Here’s what drives us mad about our insurers

South Africa’s insurance sector has seen a significant increase in claims across most products and segments throughout the Covid-19 pandemic, which has also accelerated the digitisation of industry, shifting consumer behaviour and expectations.

It is against this disruptive backdrop that the 2021 South African Insurance Sentiment Index, conducted by PwC South Africa in collaboration with BrandsEye, offers insight into consumer sentiment towards 15 of the country’s major insurers.

The index tracked over 450,000 public non-enterprise posts on social media platforms between 1 April 2020 and 31 March 2021.

The data is based on unsolicited feedback from consumers – customers and non-customers alike – which offers a distinctive view of what people perceive about insurers and where they tend to fall short.

Industry overview

A net sentiment comparison across a broad range of industries saw South Africa’s insurance sector emerge as the industry with the lowest level of negative conversation among consumers.

With an average Net Sentiment score of -0.4%, the insurance industry was followed closely by retail (-1.0%) but significantly outperformed both the banking (-16.3%) and telecoms (-34.6%) industries.

The net sentiment is the net value of all those opinions expressed on social media about a brand or product and is calculated by subtracting the percentage of negative online mentions from the percentage of positive online mentions.

Of the 15 insurance providers included in the index, King Price obtained the highest Net Sentiment of 44.3% and was one of only five insurers to get a positive net sentiment.

King Price’s staff were praised for their competency and conduct, while on the other end of the spectrum, customers of brands 13, 14 and 15 complained about slow service and a lack of response. The lowest ranking insurance brand had a Net Sentiment of -28.0%.

King Price had the highest net sentiment for operational conversation, with 87% of positive mentions complimenting staff competency. Additional positive drivers included staff conduct (47.7%) and turnaround time (22.1%).

Only the top-performing brands were named in the report.

The lowest operational Net Sentiment recorded among insurance brands was -73.2%. Turnaround time was the most significant operational issue for the unnamed insurer, contributing 65.7% to the negative conversation. Other key complaints included no response received (30.9%) and status of the claim (28.2%).

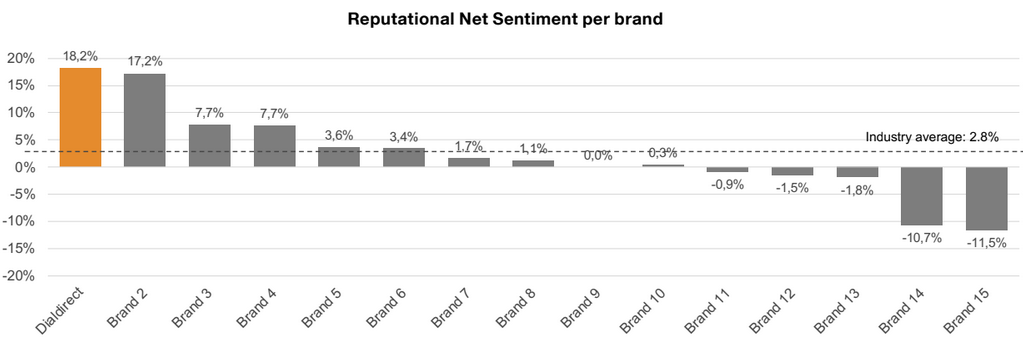

Dialdirect ranked highest in reputational net sentiment, achieving 18.2% — well above the industry average of 2.8%.

Dialdirect’s reputational positivity was driven predominantly by the #DialUpChing campaign, which included premium discounts and a webinar hosted by ProVerbMusic. The brands with the lowest reputational scores were hampered by negative PR incidents as well as complaints associated with Covid-19 claims, the report’s authors said.

Customer experience

“Complaints about turnaround time were seen across all insurance products, brands, and channels, and along all customer journey points, making up 52.8% of the negative conversation. Interestingly, turnaround time was also among the top three drivers of positive conversation (21.5%), showing that it can make or break the customer experience,” PwC said.

Other topics driving negative conversation were no response received (23.9%) and speaking to multiple contacts (16.5%), which highlights customer communications as an area that insurers should consider improving.

The overall claims process across the industry was rated -64.3% in terms of Net Sentiment, driven primarily by customers’ complaints about not knowing the status of their claim.

“Improved responsiveness to customer mentions on social media would not only boost consumer sentiment but also assist insurers in reducing the conduct risk they’ll face when the TCF (Treating Customers Fairly) framework is fully implemented,” said BrandsEye’s chief executive, Nic Ray.

“Given this scenario, insurers would do well to pay close attention to their online conversation and ensure they are equipped to identify through all the noise, the priority conversation that requires attention and action. Doing this not only improves outcomes for consumers but also mitigates reputational risk while ensuring regulatory compliance,” he said.

Read: South Africa’s best and worst life insurance providers, according to customers