Allan Gray has a lot to say about Dis-Chem in South Africa

Allan Gray is investing in Dis-Chem, with the retailer set to benefit from its growing store numbers and new rewards programme.

Jonty Fish from Allan Gray said that Dis-Chem meets the definition of a great business at a fair price, with a long runway for growth.

Fish said that since the liberalisation of the South African pharmacy market in 2003, corporate pharmacies have rapidly increased their market share.

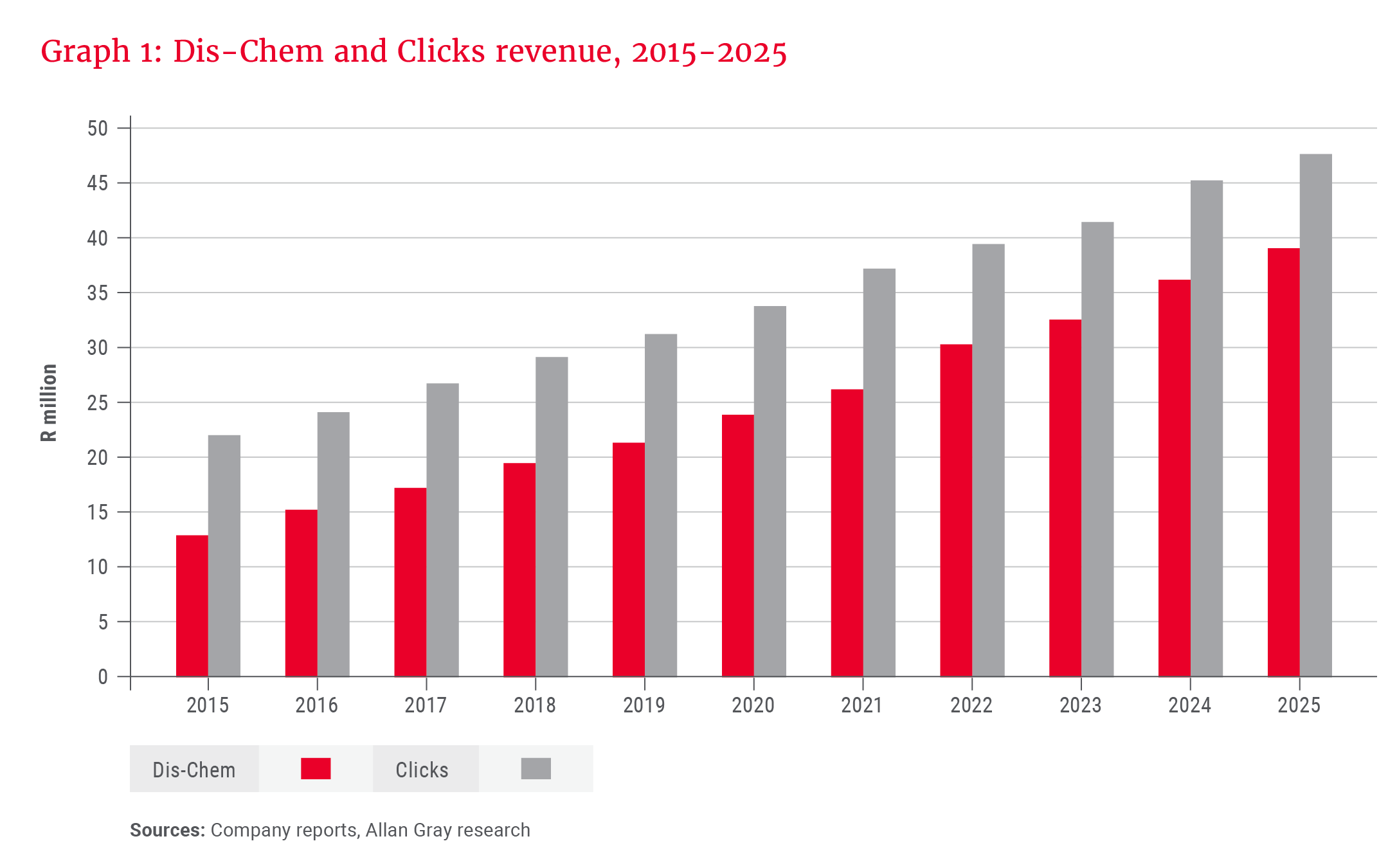

Dis-Chem and Clicks now account for more than half of the dispensary market, translating into strong, consistent revenue growth for both businesses.

While Dis-Chem started from a smaller base of pharmacies than Clicks, it has achieved average annual revenue growth of 11% over the last decade, compared with Clicks’ 8%.

“There is reason to believe that this consolidation theme will continue well into the future, as it is incredibly hard for independent pharmacies to compete with large groups,” said Fish.

“Lack of scale to reinvest in price, low front-shop percentages where higher-margin products are sold, no loyalty programmes, and no succession planning are just a few reasons why the consolidation theme should continue to play out.”

Dis-Chem has a large roll-out plan, shifting its strategy in 2023 from 20-25 new stores per year to 40-50. While execution has been slow, Fish said that there are still opportunities to increase the store count.

He added that pharmacy sales are generally resilient through economic cycles. Moreover, the front shop at Dis-Chem includes personal care, hygiene, and cleaning products, which enhances defensiveness.

Dis-Chem’s product mix makes its earnings more stable than those of many other retail formats.

Return on capital should catch up

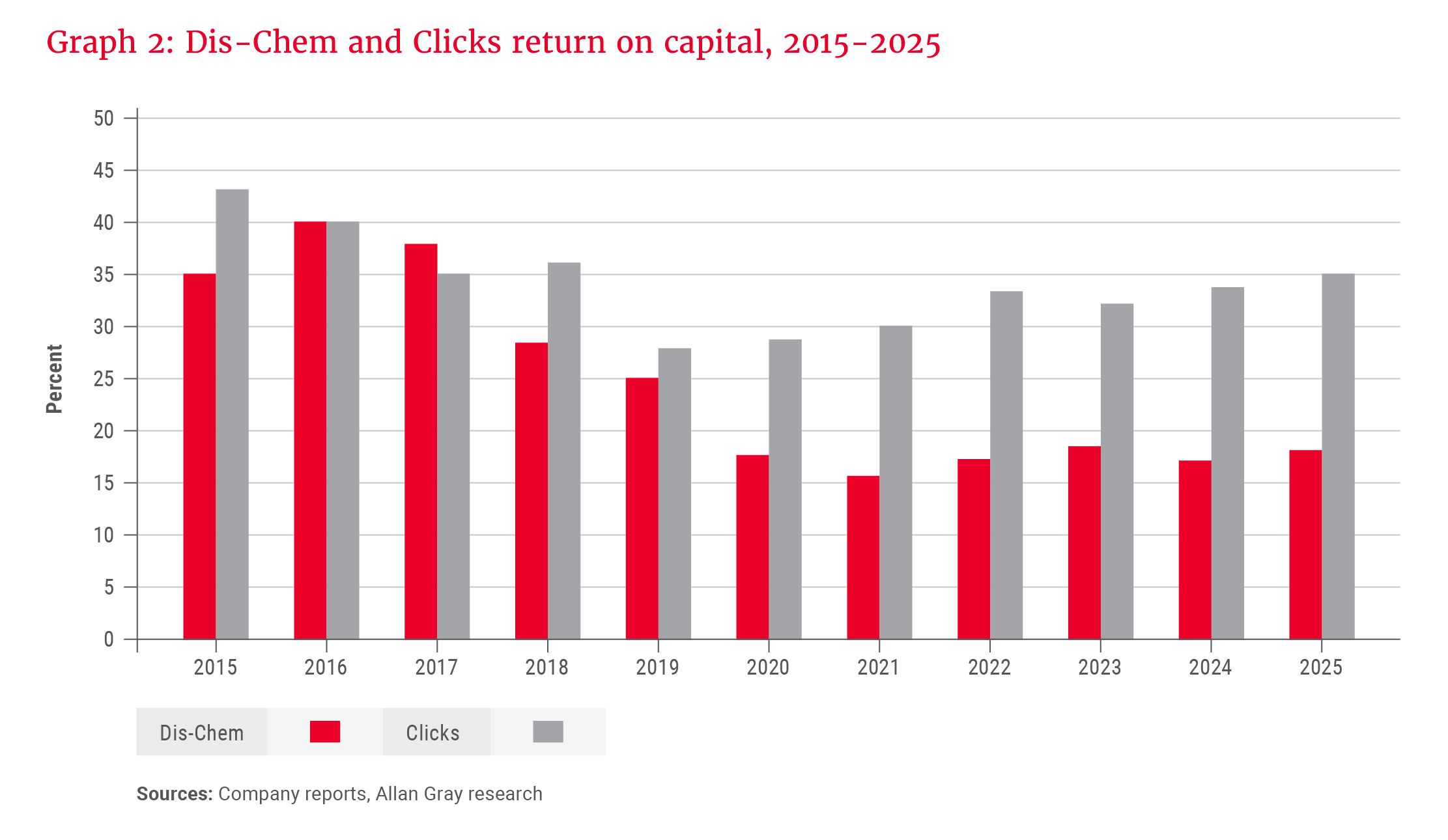

Dis-Chem’s return on capital has declined over the last decade. While some investors may be concerned, Fish said the decline is due to fixable issues rather than a business in decline.

“Investing is inherently forward-looking. Markets often anchor to recent history, but value is created by anticipating what a business can earn in the future, not what it earned in the past,” said Fish.

“The current return profile does not fully reflect the earnings power of a more efficient, better optimised Dis-Chem and return on capital should return to levels well above the company’s cost of capital.”

Several factors support Allan Gray’s view that Dis-Chem’s return on capital should start to reach the company’s cost of capital:

- Cost-cutting measures and margin improvements, including a new centralised store management system

- New smaller-sized stores have better economics

- Better data and analytics under its innovation arm, X, bigly labs, and its new Better Rewards loyalty programme.

Dis-Chem also benefits from stringent pharmacy licensing requirements, which limit competition and ensure consistent footfall from chronic patients.

Returning pharmacy customers also lead to further purchases of higher-margin front-shop products.

Scale is also a benefit for Dis-Chem, as the larger number of stores means higher procurement volumes, improving bargaining power with suppliers and lowering costs.

“These savings are reinvested into lower pricing and better promotions, strengthening the value proposition and attracting more customers,” said Fish.

“Higher traffic then drives further volume growth, reinforcing scale advantages.”

When looking at the balance sheet, the group maintains modest levels of debt, giving it financial resilience and balance sheet flexibility.

Allan Gray also sees a larger amount of earnings to convert into free cash flow over its forecast period. Greater cash provides management with flexibility, reduces risk, and creates value for shareholders.

While Dis-Chem does not appear cheap at 23 times trailing earnings, Fish said that Dis-Chem is trading on just 16 times our normal earnings based on Allan Gray’s estimates.

“For a defensive business with a long growth runway, strengthening returns on capital, and a durable moat, this is an attractive entry point,” said Fish.

“This also screens as attractive relative to Clicks, trading on 22 times trailing earnings, which we view as having a more limited store roll-out pipeline and less scope for margin expansion.”

His comments came prior to Clicks’ latest results, which were below market expectations.

He did warn that the execution of margin recovery and store roll-out will be key. That said, even if management falls short of margin targets, Allan Gray sees Dis-Chem as a great business at a fair price.

Allan Gray clients now own over 10% of Dis-Chem, making them one of the largest shareholders in the company.