Best news in 8 months for one of South Africa’s most important sectors

The seasonally adjusted Absa Purchasing Managers’ Index (PMI) has risen into positive territory, but there are warnings that the improvement may not be sustainable.

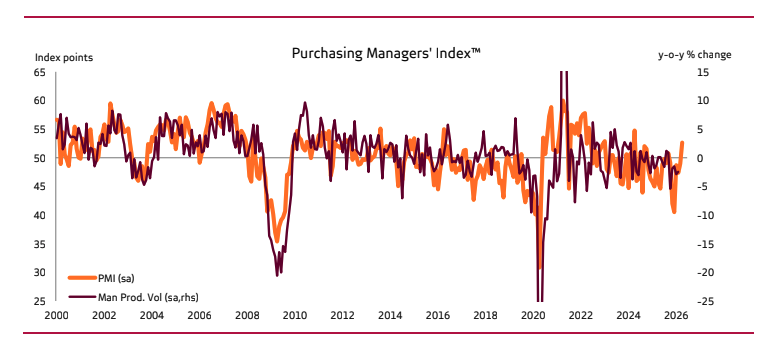

The Absa PMI is an indicator of the health of the manufacturing sector, one of the nation’s largest employers, and is compiled by the Bureau for Economic Research (BER).

The PMI rose above the neutral 50-point mark for the first time since September 2025, increasing to 52.6 in April from 49 in March. This was ahead of Investec’s prediction of a contraction to 47.8.

The Q2 improvement was driven by a rebound in both business activity and new sales orders, which pointed to a stronger start to the second quarter following a weak first quarter.

That said, some of the improvement likely reflects front-loading of demand ahead of expected price increases, raising questions about the sustainability of the recovery.

The business activity index rose for the second straight month, returning to expansionary territory.

This suggested that production picked up meaningfully at the start of Q2 following a subdued first quarter for 2026.

The increase also appeared to be driven by stronger domestic demand, while export sales declined. The divergence suggests the recovery is not broad-based and remains vulnerable to external headwinds.

Some respondents also indicated that orders could have been brought forward in anticipation of further cost increases, which could result in weaker demand in the months ahead.

The inventories index increased and moved above the neutral 50-point mark for the first time since August 2025.

“This likely reflects stock-building behaviour, with firms purchasing inputs ahead of expected price

increases,” said the report.

“While this supported the headline PMI in April, it may also point to temporary factors rather than a

sustained increase in underlying demand.”

Cost pressures grow

Absa noted that cost pressures continued to rise in April, with the purchasing price index rising to 85.6 following the record increase in March.

The index is now over 30 points above its level at the start of the year, reflecting higher oil-linked input costs and a slightly weaker exchange rate.

Absa said that input costs are likely to squeeze profit margins and could limit the sustainability of the April improvement in activity.

Moreover, greater cost pressures at the factory level could contribute to larger inflationary pressures in the economy.

The index tracking expected business conditions improved slightly in April, even if it remains below the neutral 50-point mark.

“This suggests that while purchasing managers are somewhat less pessimistic than in March, confidence in the outlook remains subdued.”

“Most responses were in before the fuel levy relief extension was announced, which does soften the direct hit from the diesel price increase a little.”

| Sub-Index | February | March | April |

| Business Activity | 45.7 | 46.1 | 52.8 |

| New Sales Orders | 45.2 | 44.5 | 52.9 |

| Employment | 42.5 | 43.3 | 43.8 |

| Inventories | 48.1 | 48.8 | 52.3 |

| Supplier Deliveries* | 55.3 | 62.1 | 61.4 |

| Purchasing Prices* | 55.1 | 75.8 | 85.6 |