The major areas in South Africa where businesses are suffering the most

Third-quarter data from the FNB Commercial Property Broker Survey, which surveys a sample of commercial property brokers in the six major metros of South Africa, shows a perceived easing in levels of financial pressure; however, the rate of improvement is slowing, which is a concern.

The data is drawn from brokers in the City of Joburg and Ekurhuleni (Greater Johannesburg), Tshwane, Ethekwini, City of Cape Town and Nelson Mandela Bay.

Focusing on the key drivers of movement and sales activity in owner-serviced properties, the survey results show financial pressure to still be by far the biggest single driver. However, the latest quarterly reading pointed to a slow continuation of the declining trend, a sign that financial pressure is gradually alleviating as the economy slowly recovers from last year’s deep lockdown-related recession, said FNB property strategist, John Loos.

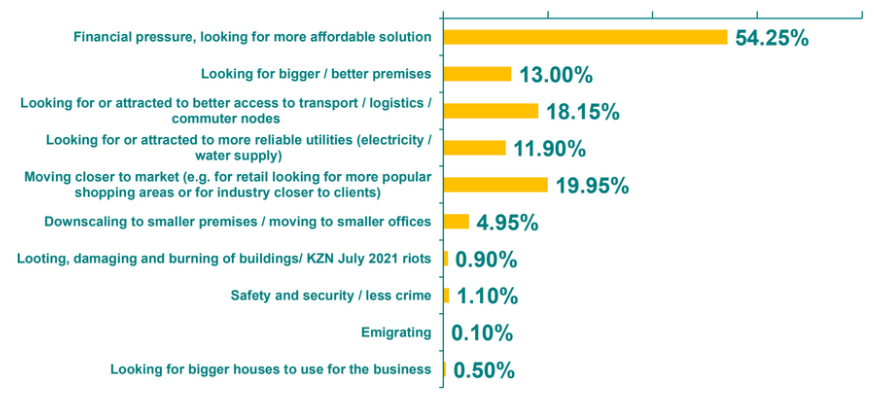

Owner-occupiers are still perceived to be selling or relocating influenced by financial constraints/pressures, i.e. 54.25% in the third quarter 2021 survey. This is only slightly down from 55.35% previously, but more noticeably down from the post-hard lockdown peak of 65.3% reached in the final quarter of 2020.

Factors driving owner-occupiers’ movement and sales

Levels of upgrade-related selling

In another sales motive also possibly reflecting financial constraints, sales and relocation for “bigger and better premises” remains very low at 13%, said Loos. This is still significantly down on the 18.4% reading from the pre-lockdown first quarter of 2020. However, it too has shown some mild improvement from the previous quarter’s 11.1%, the strategist said.

“This percentage has been significantly lower since the start of hard lockdowns in the second quarter of 2020. It had admittedly already declined in prominence as economic and financial times toughened prior to Covid-19 lockdown, but then declined far more noticeably in the second quarter of 2020, to an 8.2% low, as lockdown caused the recession to go far deeper.

“The most recent percentage of 13% thus continues to reflect the combination of tough economic and financial times since the onset of lockdown, combined with a cautious approach to property in a time when business confidence is still weak.”

Relocating to be better positioned

A further key reason for selling, which may reflect both current financial pressures on businesses as well as risk aversion due to uncertainty regarding the economic future, is the estimated percentage of sellers selling in order to move closer to their market, said FNB.

This percentage declined slightly further to 20% of total sellers in the third quarter 2021 survey, the lowest percentage since the survey started, down slightly from 20.5% in the prior quarter, and from 36.3% at the beginning of 2019.

“This suggests a “wait and see” approach by an increased portion of aspirant sellers. While it may often make sense to incur the cost of relocation closer to one’s market, in such weak economic times less relocating and more “staying put” for the time being is the likely outcome,” said Loos.

Coastal metros appear to “outperform”

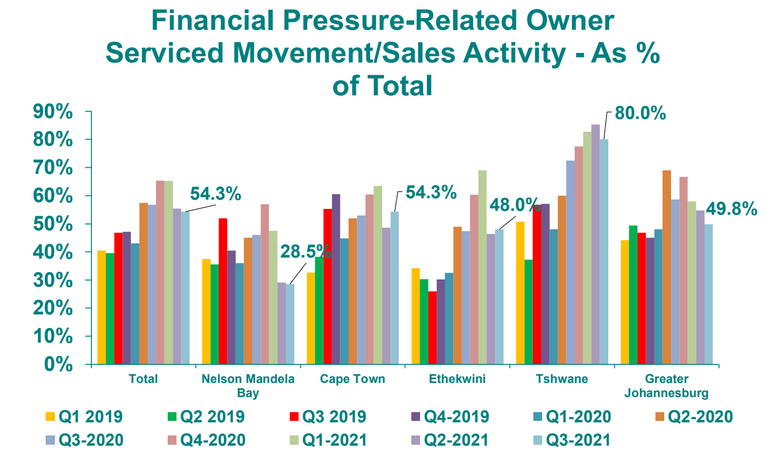

Examining where, by region, the greatest level of financial pressure-related selling or relocation is perceived to be, Gauteng appears on average to have higher (worse) readings due largely to the Tshwane region. Tshwane was the highest in the third quarter 2021 survey at 80% of sellers, while Greater Johannesburg was a significantly lower 49.8%.

Of the 3 coastal metros, the highest (worst) percentage was recorded by Cape Town, i.e. 54.3%, Ethekwini 48%, and Nelson Mandela Bay the lowest percentage of 28.5%.

Conclusion – Financial pressure continues to ease, but the pace of improvement appears to be slowing

Loos said that the slowing pace of improvement compared to the prior quarter’s survey results, is not entirely unexpected, because the economy itself has seen a slowing in the pace of its recovery out of last year’s second quarter hard lockdowns.

“The battle to achieve the last part of “full” recovery back to pre-Covid-10 GDP levels has to do with a portion of businesses across the economy closing down permanently, and thus a smaller economy-wide production capability today compared with the pre-lockdown days.

“In addition, existing businesses took a significant financial knock during 2020’s deep recession, business confidence remains low as a result, so they are not necessarily moving swiftly to expand their own production capabilities. Therefore, we sit with a still-smaller economy than 2019, and significant financial pressure on the business sector still lingers as a result.”