Hope for Mr Price after controversial deal to buy European retailer for R9.6 billion

While Mr Price’s acquisition of European retailer NKD drew widespread shareholder backlash, there is optimism about the deal.

The deal was valued at €487.00 million (roughly R9.6 billion in December when the deal was announced) and was funded by a combination of cash and debt.

NKD has over 2,000 stores in several European countries, including Germany, Austria and Italy. The company generated net sales of €684.57 million in 2024.

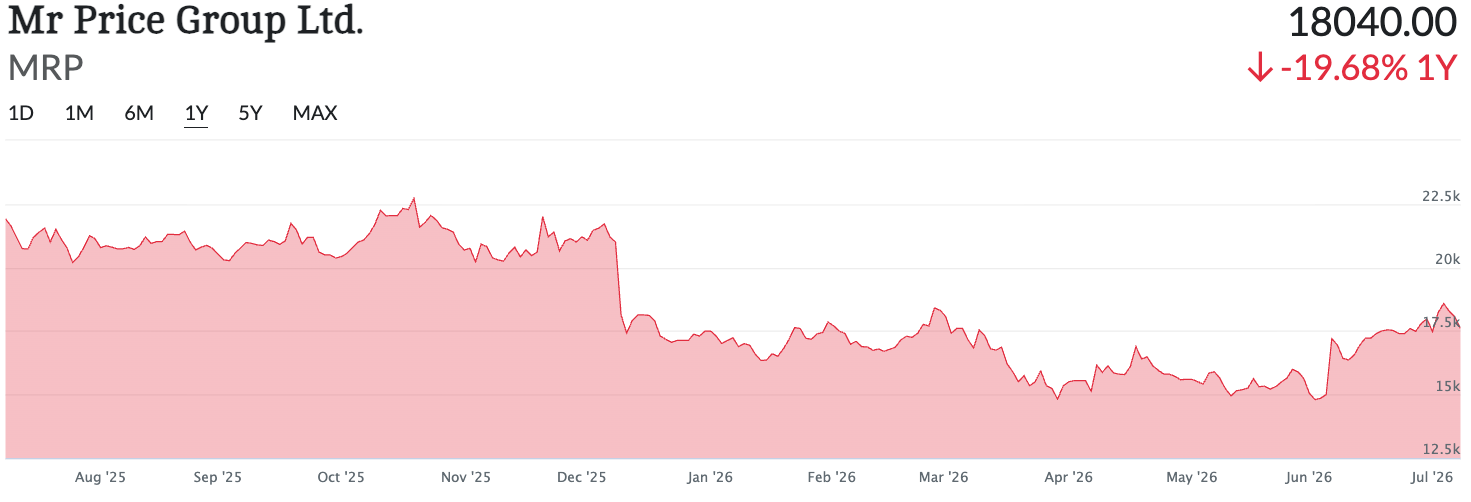

However, the market did not respond positively to the deal, with R6 billion wiped off Mr Price’s market cap on the first day after the announcement.

Analysts from 36One Asset Management and Benguela Fund Managers said that NKD’s financials were incredibly weak.

This includes profit margins of around 1% to 2%, which is far lower than Mr Price’s typical 9% to 14%. Mr Price’s return on equity (ROE) of 27% was also far higher than NKD’s approximately 13% at the time.

The deal also added a massive amount of debt to Mr Price’s balance sheet, with R7 billion in interest-bearing loans following the acquisition.

Several local retailers have also attempted expansion in international markets, with incredibly limited success, such as Woolworths’ acquisition of David Jones for R21 billion in 2014.

Despite the concerns over Mr Price’s acquisition of NKD, Brendan Capstick from Nedbank Private Wealth actually chose Mr Price as his stock pick when speaking with Business Day TV.

Capstick said that Nedbank Private Wealth believes that the deal will be positive on a read-through basis.

He also alluded to the market fears over current headwinds facing South Africa, which include high inflation and heightened interest rates following the United States war with Iran.

He noted that South Africa has recently seen a decrease in petrol and diesel prices. However, his comments came before the resumption of attacks between the two nations.

Financial results are strong

Capstick added that Mr Price’s latest financials were solid, with the company showing attractive valuation metrics.

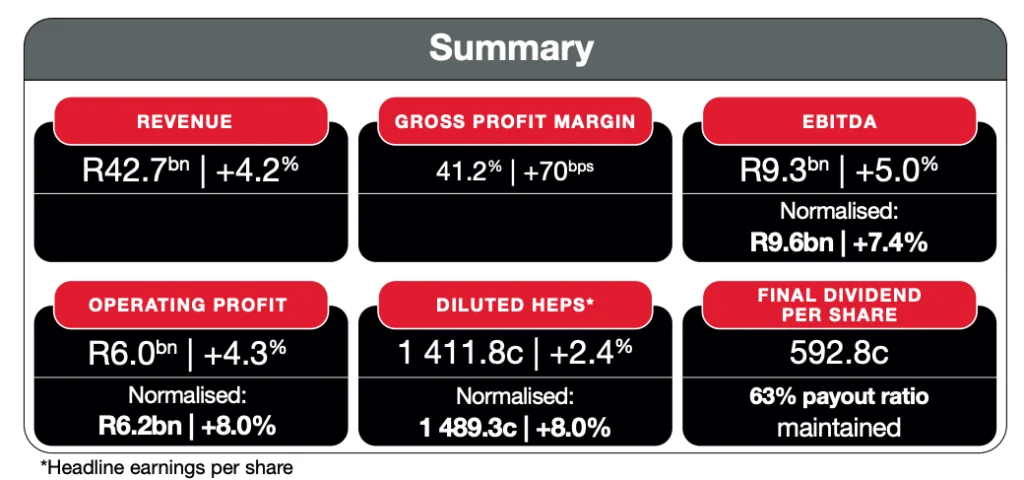

For the 52 weeks to 28 March 2026, Mr Price Group reported total revenue of R42.7 billion, up 4.2% from the prior year.

When using normalised figures, which exclude those costs, basic, headline and diluted headline earnings per share increased by 8.0%, 7.7% and 8.0%, respectively.

On a statutory basis, basic, headline and diluted headline earnings per share of 1,449.5 cents, 1,453.9 cents and 1,411.8 cents, increased by 2.3%, 2.1% and 2.4%, respectively.

The group still declared a final dividend of 592.8 cents per share, maintaining a pay-out ratio of 63%.

Capstick said these results were quite good, with diluted HEPS showing strong growth of 8%. He believes that the management is doing well in driving earnings.

Looking at the stock’s valuation, he noted that Mr Price was trading on a forward price-to-earnings ratio of around 11 and offering a nearly 6% dividend yield, which is strong for a retailer.

The stock is also trading ex-dividend, making it a good entry point for longer-term investors into Mr Price.

The Ex-dividend deadline is the date before which you must own a stock to receive its dividend payment. Stock prices typically decline after this date as cash leaves the business.