Hidden costs of home owning you need to know about

Owning your own home is a huge milestone, but the purchase price of your new house is not the only cost that you need to consider.

Whether you are buying your first house or upgrading, understanding the hidden costs associated with owning a home is crucial.

“You need to be aware of all the costs associated with buying a property and what you can afford to pay on a monthly basis,” said Tahir Desai, Senior Content Manager in Private Property’s Marketing department.

“The bond repayment and affordability calculators on Private Property are a great place to start.”

To help potential homeowners better understand this, Nedbank has created a buyer’s guide that provides a step-by-step explanation and offers all the information you need about being a homeowner.

As you draw up your budget, you will want to consider the following monthly expenses outlined by Private Property.

Utility fees

Your local municipality will charge you for your use of water and electricity every month, and you might need telephone and internet lines as well.

The costs vary from area to area, and also depend on the system available in the area, whether a prepaid system or monthly billing.

Fortunately, you can monitor your consumption by making use of a prepaid system, allowing you to pay upfront for electricity and carefully monitor your spending.

The cost of your internet will depend on the service provider you choose and the type of connection that you want.

Rates, taxes and levies

Depending on the value of your property, the cost of your rates and levies can range anywhere from a couple of hundred to a few thousand rand every month.

Rates cover services such as sewerage facilities, road maintenance, street light maintenance and refuse collection.

Rate calculations are based on your property type, while your taxes are calculated against the value of your property.

If you are buying a sectional title property such as a property in a complex or a flat, you will be charged levies.

These are the costs involved in running the complex, such as limited building insurance coverage, repairs and maintenance.

Some suburbs have extra levies that are used for security purposes, like a boom operator, which are usually voluntary.

These costs are usually made available to you during the house hunting stage, and you’ll need to factor them into your budget when choosing a home.

Homeowner’s insurance

Homeowners insurance is mandatory when you apply for your home loan, as it covers your property against loss and structural damage.

The monthly premium depends on the loan amount granted for your property, and they can be included in your monthly bond repayments.

There are many competitive options available, so you should shop around for an offer that best suits you.

Homeowners insurance does not cover the contents of your home, however, so you will need to look at home contents insurance if you’d like to insure your possessions.

Owning your own home is exciting and liberating, and with planning, you can budget for these expenses and gain some control and confidence as you settle in to your new house.

But should you buy?

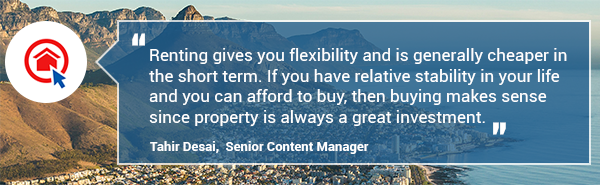

One of the most frequently asked questions that people looking to buy a home have is “should I rent or buy?”

Desai explains that the answer depends on your personal circumstances.

Due to a decline in the economy and rising interest rates, the South African property market is starting to turn towards a buyer’s market.

“In a buyer’s market, homes tend to take longer to sell and often sell for the less than the asking price. It is therefore key for sellers to price their homes correctly from the outset,” says Desai

For buyers, this is a fantastic opportunity to negotiate a favourable deal since there is less competition for property.

When choosing where to buy, Desai advises that “Buying property is a long-term investment and over the long term most property will show good returns.

“By choosing lifestyle you get to enjoy a lifestyle that improves the daily quality of your life while still getting the benefit of investing in the property market.”

However, he cautions that property is a long term investment and so the decision should be carefully considered.

“It is best to choose a home that you would like to keep for a while. Sell too soon and you won’t reap the benefits of a good financial return on your property.”