looking back. December is the season for reflecting, after all.

Bonds

Let’s start with bonds. The All Bond Index returned 8% for the first 11 months of the year, ahead of cash, despite all the negativity.

After all, this year has seen financial media saturated with articles on debt traps, downgrades and unfounded fears of International Monetary Fund (IMF) bailouts.

To be clear, there is a lot of bad news for the bond market.

Government’s fiscal deficits are increasing, not declining, and too-big-to-fail Eskom is still lurking in the shadows, cap in hand for more state support.

More borrowing means more bond supply, which should in theory suppress prices and raise yields. The key thing is that the demand for bonds remains healthy, due to the attractive yield.

Also, the yield is high precisely because of all the bad news, which is already priced in. By the time you read about something in the newspapers, it has long been discounted by financial markets.

The yield on the 10-year South African government bond declined slightly from 9.6% to 9.4% during 2019. The high starting yield means return from income will probably be good even if there is some capital loss.

If there is a capital gain, the returns can be substantial.

Chart 1: Local bond yields and returns

There is also the element of luck. Global bond yields slumped during the course of the year as investors priced in slower growth and lower interest rates.

This limited upward pressure on South African yields. The other factor limiting the upward pressure on yields is muted inflation.

Consumer prices have been rising at an average annual pace of 4.5% over the past three years. The latest reading was only 3.7%.

Property

Listed property had a torrid time, buffeted by three broad trends. Firstly, the local economy is struggling, suppressing demand for property even as supply growth (new malls, office buildings and logistics facilities) has been reasonably robust.

The result is rising vacancies and downward pressure on rents.

Rental income is ultimately what property companies pay out to investors. Secondly, local companies engage in a number of financial tricks to boost short-term distributions.

These were not repeatable indefinitely and are now unwinding, but caused many investors to overestimate future distribution growth.

Thirdly, JSE-listed property has high exposure to UK retail, which has taken the twin blows of Brexit uncertainty and competition from e-commerce.

The FTSE/JSE All Property Index returned 1% in 2019 to date, an improvement from last year’s 25% slump.

The sector trades on a yield of almost 10% which is attractive, but there is still some risk that distributions will decline next year instead of growing as the adjustment to a new reality continues.

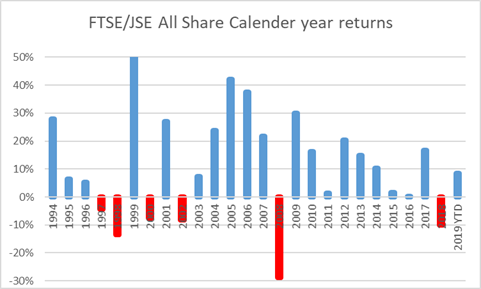

Equities

Depending on your choice of benchmark, local equities lost 10% in 2018, the first negative calendar year in ten. This year has been better, with the FTSE/JSE All Share Index returning 8.5%, most of this in the first quarter.

This gain is ahead of cash and represents a real return of almost 5%, closer to the historic long-term average real return of 7%.

However, the real return over the past five years is still basically zero, and the index level is still below its January 2018 record high of 61,684.

Chart 2: FTSE/JSE All Share Calendar Year Returns

The bounce in the local equity market came despite the lack of discernible improvement in the domestic economy.

While there has been steady if unspectacular progress on economic policy reform and improved state governance, economic activity is not accelerating and business confidence is still depressed.

The Bureau for Economic Research’s Business Confidence Index hit a 20-year low level of 21 points in the second quarter, with only a mild improvement in the third quarter.

But then the local market is largely disconnected from the domestic economy, with most of the largest companies being global in nature.

The standout performers have been the platinum miners. Both Impala and Amplats have more than doubled this year from low levels, thanks to stronger platinum group metals prices.

Gold miners have also rallied along with the underlying dollar gold price. The diversified miners, Anglo American in particular, also had a good year.

Among the global consumer companies, British American Tobacco and Richemont have strongly rallied from 2018 lows.

Naspers, the largest company on the local bourse, gained 9% so far in 2019, but bear in mind it spun off Multichoice and listed its internet businesses separately under Prosus.

In contrast, financials, food producers and clothing retailers, all heavily exposed to local conditions, have struggled this year.

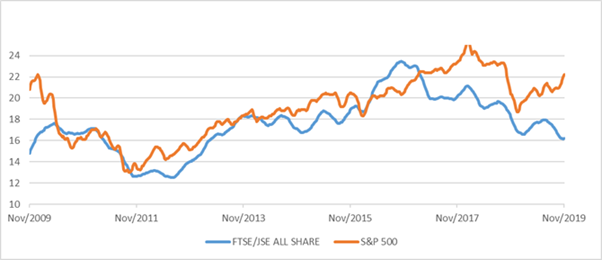

During the course of the year, the price: earnings ratio of the All Share continued to decline and is now at the lowest level since early 2013.

Compared to global markets whose valuations have increased this year, the local market trades at a 10-year low. It is therefore not the time to sell out.

Historically, buying at such valuations has rewarded patient investors. South Africans do have more investment options these days, however, and one should consider the concentrated nature of the local market as a risk factor in particular.

The top five shares make up 40% of the FTSE/JSE All Share Index, against only 27% for the UK FTSE 100, 14% for the US S&P 500 and 11% for the Stoxx Europe 600 Index.

Four out of the five largest shares in the All Share Index – Naspers, BHP, Richemont and Anglo American – are global companies, with only Standard Bank predominantly focused on South Africa.

Chart 3: Price to trailing earnings ratios

It has been a phenomenal year for global equities. The S&P 500 gained 27% in the first 11 months to hit new all-time records.

The Stoxx Europe 600 returned 25% in euros, and the Nikkei 225 19% in yen.

The MSCI All Countries World Index, our preferred global equity benchmark covering developed and emerging markets, returned 23% in dollars.

International markets have benefited from central bank easing while fears of an all-out trade war and global recession have abated.

But bear in mind that they slumped in the final quarter of 2018, with the S&P 500 suffering a 19.5% peak-to-trough decline in the 11 weeks before Christmas Eve.

At that point, the Federal Reserve was still on a hiking path and investors panicked that it would go too far, given the weakening economic outlook.

As it became clear that central banks would have to cut interest rates, global bond yields collapsed during the first nine months of the year, and at one stage $17 trillion of bonds traded at negative yields.

Bondholders clearly benefited from this rally, but even after an uptick in yields the past few weeks, they remain extremely unattractive from the point of view of a South African investor who can earn 7% from the money market, taking minimal risk.

International listed property benefited from the decline in bond yields and the rally in equities.

The FTSE EPRA/NAREIT Developed Index returned 22% in dollars this year. Unlike developed market bonds, yield in this sector is still reasonably attractive, and income growth solid.

Currency

The rand was volatile as always, hitting highs of R13.27 and lows of R15.41 against the dollar during the course of the year.

However, at the end of November, the rand was only 2% weaker against the greenback than at the start of January.

Exchange rate movements therefore provided only a modest boost to the rand-based return of global investments.

Hang in there

Putting this all together, a typical Regulation 28-compliant balanced portfolio could deliver double digit returns this year, while last year it would have been flat to negative.

Given the decline in inflation, the real return, which is what really matters, has picked up materially from 2018. Yet if you pondered your portfolio in January, you would probably not have expected much from the coming year.

Global markets had sold off sharply the previous few months, and the domestic outlook was as gloomy as ever. Turning points in markets are unpredictable, and one has to stay invested to benefit.

Turning points also tend to happen long before the proverbial dust has settled and there is an observable improvement in economic activity. Next year is bound to test our patience and willpower again.

Hang in there.

Read: High risk of load shedding for the next 18 months: analyst