One group of South Africans in deep trouble

Young South Africans are increasingly being pushed out of the property market by a cost-of-living crisis and stagnant wages, which could create long-term demand risk to the country’s housing market.

This is the feedback from Hayley Ivins-Downes, Managing Executive, Real Estate, at Lightstone Property, who described the trend as a deep structural problem rather than a temporary setback.

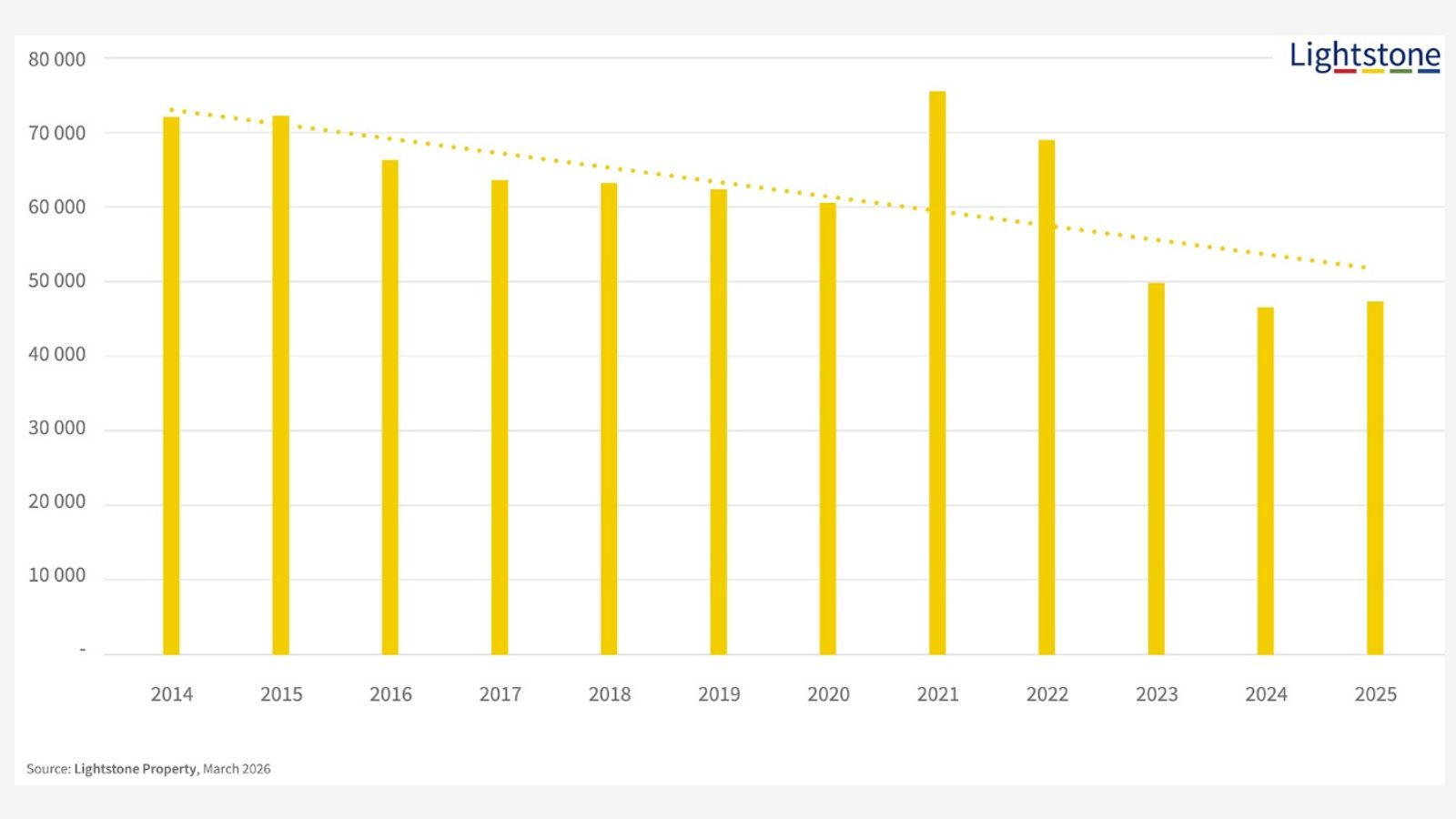

Data from Lightstone Property showed that fewer young people are managing to buy homes in South Africa.

“Our analysis of data from 2014 to 2025 confirms that property volumes have drifted downwards while prices have escalated most significantly in the higher price bands,” said Ivins-Downes.

“The revealing and worrying aspect is the decline of buyers between the ages of 18-35, both in percentage terms from 40% to 30% but also in absolute numbers from 72,000 in 2014 to 47,000 in 2025,” she added.

She warned that this shift reflects a broader affordability crisis. “Economists, policymakers, and institutions have come to the same conclusion.

“The Organisation for Economic Cooperation and Development (OECD) and International Monetary Fund (IMF) have increasingly described this as a structural affordability problem, not just a temporary cycle,” she said.

Ivins-Downes explained that there are several reasons behind the drop in younger buyers across the market.

These include lifestyle changes, house prices rising faster than wages, large deposit requirements, and higher student debt.

Other reasons include stricter mortgage rules following the 2008 global financial crisis and even a lack of confidence in the government or the future. The result is a generational imbalance in wealth.

“We are seeing that the younger people rent from older people, often paying higher proportions of their income for housing. In the process, housing wealth has shifted towards older generations,” she said.

While parts of the market remain resilient, this has done little to ease pressure on younger households. The broader economic environment is compounding the problem.

Cost of living is hitting the property market

According to Competition Commission senior economist Raksha Darji, South Africa is facing a prolonged cost-of-living crisis that has steadily intensified.

In an interview with Kaya Biz, she said it started when Russia invaded Ukraine about four years ago, and that it just seems to be getting worse, as global shocks interact with local structural challenges.

The impact on household finances is severe, particularly for lower-income groups and younger earners trying to enter the property market.

“Low-income households spend about 66.81% of their income on food and housing utilities, leaving almost no room to absorb any shocks that may come their way,” Darji said.

Rising administered prices have made matters worse. “Prices have increased by about 85% over this 5 to 6 year period,” she noted.

These increases far exceed overall inflation, with electricity costs placing additional strain on already tight budgets. This leaves many households forced into difficult trade-offs.

She explained that, because their budget is squeezed and prices are increasing, people have to choose between things they shouldn’t have to choose between.

She added that these choices refer to essentials such as food, water, electricity, healthcare, and education.

Structural inefficiencies in the economy are also keeping prices elevated. Darji highlighted rocket and feather pricing.

This is where prices shoot up quickly, but don’t come down as fast as they should when your costs come down.

With little immediate relief in sight, the outlook is concerning. Without meaningful reform, the likely outcome is a continued decline in homeownership, rising rental burdens and widening inequality.

Ivins-Downes said the situation could pose long-term demand risk to housing markets. She explained that if young buyers never enter the market, future housing demand could weaken.

“Housing markets historically rely on first-time buyers moving up the ladder. If the ladder breaks, transaction volumes will fall, and prices will become dependent on wealth transfers (inheritance, family help).”