The biggest complaints taxpayers have with SARS – and why it is blocking refunds

The Office of the Tax Ombudsman (OTO) has released its annual report for 2017/2018.

In South Africa, taxpayer complaints lodged with the OTO must relate to a service, procedural or administrative matter arising from the application of the provisions of a tax Act by SARS.

A complaint is accepted if it falls within the mandate of the OTO in terms of section 16 of the Tax Administration Act.

The proviso, however, is that the taxpayer first needs to exhaust SARS’ internal resolution mechanism.

According to the report, the ombudsman received 17,920 contacts during the reporting period – 14,268 were queries and 3,652 were complaints.

The preferred mode of contact by taxpayers is email (95.37%) followed by fax, post and walk-in visits.

Most users who contacted the OTO in the 2017/18 financial year were individual taxpayers, who accounted for 53.77% of users. Tax representatives accounted for 46.23% of users.

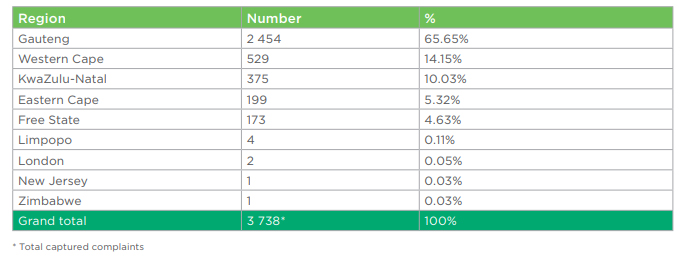

The majority of taxpayers whose complaints were captured reside in Gauteng (65.65%), followed by the Western Cape (14.15%).

Total complaints validated for the period under review came to 3,637, of which 1,945 were accepted as falling within the Office’s mandate, 446 were later terminated and 1,692 were rejected. The latter either did not fall within the mandate of the Office or were prematurely lodged by taxpayers.

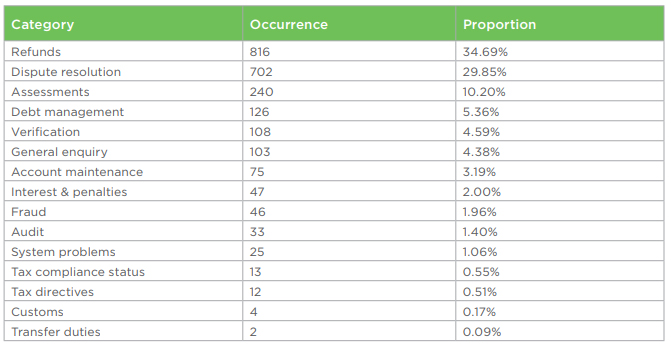

The majority of the complaints reviewed by the OTO related to refunds (34.69%), followed by dispute resolution (29.85%), and assessments (10.20%).

At the end of the reporting period, 786 accepted complaints were carried forward to the 2018/19 financial year. The number of unresolved cases carried forward from previous periods remains a concern and is due to delays by SARS in considering the recommendations of the Tax Ombud, it said.

The table below shows the time it took for SARS to finalise recommendations from the OTO.

Blocked refunds

The ombudsman also provided a breakdown of some of the most serious issues experienced by taxpayers, as well as analysis of systemic and emerging issues.

Notably, the payment of refunds was at the top of the list with a wide number of reasons given for delays and non-payment.

According to the OTO these include:

- Failure to link submitted documentation requested by SARS to the main file;

- Unwarranted placing of special stoppers;

- Using the filing of new returns as an excuse to block refunds;

- Delay in the lifting of stoppers and lack of timeframe for doing so;

- Refunds for one period being withheld while an audit/verification is in progress for another period;

- Using historical returns to delay the payment of refunds.

- Raising assessments to clear unallocated credits;

- Requesting further information which was previously requested and submitted during audit;

- Assessments successfully disputed, but refund still not paid out;

- Diesel refunds;

- Raising assessments prematurely;

- Debt set-off notwithstanding a request for suspension of payment

In 7 February 2018 SARS responded on each of the above issues as follows:

- Procedures would be reaffirmed internally to SARS staff; upload size for documents would be increased from 2mb to 5mb; and SARS was exploring system improvements i.e. allowing taxpayers to re-open a case to submit further documents.

- SARS undertook to finalise 80% of all “special stoppers” within 21 days and “banking detail stoppers” within 5 days.

- SARS implemented system changes to stop this practice for VAT; however it seemed not to be effective and SARS implemented a manual solution for income tax pending the system being fixed. The fix will be rolled out for other tax types in future.

- SARS would align its systems to ensure consistency and consider basing compliance status on a limited historical period.

- SARS will ensure strict compliance with the TAA and develop new procedures to deal with unallocated credits in line therewith.

- Officials will be reminded to comply with existing procedures when requesting relevant information.

- SARS was considering internally adopting a shorter period than the 45 days allowed by legislation to ensure timeous revision.

- SARS noted that the intention to split the returns was already included in the 2018/19 budget review.

- Educational material would be reviewed and standard verification letters will be updated to be more specific where possible. No response was given on the subsequently identified matters.

- The process for applying for suspension of payment has been automated since May 2017

Additionally, the OTO said that it made its own recommendations to SARS in an effort to help reduce these issues, and it indicated that various engagements had taken place focusing primarily on the issue of refund complaints.

It noted that in the last engagement it requested SARS to provide specifics on the implementation of each of the OTO’s recommendations to enable it to monitor the effectiveness efficiently – however SARS is yet to respond.

Tax Ombud Annual Report 17-18 by BusinessTech on Scribd

Read: Tax ombudsman to investigate SARS over growing complaints