Signs of life for one of South Africa’s largest employers

South Africa’s manufacturing sector remains constrained, but expectations are high for improvements in the first half of 2026.

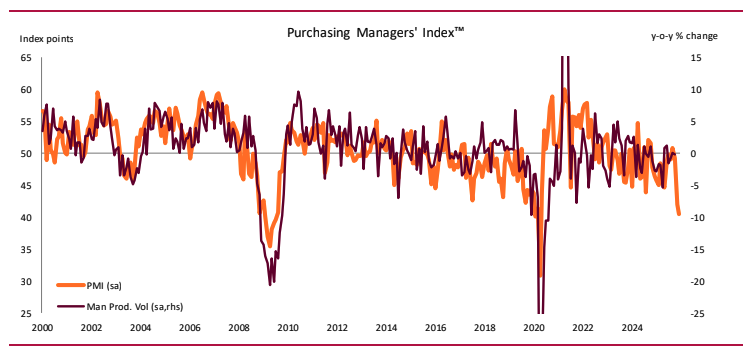

The seasonally adjusted Absa Purchasing Managers’ Index (PMI) decreased further by 1.5 points to 40.5 points in December 2025, remaining in contractionary territory.

That said, it is essential to note that the unusually sharp decline in the inventories index and the steep decline in the employment index were the primary drivers of the weaker headline reading.

New sales orders were barely changed from November and remained at a subdued level, while business activity actually improved sharply during the month, albeit remaining below the 50 mark.

The headline PMI, which is compiled by the Bureau for Economic Research (BER), thus signals that conditions in the sector remain difficult, even if activity may have improved.

However, the index tracking expected business conditions over the next six months jumped by a significant 18.1 points to 68.8 in December.

This is the highest level since the 70.8 reached in September 2024, indicating expected favourable conditions in the first half of 2026.

This is a positive sign for the manufacturing sector in South Africa, which is one of the country’s biggest employers, employing over 1.6 million workers as of Q3 2025.

While weak economic conditions persist, there are growing data points suggesting that South Africa is poised for a stronger 2026.

The South African Reserve Bank (SARB) expects growth to reach 1.4%, an improvement from the estimated 1.2% in 2025.

Interest rate cuts of 50 basis points are widely expected throughout the year, bringing the repo rate to 6.25% and lowering borrowing costs.

A fellow BER study, the FNB/BER Civil Confidence Index, reached its highest level in 11 years, driven by higher activity and profit margins.

What the PMI shows

Breaking down the PMI, the new sales order index dipped marginally to 35.4 in December.

Absa said that the decline in sales was primarily driven by the domestic economy, as improvements in export orders were insufficient to make a significant contribution to a turnaround in demand.

The business activity index also increased by 9.4 points to 46.1 in December. While remaining below the neutral level, the increase was sizeable compared to usual month-on-month movements.

“The index has been in contractionary territory for eleven of the twelve months in 2025, underscoring the

persistence of weak underlying conditions,” said Absa.

The employment index also decreased by 6.3 points in December, declining further below the neutral 50-point mark. The index has remained in contractionary territory since April 2024.

The weak performance in business activity and volatile sales orders continues to limit the scope for hiring, while shortages of specialised skills in certain industries also weigh on employment outcomes.

The supplier deliveries index also remained at similar levels, edging down to 45.1 points in December from 45.5 in November.

The purchasing price index also declined further by 4.5 points to 50 in December, the lowest level since late 2009.

“While the fuel, and particularly diesel prices, increased at the start of December, the stronger rand exchange rate likely helped alleviate input cost pressure,” said Absa.

“The sharp decline in diesel prices at the start of 2026 is expected to help further contain price pressures in the new year.”

| Index | Oct | Nov | Dec |

|---|---|---|---|

| Business activity | 49.4 | 36.7 | 46.1 |

| New sales orders | 48.9 | 35.6 | 35.4 |

| Employment | 45.1 | 46.2 | 39.9 |

| Inventories | 48.8 | 46.0 | 36.1 |

| Supplier deliveries | 53.5 | 45.5 | 45.1 |

| Purchasing prices | 61.9 | 54.5 | 50.0 |