Retirement expectations vs reality in South Africa

Financial services firm 10X Investments has published the fifth edition of its South African Retirement Reality Report 2022, noting that warnings of the last four years have had little effect, and retirement still holds the prospect of deprivation and disempowerment for most in the country.

The economic pain of the last few years has magnified society’s vulnerabilities and caused havoc to ordinary lives and livelihoods.

Increasingly, the data shows that for the majority the issue is not simply one of unrealistic expectations or ignorance, but of economic hardship: 70% of people surveyed say they simply cannot afford to save because there is nothing left at the end of the month.

One bright spot in this year’s survey is that the steady deterioration in a key trend has halted, reversed even, said 10X. The share of people not providing for retirement at all has reverted to the 2019 level of 46%, after hitting 50% last year.

That leaves 54% of people indicating that they have a savings plan of some sort, although most of them will admit they don’t know too much about it.

As with our previous reports, RRR2022 shows a widespread lack of retirement planning, a lack of engagement that often manifests in hubris and unrealistic expectations which, in turn, leads to further disengagement.

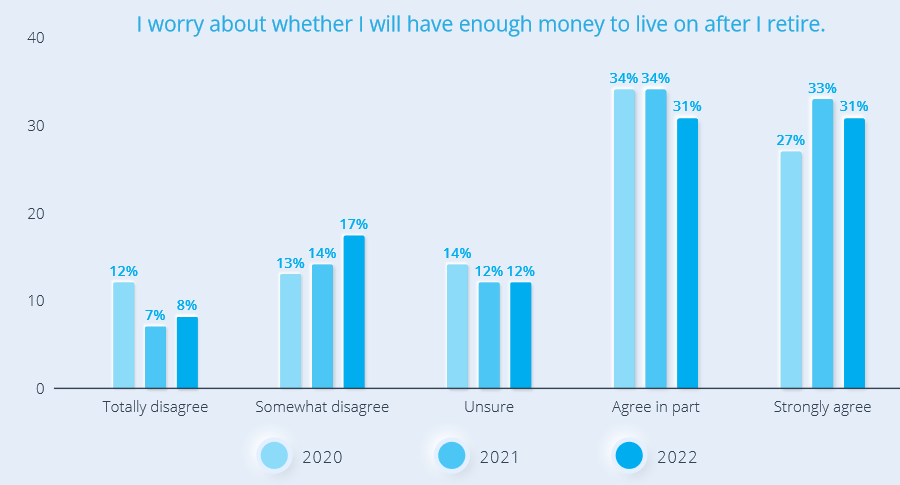

Just 7% of respondents feel confident that they are on course for financial independence in retirement, with the other 93% accepting that they will probably have to supplement their income after they retire, or feeling sure about this.

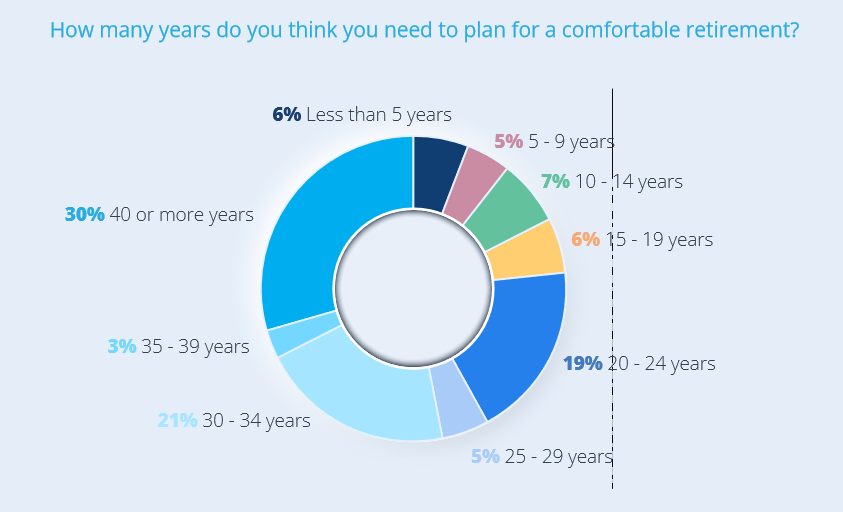

Perceptions have barely changed since last year’s report in terms of how long people think it takes to save for a comfortable retirement. Almost half those surveyed think they can save for retirement in less than 30 years.

“It is recommended that workers save an average of 40 years throughout their working life, keeping the required savings rate at a manageable 15% of earnings. Skipping the first 10 years exacts a disproportionate punishment because money invested in the first years will grow the most.

“Thanks to the benefit of compounding, small amounts invested in a well-diversified high equity fund at a low cost will grow to amounts that might be difficult to imagine at the start of a savings programme,” said 10X.

The fact that most people think they can leave it late (ie to the final 20 or 30 years of work) is a fundamental problem. This issue is a significant contributing factor to SA’s retirement crisis, the group said.

This report is based on the findings of the 2022 Brand Atlas Survey.

Brand Atlas tracks and measures the lifestyles of the universe of 15.4 million economically active South Africans – defined as those living in households with a monthly income of more than R6,000, aged 16+, with internet access through online completion surveys.

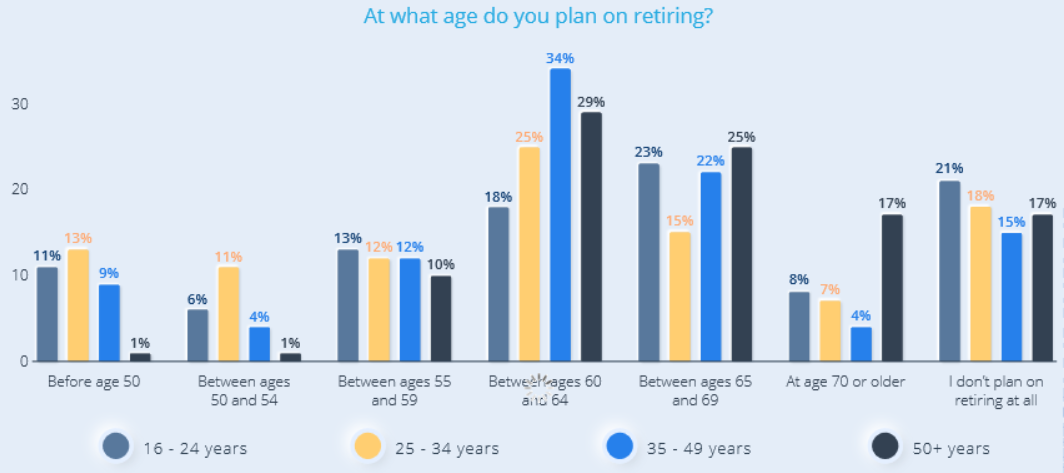

It is striking that whereas some 33% (2021: 35%) of respondents under 35 believe that retiring below age 60 is achievable, only 12% (2021: 5%) of over 50s consider this realistic, said 10X.

“In the same vein, whereas among the younger cohort (between ages 25 and 49), on average, only 41% (2021: 46%) expect to work past the age of 64, among those 50 years and older, 59% (2021: 71%) have wised up to their retirement reality and expect to retire beyond age 64, or not at all.”

Both sets of expectations seem unrealistic in a country like ours, the savings expert said.

“Perhaps the older people felt somewhat buoyed by higher market returns last year, boosting their portfolio by 25% or so. This may bring in an element of recency bias, expecting higher returns to continue. It also underlines how people may be swayed in their thinking and financial self-evaluation based on how they feel, or how the market makes them feel.”

Discrepancies between the age cohorts are still quite striking, painting a picture of the optimism of youth versus the experience of old age, said 10X.

Read: New data shows wealthy South Africans under financial strain