STANLIB balanced funds position for a low-growth, low-inflation future

Herman van Velze and Kobus Nell; STANLIB Balanced and Equities team.

Speaking at the 2021 Investment Forum, hosted by The Collaborative Exchange earlier this week, STANLIB’s Balanced and Equities team Herman van Velze and Kobus Nell shared their views on the pressing topic of growth and inflation in a post COVID-19 environment.

With inflation trending lower for many years prior to 2020, the word “inflation” was less prevalent in investment vocabularies.

This year, “inflation” is one of the words most bandied about in markets. For some investors it is a concern, and for others it represents an opportunity.

In the short term, economic indicators, both globally and in SA, are indicating price pressures.

But we believe that in the medium term, growth will slow, and inflation will moderate to lower levels, mainly due to the underlying structural factors that kept inflation low pre-COVID-19 are still in place.

Interestingly, global trend growth since 1980 has been around 3.3%. Beyond 2022/23 we see growth back to that level again, or lower.

Government support to protect asset values is ultimately negative for structural growth beyond the cyclical recovery.

The classic “accounting 101” equation is that assets are equal to shareholders’ equity plus liabilities.

Similar to the global financial crisis in 2008, Governments stepped in during the current pandemic to protect the asset base by taking on more debt.

This in effect sustained manufacturing capacity and an imbalance between debt and equity in the economic system occurred, which ultimately affected the confidence to invest negatively.

We are further of the view that this move by governments largely provide a once-off and not sustainable benefit to the economy, and in fact depresses growth as debt servicing burden won’t go away for quite some time.

Since the 2008 global financial crisis, when the US government stepped in to protect households and financial institutions from the consequences of excessive borrowing in the preceding years, government debt has been increasing faster as a proportion of GDP.

After the recent pandemic, the US government took on even more debt, and it currently stands at over 120% of GDP.

Normally, a recession is followed by an investment boom when asset prices correct and available capacity contracts.

That may not happen in the current cycle, as it did post the global financial crisis in 2008. The level of government intervention has been the key factor that explains the difference in our view.

Another longer-term potential structural factor impeding growth is the ageing population in developed countries, with Japan providing empirical evidence of how that practically slowed consumption and growth.

In the short term, there are concerns that supply bottlenecks and job vacancies in the US will push up wages and inflation.

As a result of shutdowns, there were shortages of many inputs such as semi-conductors, shipping capacity and lumber, but these shortages are unlikely to persist as economic activity normalises and supply chains gets readjusted.

Interestingly, Americans seemed to have shown a reluctance to return to the workplace, partly because of generous handouts to the employed and unemployed, and partly because of fears of infection.

But underlying the current shortage is a structural deficit in the labour market, which we think will persist, as corporates have focused on technology and cost-cutting in recent years, which was excelled during the pandemic.

Economies have become more innovative, creating capacity, which increases the output in manufacturing ahead of end-user demand.

A further stand-out has been the low level of bankruptcies and liquidations during the current pandemic, which means there has been minimal downward adjustment in capacity.

The cost of oil as a percentage of GDP remains an important variable in US inflation, but since COVID-19 there has been many changes in behaviour, including people traveling much less as the work from home phenomenon became more integrated with the enhancements of technological solutions that are freely available, for instance frequent long-distance business travel may also be reconsidered given the increased focus to reduce the carbon footprint in general.

This implies a lower level of oil utilisation in the economy.

In future, we see intensity of oil use remaining at lower levels, which is likely to cap the longer-term price of Brent crude and will contain inflationary pressures.

Our view is that inflation expectations are overstated at current levels and likely to moderate in time implies that future interest rates will be contained at moderate levels.

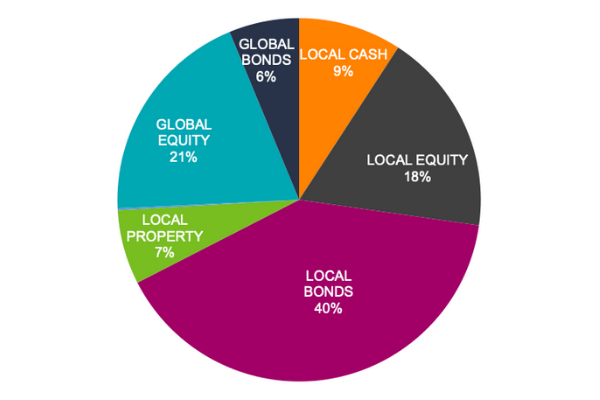

Our balanced portfolios favour long-dated local and global bonds. Currently, our Balanced Cautious Fund is tilted towards local bonds (40%), global equity (21%) and local equity (18%).

SA’s government debt levels have ballooned, but strong metal prices have supported tax revenue collections.

We are also seeing positive political and economic developments, which we expect to maintain the momentum that started to filter through.

These factors, coupled with a low inflation outlook, favour longer-duration bonds especially Emerging Market markets in countries including Mexico, Indonesia and Columbia.

Over the last 10 years, the STANLIB Balanced Cautious Fund has only delivered nine positive years of returns, and in many other years it has delivered double-digit returns, showing the benefits of diversification.

We are confident that in a future lower inflation environment, balanced funds will continue to be an attractive investment.