South Africans getting crushed by Eskom, petrol and diesel hikes

Sharp increases in electricity, petrol and diesel prices in April have sent headline inflation surging, pushing the limit of the South African Reserve Bank’s tolerance band.

Annual consumer price inflation spiked to 4.0% year-on-year in April 2026, up from 3.1% in March 2026.

This was in line with market expectations, as the surge in fuel prices resulting from the Iran War came to bear during the month.

The month also saw power utility Eskom’s 8.8% average price hike for electricity kick in, on top of increases to fixed fees in its pricing structure.

Administered prices for electricity and other gas fuels were up 8.2% y/y, while water bills were up 7% y/y. Overall, administered prices were up 8.3%, more than double the headline rate.

Following a R3 per litre and R7 per litre hike in petrol and diesel prices, respectively, in April, fuel CPI surged 11.4% y/y.

According to Stats SA, in addition to the jump year-on-year, month-on-month pricing also increased by 1.1%, showing a marked upward trend.

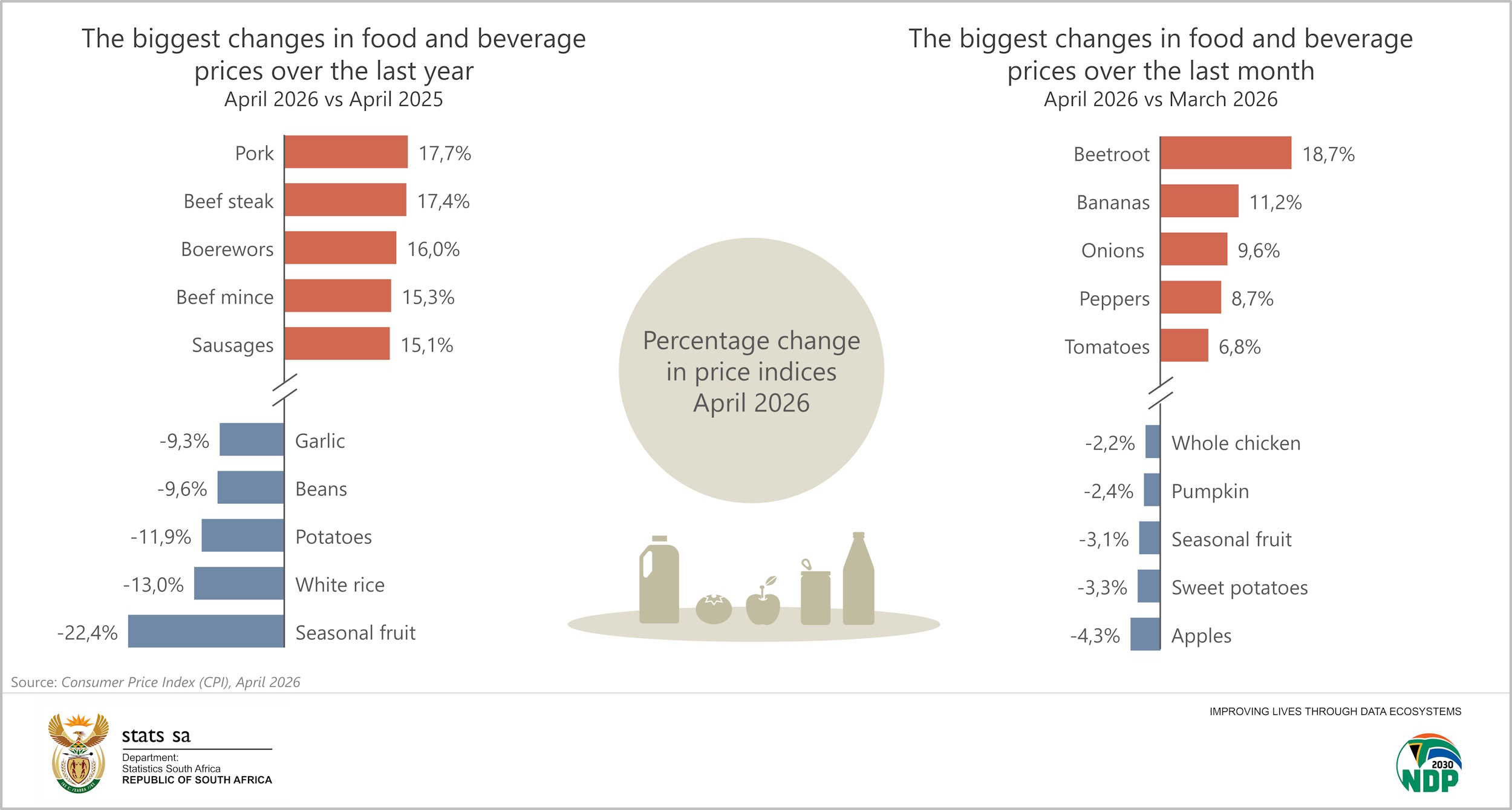

In contrast to the fuel price bruising, annual inflation for food & non-alcoholic beverages (NAB) decreased for a third consecutive month, from 3.6% in March to 2.9% in April.

Six of the eleven food & NAB categories recorded lower annual rates.

Continuing the pressure from the Foot and Mouth Disease outbreak in the country, meat prices continued to show high y/y price inflation, recorded at 9.4% for April.

However, meat also registered the largest decline, easing from 11.6% in March.

Beef mince inflation slowed from 22.2% to 15.3% and stewing beef from 22.6% to 8.7%. The rate for pork moderated from 19.5% to 17.7%.

The cereal products category recorded its third consecutive month of deflation.

Five of the nineteen items in the category are cheaper than a year ago. These include white rice, maize meal, porridge, basmati rice and bread flour.

Milk, other dairy products & eggs recorded their first annual increase since May 2025.

The rate was 0.1%, up from March’s -0.5%. Powdered milk and eggs continue to occupy deflationary territory, at -3.4% and -5.8% respectively.

Interest rate decision up next

Hitting 4.0% year-on-year is also notable because it is at the upper limit of the SARB’s 1 percentage point tolerance band under its new 3% inflation target, making the prospects of interest rate hikes next week a starker possibility.

The higher inflation figure was expected, with economists pointing to a 3.8%-4.1% y/y range in their expectations.

The spike was inevitable, given the escalating conflict between the US/Israel and Iran since the end of February, and the resultant impact on global oil prices.

Oil prices moving above $100 per barrel have had a direct impact on local fuel prices, with South Africa experiencing two consecutive significant fuel price increases in April and May.

However, the wider warning is that the inflation jump is likely to follow through to May’s data and beyond, risking becoming entrenched the longer the war drags on.

According to Mzimasi Mabece, Head of Domestic Fixed Income at Melville Douglas, the second-round effects of rising prices will be under the SARB’s watch as it considers its next interest rate moves.

“The key concern for central banks is not only the initial fuel shock itself, but whether it becomes embedded more broadly through food prices, administered prices and wage negotiations,” he said.

However, while inflation expectations have drifted higher, Mabece noted that they remain broadly anchored and largely reflect a temporary impact of higher fuel costs rather than overheating domestic demand conditions.

“This is still primarily a supply-side shock. Importantly, inflation expectations have not meaningfully de-anchored, and the SARB retains significant policy credibility,” he said.

The SARB has repeatedly highlighted geopolitical risks and oil prices as important upside risks to inflation, particularly as expectations remain above the bank’s preferred 3% anchor.

Against this backdrop, Mabece expects the SARB to maintain interest rates at its upcoming Monetary Policy Committee meeting on 28 May 2026, while adopting a decisively hawkish tone.

But not everyone is as optimistic as this, with several other economists and finance groups expecting a historically hawkish Reserve Bank to pull the trigger on hikes sooner rather than later.

This has led to a growing view that the Reserve Bank will hike rates next week, with as many as two more hikes on the cards for the rest of the year.