Retailers in South Africa smell trouble

The latest BER Retail Survey shows that confidence among South African retailers has declined by 10 percentage points over the last quarter, taking it to levels last seen in the early months of 2024.

According to the Bureau for Economic Research (BER), the 10 percentage point drop puts the index at 32% in the third quarter of 2025, down from 42% in Q2.

This pulls retailer confidence below the long-term average of 40% and at a similar level to early 2024, where businesses faced a highly volatile and uncertain year ahead of the national elections.

Notably, while retailers are showing clear signs of stress and worry, overall profitability in the sector is still quite favourable, the BER said.

This means that businesses in the sector are anticipating trouble to come in terms of consumer demand, likely from the continued high interest rate environment, which is putting pressure on indebted households.

“Over the past year, retailers’ confidence has been much better than in the first half of 2024,” the BER said.

“However, it appears the pendulum is swinging in the opposite direction for the second half of 2025.”

The BER’s survey results suggest volume growth in the retail and wholesale sectors likely moderated during 2025Q3, pointing to a slowdown in the consumer demand environment.

This is an expected outcome as many tailwinds to consumer spending over the last few months, two-pot withdrawals and low inflation are set to provide less support in the second half of 2025.

“On the upside, new vehicle dealers and furniture retailers remain a bright spot amid an otherwise gloomy trade sector,” the BER noted.

“This indicates some resilience prevailing in consumer spending, particularly from higher-income consumers.”

In line with this, the concerns are not prevalaent across the board.

Looking at wholesales, after five quarters of outperformance, confidence in this sector lost ground, declining from 50% to 38%.

The business conditions of wholesalers ticked up, but remained just below the long-term average, signalling a challenging operating environment, the BER said.

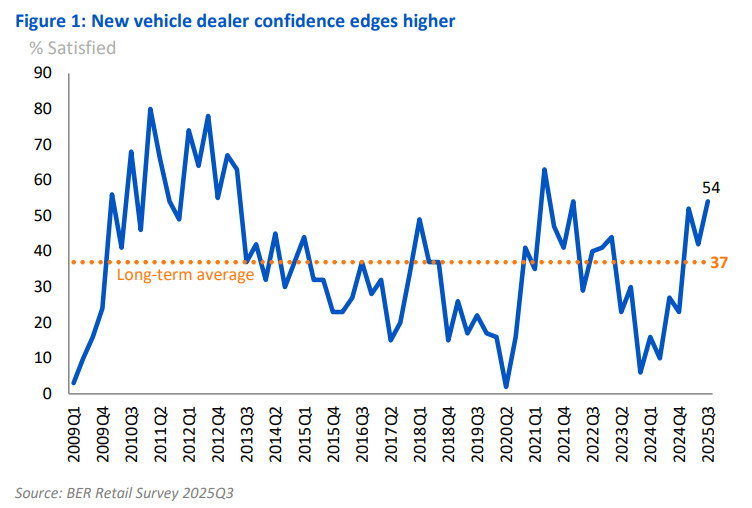

On the other side of the equation, new vehicle dealer confidence improved by a significant 12 percentage points to 54%—its highest level since early 2022.

Sentiment in this sector brightened despite a slowdown in volume growth and a decline in business conditions.

“On balance, the motor trade survey indicates a favourable operating environment for new vehicle dealers,” the BER said.

Interest rate views

Longer-term analysis comes with the warning that it that activity has reached its peak and is likely to lose some steam going forward.

“This coincides with what is probably the end of the SARB’s current interest rate cutting cycle,” the BER noted.

The SARB last week voted to hold interest rates at their current levels, being a repo rate of 7.00% and a prime lending rate of 10.50%.

While some economists had aniticipated a small cut of 25 basis points, given the lower-than-expected inflation figure, stronger rand, and the US Fed cutting rates ahead of the announcement, the central bank erred on the side of caution.

As the SARB is starting to target a lower inflation figure (“preferring” 3%) and some inflation pressure is coming in 2026 due to electricity pricing, the Monetary Policy Committee elected to sit back and assess the impact of previous cuts on the economy.

Several economists and market analysts are treating the hold as a pause—ie, forecasting more interest rate cuts on the way—but this is not a consensus view, with others seeing it as the SARB ending the cutting cycle that started in September 2024.

The SARB’s own forecast modelling still has one 25 basis point cut on the cards for 2025—and up to 75 basis point cuts in 2026—but this will hinge entirely on available data, and where the new inflation target will land.

The latest retail survey signals that the wider retail market is not expecting any significant moves.