This is how much you could lose if you cash out your retirement funds early

South Africans who cash in their retirement savings when changing jobs are not doing themselves any favours.

This is according to Hilan Berger, head of Institutional Business Development at 10X Investments, who said that 70% to 80% of South African employees opt to ‘cash out’ when leaving an employer.

“This behaviour is partly borne out of ignorance, because people believe they have time to play catch up. But to do so, they would have to work much longer, or save much more, to make up the shortfall,” he said.

Below Berger provided an example of someone who is investing R1,000 per month (growing at 1% pa) for 40 years, earning a net real return of 5% pa.

If this programme is followed for 40 years the saving would grow to R1.7 million, Berger said.

If this programme is followed for 40 years the saving would grow to R1.7 million, Berger said.

“Cashing out after 10 years, and starting over would reduce the payout to R910,000 (47% less).

“Cashing out after 20 years, and starting over, means a retirement savings pot of only 25% of what it could have been (R440,000).”

Berger said to make up the ‘10-year’ shortfall, you would have to save twice as much thereafter every month; to make up the ‘20-year’ shortfall, you would have to save four times as much.

“So instead of cashing out, rather exercise the option to transfer your retirement savings tax-free to your new employer’s fund or to a preservation fund.

“By preserving your savings, you not only preserve all the tax benefits, but also all the future returns on that money that you would otherwise forego, and ultimately, the lifestyle that you wish to retain into retirement,” he said.

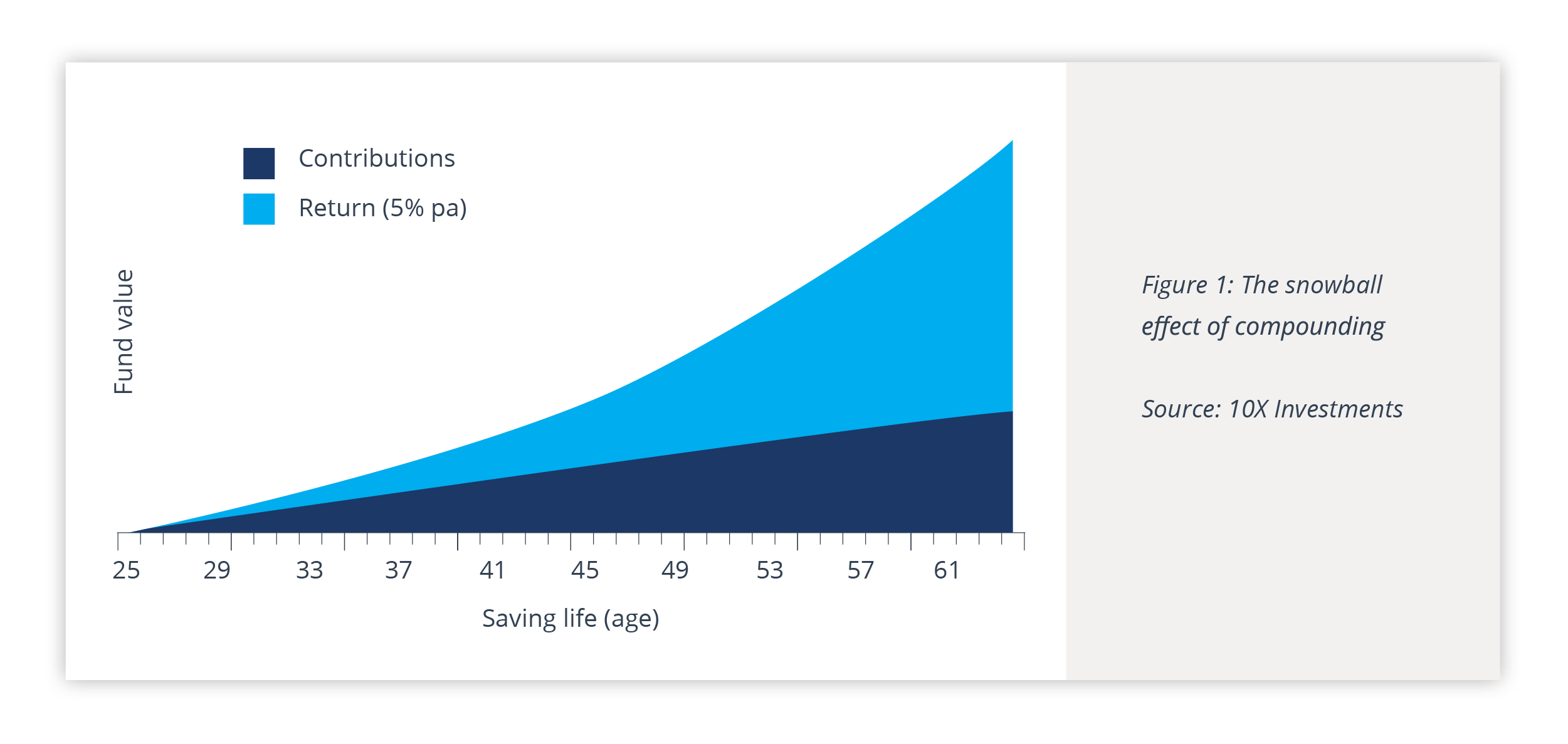

Snowballing

The earlier you start to save for retirement, the longer your money has to work for you, Berger said.

The earlier you start to save for retirement, the longer your money has to work for you, Berger said.

“Early on, the return component is just a tiny fraction of your total savings, and it takes quite a few years to become significant.

“In the above graph, returns equal contributions only at around age 50, after 25 years of saving and investing. However, at the end of the period (only 15 years later) returns are more than double contributions.

This shows that it takes some time for compounding to become a powerful force, with the big acceleration happens around the 20 years-mark, he said.

“For example, say you earn a total real (after-inflation) return of 4% per annum (net of fees of 1% pa) on your annual contribution to your retirement fund.

“After 10 years, returns will equal roughly 32% of your total contributions, after 20 years that will be 74%, after 30 years 132%, and after 40 years 217%.”

Read: The biggest mistakes that individual South African investors make