South Africa’s ‘gold’ bank accounts compared

BusinessTech looks at the middle market accounts of South Africa’s five biggest banks – Standard Bank, FNB, Absa, Nedbank and Capitec – calculating each monthly cost based on a set number of transactions.

The transactions used are those outlined by Solidarity’s Research Institute in its annual banking charges report. While the group has not published a new report for 2018, the transaction profiles have remained the same in each iteration.

According to Solidarity, the profiles are based on guidelines consistent with fee-saving guidelines published by the banks – promoting digital channels and reducing physical interaction with the banks as much as possible.

The banking profiles are split into low-income groups (12-17 transactions), middle income groups (25 transactions) and higher income groups (30 transactions).

While these middle market accounts are targeted at the middle-income groups, the comparison below takes into account the costs for all profiles – and includes both the pay-as-you-transact fees, as well as the bundles offered.

Unlike entry-level accounts, which typically have set fees for transactions, middle-market accounts use slightly more complicated formulae to calculate costs, particularly when it comes to deposits and withdrawals.

The one account that differs is Capitec’s Global One, it has all the same price points as in the entry-level account comparison, and uses a set-fee structure.

Capitec’s Global One account is the only account offered by the bank, and targets both entry level and mid-level consumers.

However, the retail banks offer bundle options, which carry a higher monthly account fee, but in turn remove the single fees attached to the various transactions (with limits).

Similar trends can be seen across the other bundled products. This is how all the accounts compare:

Absa

Absa’s pay-as-you-transact fees carry costs for almost every transaction – making its Gold Value bundle appear like a no-brainer.

Absa’s Gold Value Bundle covers all the transactions across the banking profiles used in this comparison, which means all users – light to heavy – will just pay the R105 monthly fee, so long as they don’t go past 5 ATM withdrawals, and stick to the other limits that come with the account.

But other transactions, such as point-of-sale purchases, SMS notifications and external debit order fees fall away.

If you manage to maintain an account balance of over R30,000, Absa discounts the monthly fee by 50%.

Capitec

Capitec stands out among middle market accounts because the Global One has only the one fee structure – which is already among the most affordable in the entry-level market.

Maintaining a balance of R10,000 or more effectively allows the interest earned to cover a large bulk of a month’s transaction fees – though a heavy-use client would have to have a balance of just over R20,000 to see the same full benefit.

When it comes to debit orders, Capitec only has one internal debit order available (for funeral policies), so only the charge for one debit order can apply.

FNB

FNB’s Gold account is available only on the unlimited option, which carries a monthly fee of R105.

The Unlimited bundle has a withdrawal limit of R5,000 at all ATMs (and point-of-sale) before any fees are charged. The maximum ATM withdrawal across the profiles covered is R4,500.

However, beyond this limit, regular fees apply (R1.90 per R100 at FNB ATMs, and the same plus R9 at other ATMs). InContact notifications are free and unlimited, but the R1.25 payment notification SMS for beneficiaries still applies.

Point-of-sale withdrawal amounts are not specified, but outside the R5,000 bundle limit they are charged at R1.60 per transaction. For the sake of this comparison we are assuming that all withdrawals are within the limit.

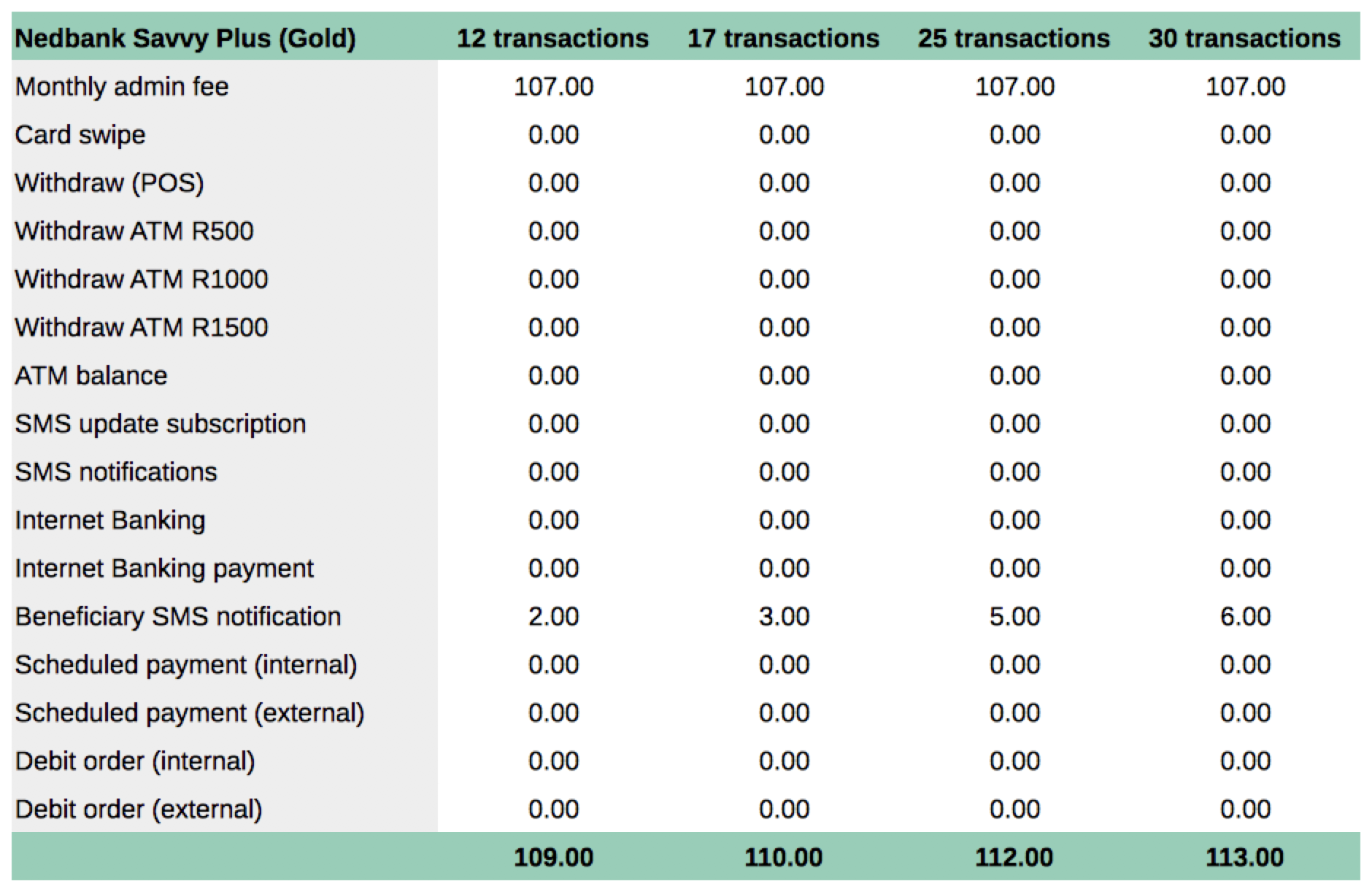

Nedbank

As with FNB, the Nedbank Savvy account only has the bundled options (with the Savvy Plus representing the ‘gold’ equivalent account and the Savvy Bundle representing the ‘platinum’ equivaelent).

The Savvy Plus account offers a host of free and unlimited transactions, with the withdrawal limit before fees kick in set at 4 per cycle. This covers the maximum of 4 withdrawals used in the heaviest-use profile.

As with the other accounts, the only real charges are for third party notifications.

Standard Bank

As with Absa, Standard Bank has three main ways to transact in its middle market account – a bundle option, a pay-as-you-transact option, and a rebate option.

The bundle option again makes the most sense across all the profiles, as it covers practically all the transactions, except for third party SMS notifications.

Standard Bank’s notification system is also different to other banks, not charging for notifications unless a transaction is under R100. A transaction under R100 incurs a monthly subscription fee of R2.52. The breakdown below assumes this fee is applicable.

The group’s rebate option works on PAYT fees, but offers a rebate depending on the positive cash balance at the end of the month. The rebates are between R85.75 (balance of R10,000-R19,999) and R423.68 (balance of R100,000+).

It’s also worth noting that Standard Bank also charges an additional R8.83 per month to old a cheque card instead of a debit card.

The charges used are as reported by the banks in their fee schedules, which you can find here: Absa | Capitec | FNB | Nedbank | Standard Bank