Most SA households earning over R14,000 a month belong to a stokvel

The South African stokvel economy, with over 11 million local participants, is currently worth R49 billion according to Thobela Mfeti, research & investment analyst at Glacier, Sanlam, who says that the essence of these groups is to mobilise like-minded individuals towards achieving financial and social goals.

“Members of stokvels come together and make contributions of an agreed amount on a regular basis, usually monthly,” said Mfeti.

“The group decides on how the money is shared, whether it is a rotating lump sum payment to the members or saved and shared at the end of the stokvel period, which is commonly six months or a year.

“This decision is mainly dependent on the type of stokvel.”

According to Mfeti, members of stokvels are almost always saving for something specific such as debt repayment (43%), emergency savings (44%), education (25%), groceries (31%), and clothing (18%).

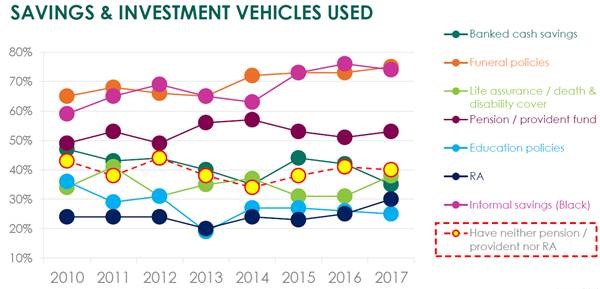

According to Old Mutual’s 2017 Savings and Investment monitor, informal savings (of which stokvels comprise 53%), were the most popular form of savings and investing in South Africa after funeral policies.

This was confirmed by Treasury economist Olano Makhubela who said that 60% of stokvels are investment focused while 18% are investment clubs and 22% are grocery stokvels.

“There is a perception that stokvels are for ‘old women in poor communities’,” said Mfeti. “However, stokvels have become increasingly popular even with high income earners.’

Most households with incomes above R14,000 per month in 2016 belonged to a stokvel, according to Mfeti.

“The more the household earns, the higher the incidence of belonging to more than one stokvel. In 2017, 42% of households with an income of R40,000 and above belong to more than one stokvel.”

Investment and stokvels

Stokvels are short term in nature. In a rotating stokvel, each member gets a turn to receive a lump sum of pooled contributions at least once in the lifetime of the stokvel.

The lifetime is typically six months or a year, depending on the number of members.

Stokvels can be used by individuals to establish a sizable amount of capital to invest in a formal and a longer-term investment structure.

‘Stokvellers’ can use their capital to access longer-term and higher growth assets through products such as tax free savings accounts (TFSA) or retirement annuities (RA).

Stokvels can also be used to fund retirement savings, with approximately half of the informal savers currently without a pension or provident fund, said Mfeti.

“Most of these people have funeral policies, which goes to show that people generally prepare more for events with certainty such as death than they do for events that are dependent on probability (less certain events) such as retirement.”

“The national savings rate is currently at 16%, therefore South Africans do not save enough.

“More and more people retire with insufficient savings to fund their retirement, making stokvels an ideal vehicle to be used in bridging this gap towards providing for sustainable investments,” she said.

Future investment companies

There has been a shift in the stokvel savings community towards longer-term investing, with investment clubs now investing in vehicles such as property or equities, said Mfeti.

The idea is similar to stokvels where the members contribute to the investment club on a monthly basis, raising the capital to fund the investment for these long-term assets.

“The structure is usually treated as a company with the members having an equal ownership,” she said.

“These are stokvels which are more formalised in structure and more long-term focused.”

She warned that corporates cannot underestimate this fast-growing informal sector, and need to service it differently from how the traditional formal investments are serviced.

The trick is not to remove the short-term nature of stokvels, but rather to overlay it with investment education and long-term investment options, she said.

“Most informal savers believe they cannot afford financial advice or do not know how to access it.

“Financial institutions need to debunk these beliefs, reach out to ‘stokvellers’ and assist these savers to channel their hard-earned money toward sustainable, long-term growth investments that lead to wealth creation over time.

“Harnessed properly, stokvels have the power to provide broader access to financial products for lower and middle class South Africans and to act as a catalyst towards sustainable wealth creation,” Mfeti said.