Worst news in two years for people earning salaries in South Africa

While salaries in South Africa are rising, they are not keeping pace with inflation, resulting in real earnings dropping to their lowest level in two years.

This is according to the latest PayInc Net Salary Index for May 2026, which showed that earners remain under significant pressure.

Rising inflation, higher fuel costs and economic uncertainty continue to erode purchasing power, the group said.

The PayInc Index tracks the monthly average nominal net salaries of around 2.1 million salary earners.

The Nominal Salary Index increased by 0.9% year-on-year in May, bringing the average salary to R21,510 per month in nominal terms.

However, in real terms—accounting for inflation—salaries are lower at R20,262, down 2.8% year-on-year, the worst position since 2024.

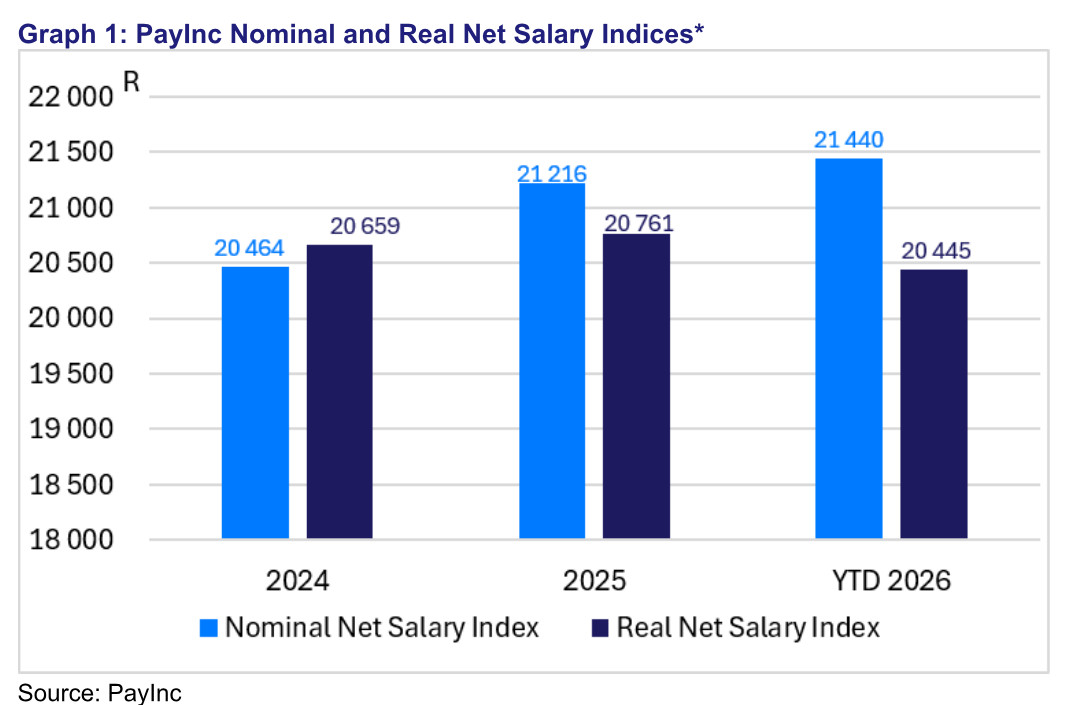

Year-to-date, a similar picture emerged, with the salary for 2026 averaging R21,440 in nominal terms, but down to R20,445 in real terms.

For the first five months of 2026, nominal net salaries increased by just 1.7%, while real salaries declined by 1.7%, signalling a challenging year for consumers after two years of relatively strong earnings growth.

“While nominal salaries have edged higher, the reality is that salary earners are losing purchasing power,” said Elize Kruger, Independent Economist.

“This is placing increasing strain on household budgets and is likely to weigh on consumer spending and broader economic growth during the remainder of the year.”

Fortunately, there could be some relief on the horizon for the local economy in the coming months.

Households under strain

PayInc noted that the pressure on consumers is evident in South Africa’s economic data, but recent developments in the Iran War could point to relief further down the line.

The deterioration in financial health in recent months came amid a sharp increase in fuel prices and a rise in interest rates following the outbreak of Middle East conflict.

These developments pushed consumer inflation from a recent low of 3.0% in February to 4.5% in May, placing additional pressure on both households and businesses.

Real household final consumption expenditure (HFCE) increased by only 0.1% quarter-on-quarter in the first quarter of 2026, compared to growth of 1.2% in the fourth quarter of 2025.

Spending growth was mainly for essential categories such as transport, housing, electricity and utilities.

Expenditure on restaurants and hotels, food and non-alcoholic beverages, and other categories weakened, reflecting growing pressure on household finances.

The growing economic uncertainty also weighed heavily on confidence levels.

The FNB/BER Consumer Confidence Index (CCI) fell from -7 in the first quarter of 2026 to -19 in the second quarter, representing a significant decline in consumers’ willingness to spend.

Similarly, the RMB/BER Business Confidence Index (BCI) dropped by eight points to 39 in the second quarter, reversing gains recorded over the previous two quarters.

Real GDP growth is currently forecast at 1.3% for 2026, marginally higher than last year but still insufficient to drive meaningful job creation or significant wage growth.

“The combination of higher living costs, weaker confidence and ongoing uncertainty is creating a difficult environment for both consumers and businesses,” said Kruger.

“Companies are likely to remain cautious in their investment and hiring decisions until there is greater clarity on the economic outlook.”

However, despite the current challenges, there are early signs that inflationary pressures could begin to ease in the coming months.

Following a tentative Middle East peace agreement, international oil prices have retreated, with Brent crude declining to around US$77 per barrel.

Current fuel price over-recoveries suggest petrol and diesel prices could decrease by approximately R2.50 per litre and R3.75 per litre, respectively, from July—although this will be offset by the full return of fuel levies.

Nevertheless, this anticipated relief, which could extend into August if oil prices remain subdued, may help stabilise consumer confidence and support a more favourable inflation outlook.

This comes with the caveat that uncertainty still remains.

“Although there are signs that inflation pressures may moderate somewhat during the second half of the year, uncertainty and volatility are likely to persist,” Kruger said.

“In this environment, businesses will continue to adopt a cautious approach, which could negatively affect employment prospects and earnings growth for the remainder of 2026.”